corporativa dezembro engl

TRANSCRIPT

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 1/19

Cor orate Presentation

1

December, 2011

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 2/19

Disclaimer

The information contained in this presentation may include statements which constitute forward-

looking statements, within the meaning of Section 27A of the U.S. Securities Act of 1933, as

amended, and Section 21E of the U.S. Securities Exchange Act of 1934, as amended. Such

forward-looking statements involve a certain degree of risk and uncertainty with respect tobusiness, financial, trend, strategy and other forecasts, and are based on assumptions, data or

methods that, although considered reasonable by the company at the time, may turn out to be

incorrect or imprecise, or may not be possible to realize. The company gives no assurance that

expectations disclosed in this presentation will be confirmed. Prospective investors are cautioned

2

that any such forward-looking statements are not guarantees of future performance and involve

risks and uncertainties, and that actual results may differ materially from those in the forward-

looking statements, due to a variety of factors, including, but not limited to, the risks of

international business and other risks referred to in the company’s filings with the CVM and SEC.

The company does not undertake, and specifically disclaims any obligation to update any forward-

looking statements, which speak only for the date on which they are made.

2

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 3/19

The Com an

3

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 4/19

VCP and Aracruz Merged to Create Fibria

Shareholder StructureShareholder Structure

Votorantim Industrial

S.A. BNDESPar Free Float

29.34% 30.42(1) 40.24%(2)

4

(1) Position as of November 30, 2011. BNDESPar has 21% linked to a Shareholder’s Agreement with Votorantim Industrial S.A. during the first 3 years and 11% during the following 2 years.(2) Free Float 40.17% + Treasury 0.07%

4

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 5/19

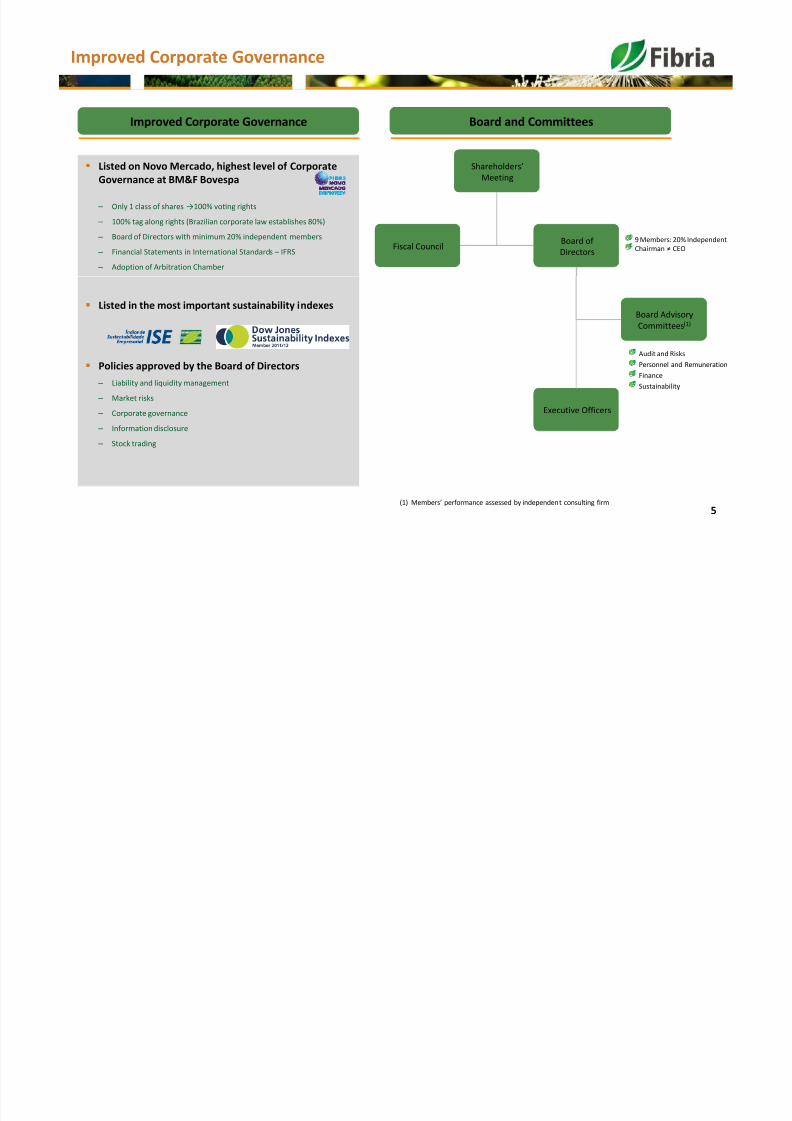

Improved Corporate Governance

Shareholders’

