apresentação resultados 3 t12 inglês

DESCRIPTION

TRANSCRIPT

1

3Q12 Presentation

Presenters

Marcos Lopes – CEO

Francisco Lopes – COO

Marcello Leone – CFO and IRO

Bruno Gama - COO CrediPronto!

2

This presentation does not constitute or form part of any offer, or invitation or solicitation of any offer to purchase,

sell or subscribe for shares or other securities of the Company, nor shall this presentation or any information

contained herein form the basis of, or act as inducement to enter into, any contract or commitment whatsoever.

This presentation contains financial and other information related to the business operations of Lopes –LPS Brasil

Consultoria de Imóveis S.A and its subsidiaries (“LPS” or the “Company”) as of and for the period ended

September 30th 2012. It should not be considered as a recommendation for prospective investors to sell,

purchase or subscribe for securities of the Company. The information presented herein is in summary form and

does not purport to be complete. No reliance should be placed on the accuracy completeness of the

information contained herein, and no representation or warranty, express or implied, is given on behalf of the

Company or its subsidiaries as to the accuracy completeness of the information presented herein.

This presentation contains forward-looking statements. Investors are advised that whilst the Company believes

they are based on reasonable assumptions by Management, forward-looking statements rely on current

expectations and projections about future events and financial trends, and are not a guarantee of future results.

Forward-looking statements are subject to risks and uncertainties that affect or may affect business conditions

and results of operations, which therefore could materially differ from those anticipated in forward-looking

statements due to several factors, including competitive pressures, Brazilian macroeconomic conditions,

performance of the industry, changes in market conditions, and other factors expressed or implied in these

forward-looking statements or disclosed by the Company elsewhere, factors currently deemed immaterial.

The forward-looking statements contained herein speak only as of the date they are made and neither

Management, nor the Company or its subsidiaries undertake any obligation to release publicly any revision to

these forward-looking statements after the date of this presentation or to reflect the occurrence of unanticipated

events.