Meeting

Shareholders’

Meeting

Fiscal CouncilFiscal CouncilBoard of

Directors

Board of

Directors

9 Members: 20% Independent

Chairman ≠ CEO

Board and CommitteesBoard and CommitteesImproved Corporate GovernanceImproved Corporate Governance

Listed on Novo Mercado, highest level of Corporate

Governance at BM&F Bovespa

– Only 1 class of shares →100% vo;ng rights

– 100% tag along rights (Brazilian corporate law establishes 80%)

– Board of Directors with minimum 20% independent members

– Financial Statements in International Standards – IFRS

– Adoption of Arbitration Chamber

5

Executive OfficersExecutive Officers

Board Advisory

Committees(1)

Board Advisory

Committees(1)

Audit and Risks

Personnel and Remuneration

Finance

Sustainability

Listed in the most important sustainability indexes

Policies approved by the Board of Directors

– Liability and liquidity management

– Market risks

– Corporate governance

– Information disclosure

– Stock trading

(1) Members’ performance assessed by independent consulting firm

5

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 6/19

A Winning Player

Main Figures(1)Main Figures(1)Superior Asset CombinationSuperior Asset Combination

Pulp capacity million tons 5.25

Net revenues R$ billion 6.0(1)

Total area thousand ha 1,076(2)

Planted area thousand ha 609(2)

6

Port Terminal Pulp Unit

Net Debt R$ billion 9.5

Net Debt/EBITDA X 4.2

Três Lagoas

Santos

Aracruz

Portocel

Caravelas

Belmonte

Veracel

Jacareí

Source: Fibria(1) Last Twelve Months as of 3Q11.(2) As of September 30, 2011, including 50% of Veracel and excluding forest partnership areas (124 thousand ha).

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 7/19

Fibria´s Units Industrial Capacity

Três Lagoas – Mato Grosso do Sul – 1.3 million t/year Jacareí – São Paulo – 1.1 million t/year

77

Aracruz – Espírito Santo – 2.3 million t/year Veracel – Bahia – 1.1 million t/year

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 8/19

Fibria’s Strate

8

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 9/19

Clear Leadership Position

Market Pulp Capacity Ranking 2010(2) (000t)Market Pulp Capacity Ranking 2010(2) (000t)Industry Outlook (1)Industry Outlook (1)

Stora Enso

Sodra

CMPC

Georgia Pacific

APP

Arauco

APRIL

Fibria

Recycled Fiber

224 million t

20% 80%

57% 43%

Paper & Board

392 million t

Pulp

167 million t

Chemical

134 million t

Mechanical

33 million t

5,250

9

0 1000 2000 3000 4000 5000 6000

Cenibra

Canfor

West Fraser

ENCE

IP

Mercer

Ilim

Domtar

UPM-Kymmene

Botnia/M-realSuzano

Bleached Softwood Kraft Pulp (BSKP)

Bleached Hardwood Kraft Pulp (BHKP)

Unbleached Kraft Pulp (UKP)

Mechanical

46% 54%

66% 34%

36% 64%

31%69%

Integrated Mills

85 million t

Market Pulp

46 million t

Hardwood

24 million t

Other Eucalyptus

Pulp producers:

11 million t

Softwood/Other

22 million t

Acacia/Other

8 million t

Eucalyptus

16 million t

(1) RISI and PPPC: considers 2010 demand(2) Hawkins Wright – January 2011 9

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 10/19

Relevant Market Share and Competitive Position in the Cost Curve

Average Cash Cost of BHKP delivered to Europe(2) (US$/t)Average Cash Cost of BHKP delivered to Europe(2) (US$/t)Fibria’s Market Share (1)Fibria’s Market Share (1)

11%

21%

464 500 501 493423 456 426 359 316 310 273

120 70 39 4185 42 33

5769 51

55

200

400

600

800

1000

Mill Cash Delivery SG&A

Maintenance Capex

Financial Expenses

10

Total Hardwood Market Pulp:

24.9 million t

49.8 million t

Total Eucalyptus Market Pulp:

15.8 million t

(1) PPPC– World Chemical Market Pulp Global 100 Report – December 2010 (World Demand by Grade)