Forward-looking statements

3

Schedule

I. Highlights

II. Operational Results

III. Credipronto!

IV. Financial Results

4

Highlights

Highlights

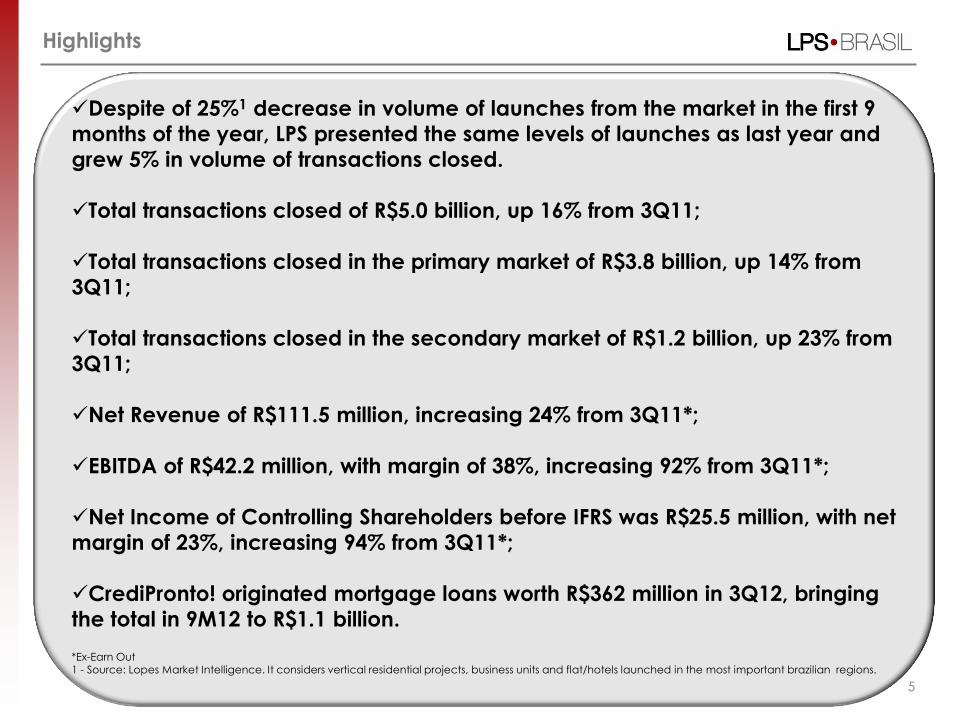

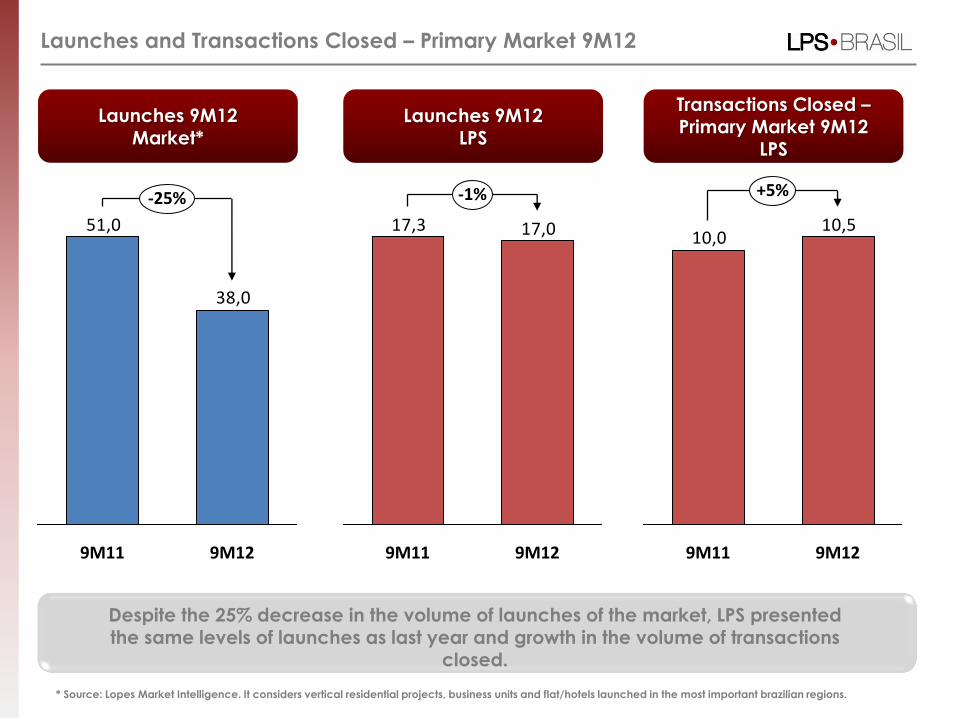

Despite of 25%1 decrease in volume of launches from the market in the first 9

months of the year, LPS presented the same levels of launches as last year and

grew 5% in volume of transactions closed.

Total transactions closed of R$5.0 billion, up 16% from 3Q11;

Total transactions closed in the primary market of R$3.8 billion, up 14% from

3Q11;

Total transactions closed in the secondary market of R$1.2 billion, up 23% from

3Q11;

Net Revenue of R$111.5 million, increasing 24% from 3Q11*;

EBITDA of R$42.2 million, with margin of 38%, increasing 92% from 3Q11*;

Net Income of Controlling Shareholders before IFRS was R$25.5 million, with net

margin of 23%, increasing 94% from 3Q11*;

CrediPronto! originated mortgage loans worth R$362 million in 3Q12, bringing

the total in 9M12 to R$1.1 billion.

*Ex-Earn Out

1 - Source: Lopes Market Intelligence. It considers vertical residential projects, business units and flat/hotels launched in the most important brazilian regions.