(2) Source: Hawkins Wright as July 2011 Report and Fibria 3Q11

33%

10

10 million t

Hardwood Cash Cost (US$/t) vs Capacity ('000 t)

Capacity ('000s t)

200

300

400

500

600700

800

100

C a s h c o s t ( U S $ / t )

5000 10000 15000 20000 25000 30000

Bleached hardwood kraft

0

0

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 11/19

Exchange Rates and Inflation Affect the Cost Structure

Real:90%

Canadian Dollar: 49%

Chilean Peso: 38%

Exchange Rate Currencies Evolution versus Dollar (Index: Jan’03 = 100)Exchange Rate Currencies Evolution versus Dollar (Index: Jan’03 = 100)

120

140

160

180

200

220

240

11

Wood: cost of land and minimum wage growth above inflation

Freight: low governmental investment in infra-structure (ports, roads, etc) and higher oil prices

Chemicals / energy / water: global demand for commodities add pressure on main raw materials

Labor: cost in Brazil in dollar terms is higher than in some developed countries

Rupia: 0%

InflationInflation

60

80

100

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 12/19

Global Presence

4141%%

Fibria’s Commercial StrategyFibria’s Commercial Strategy

Differentiation: Customized pulp products to specific paper grades

Sole supplier to key customers focused on eucalyptus pulp to the tissue market

The top 10 customers represent, on average, 70% of sales

Over 20 years of relationship with many of the main clients

Global contractsTissue

58%P&W

20%

Specialities

22%

End-Use – 3Q11

12

Miami

Nyon Csomád

Hong Kong

São Paulo

2929%%

N.America

1010%%

L.America

Europe

2020%%

Asia

Fibria Sales Distribution Fibria OfficesSource: Fibria – 3Q11

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 13/19

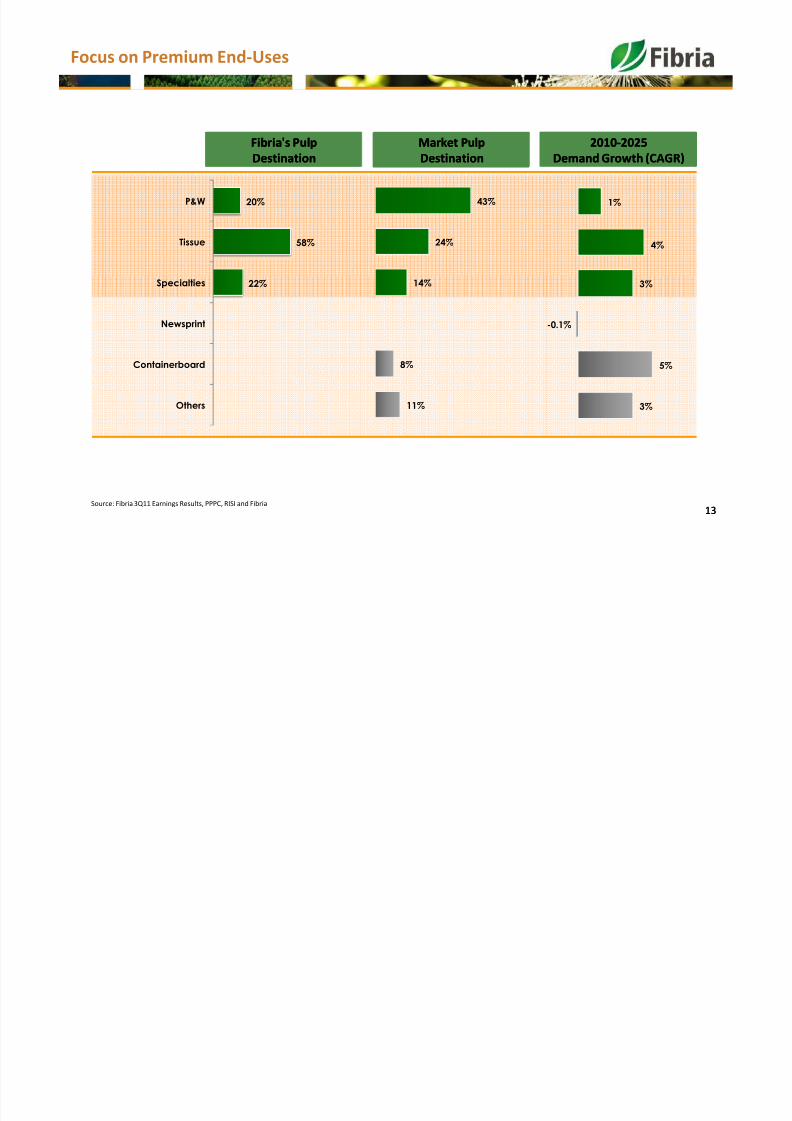

Focus on Premium End-Uses

Fibria'sFibria's PulpPulp

DestinationDestination

Fibria'sFibria's PulpPulp

DestinationDestination

20102010--20252025

DemandDemand Growth (CAGR)Growth (CAGR)