5

6

Operational Results

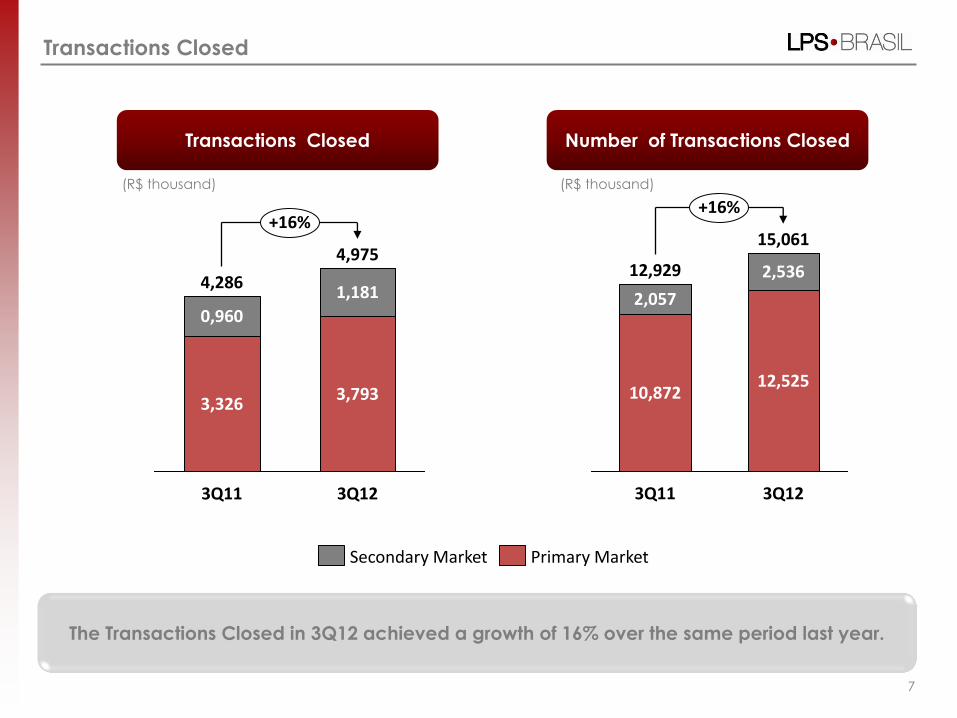

Transactions Closed

(R$ thousand)

Transactions Closed

7

Number of Transactions Closed

+16%

3Q12

4,975

3,793

1,181

3Q11

4,286

3,326

0,960

Primary Market Secondary Market

+16%

3Q12

15,061

12,525

2,536

3Q11

12,929

10,872

2,057

The Transactions Closed in 3Q12 achieved a growth of 16% over the same period last year.

(R$ thousand)