20102010--20252025

DemandDemand Growth (CAGR)Growth (CAGR)

Market PulpMarket Pulp

DestinationDestination

Market PulpMarket Pulp

DestinationDestination

24%

43%

4%

1%

58%

20%

Tissue

P&W

13Source: Fibria 3Q11 Earnings Results, PPPC, RISI and Fibria

13

11%

8%

14%

3%

5%

-0.1%

3%22%

Others

Containerboard

Newsprint

Specialties

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 14/19

Financial Hi hli hts

14

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 15/19

3Q11 Performance

3Q11 Results

3Q11 2Q11 3Q10 3Q11 vs2Q11

3Q11 vs3Q10

Pulp Production (000t) 1,296 1,271 1,293 2% 0%

Pulp Sales (000t) 1,244 1,230 1,160 1% 7%

Net Revenue (R$ million) 1,449 1,459 1,581 -1% -8%

Pro Forma EBITDA1 (R$ million) 476 490 648 -3% -27%

EBITDA Margin (%) 33% 34% 41% -1 p.p. -8 p.p.

Financial Results (R$ million) (2,015) 277 248 - -

46%

29%

14%

11%

2Q11

Euro e North America

41%

27%

20%

12%

3Q10

Sales Mix

41%

29%

20%

10%

3Q11

15

648

490 476

3Q10 2Q11 3Q11

41%

34% 33%

Net Income (Loss) (R$ million) (1,114) 215 303 - -

Cash Cost (R$/t)

435

458446

459

513

481

3Q10 2Q11 3Q11

w/o downtime with downtime

Asia Others

Pro Forma EBITDA1 (R$ million) and EBITDA Margin (%)

3Q11 vs 3Q10

(w/o downtime):

+2.5%

Inflation: +7.3%

1 Excludes Conpacel and KSR results in 3Q10

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 16/19

Market Context Evolution

1,80

1,90

2,00

May/2011:

Indebtedness and Liquidity

Management Policy Approval1

3Q11 FX (R$/US$):

Average: R$ 1.6360

Closing: R$1.8544

Exchange Rate (R$/US$)

Sep/2011:

Macroeconomic Worsening

3Q11 Dollar Appreciation : 19%

FOEX BHKP Europe: US$789/t

Sep

Average FX:

R$1.7399

1.8544

16

1,40

1,50

1,60

1,70FX R US : R 1.6111

FOEX BHKP Europe: US$876/t

1 Indebtedness and Liquidity Management Policy: 2.0 and 2.5x Net Debt/EBITDA target, leverage cap: 3.5x during growth cycle.Policy available on: www.fibria.com.br/ir

Jul-Aug

Average FX:

R$1.5809

1.5345

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 17/19

3,9

3,2

4,2

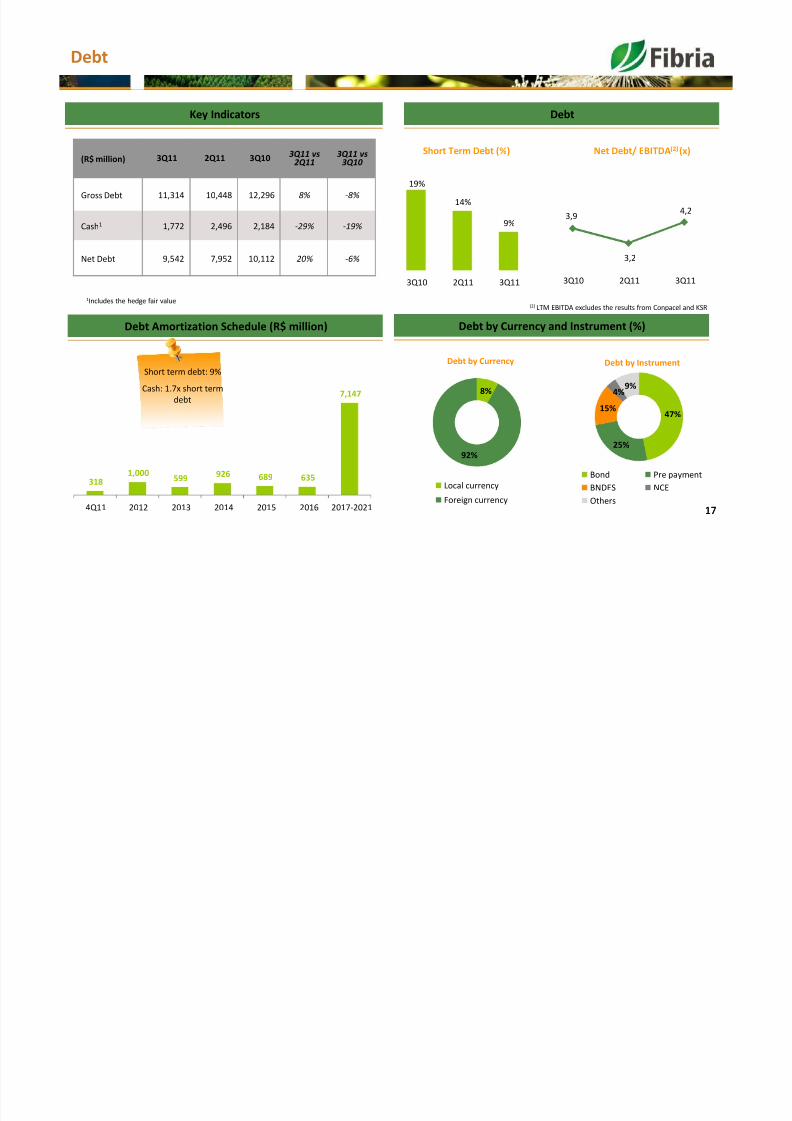

Debt

Short Term Debt (%) Net Debt/ EBITDA(2)(x)

19%

14%

9%

Key Indicators

(R$ million) 3Q11 2Q11 3Q10 3Q11 vs2Q11

3Q11 vs3Q10

Gross Debt 11,314 10,448 12,296 8% -8%

Cash1 1,772 2,496 2,184 -29% -19%

Net Debt 9,542 7,952 10,112 20% -6%

Debt

17

3Q10 2Q11 3Q11

17

3Q10 2Q11 3Q11

3181,000

599926 689 635

7,147

4Q11 2012 2013 2014 2015 2016 2017-2021

Debt Amortization Schedule (R$ million) Debt by Currency and Instrument (%)

Short term debt: 9%

Cash: 1.7x short term

debt

47%

25%

15%4%

9%

Debt by Instrument

Bond Pre payment

BNDES NCEOthers

8%

92%

Debt by Currency

Local currency

Foreign currency

1Includes the hedge fair value(2) LTM EBITDA excludes the results from Conpacel and KSR

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 18/19

Liability Management

15.7

13.2 13.1

Promises delivered, now more ahead to goPromises delivered, now more ahead to go

NetDebt(R$ bi)

Net Debt/EBITDA (x)

7.8

7.2 7.26.5

5.6

4.73.9

3.6

3.2

4.2

18

Fibria’20 Bond: US$ 750MM

7.5% 10NC5

Exchange Bond Fibria’19: 94%

to Fibria’20

Operational cash generation

Derivatives’ debt settlement:

US$ 2.6bn

Debt: lower cost longer tenor

11.0 10.9 10.810.2

9.9

7.9 7.9

9.5

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11

Sale of Guaíba: US$ 1.4bn

Fibria’19 Bond: US$ 1.0bn

9.25% 10NC5

Export pre-payment facilities:

US$ 1.175bn

Sale of Conpacel/KSR: R$ 1.5bn

Fibria’21 Bond Fibria’21: US$ 750MM 6.75% 10NC5

US$ 500MM Revolving facility + US$ 300MM EPP

Covenants: 4.0x YE2011

Tight cost and Capex control

2011 Capex reduced by R$ 201 million

Sale of Piracicaba: US$ 313MM

Commitment to investmentCommitment to investment

gradegrade levellevel

18

.

8/3/2019 Corporativa Dezembro Engl

http://slidepdf.com/reader/full/corporativa-dezembro-engl 19/19

19

Investor Relations

E-mail: [email protected]

Phone: +55 (11) 2138-4565

Website: www.fibria.com.br/ir