Sales Speed over Supply

Lopes' Consolidated Sales Speed Habitcasa’s Sales Speed

8

3Q12

22.8%

2Q12

20.9%

3Q12

34.7%

2Q12

38.2%

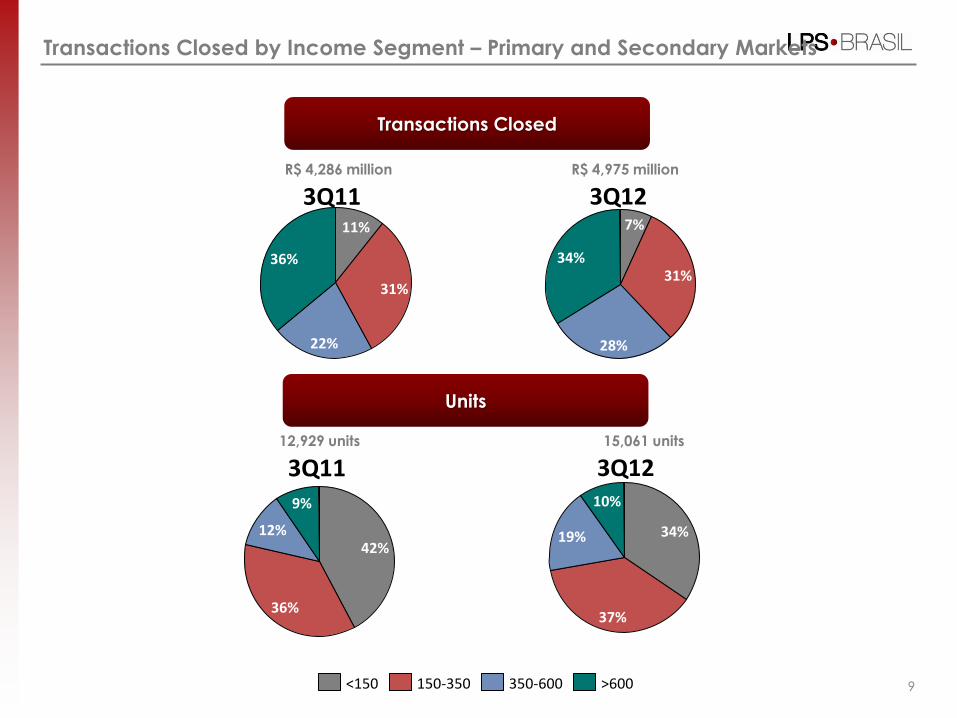

Units

Transactions Closed

9

15,061 units

R$ 4,975 million

Transactions Closed by Income Segment – Primary and Secondary Markets

36%

22%

31%

11%

34%

28%

31%

7%

9%

36%

12% 42%

>600 <150 150-350 350-600

10%

37%

19% 34%

R$ 4,286 million

12,929 units

3Q12

3Q12

3Q11

3Q11

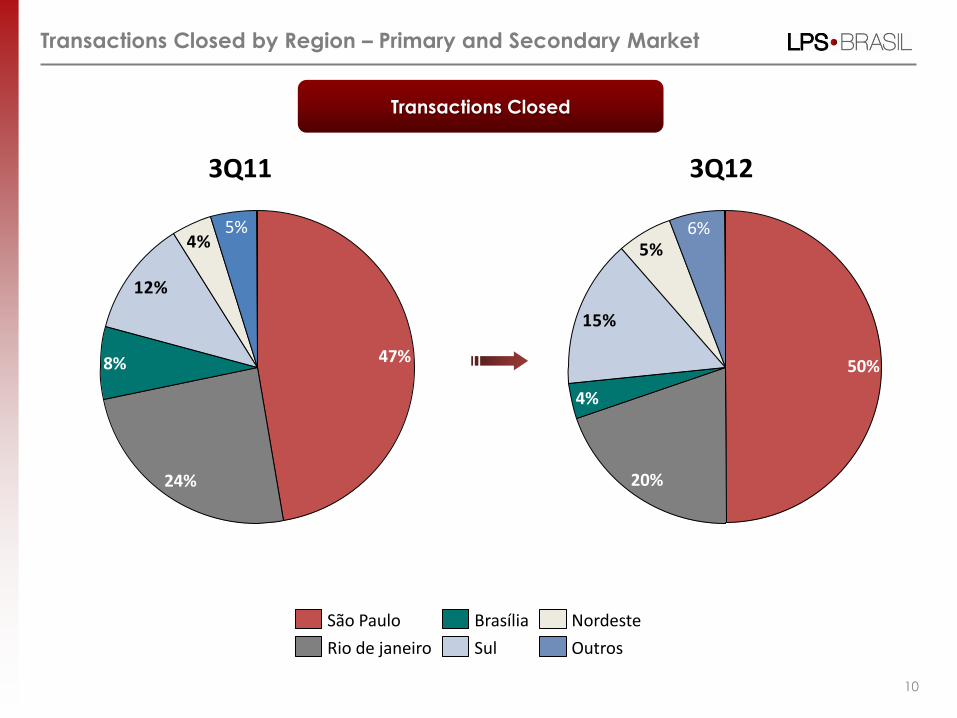

Transactions Closed by Region – Primary and Secondary Market

Transactions Closed

10

4%

12%

8%

24%

47%

5% 5%

15%

4%

20%

50%

6%

Nordeste

Sul

Brasília

Rio de janeiro

São Paulo

Outros

3Q11 3Q12

11

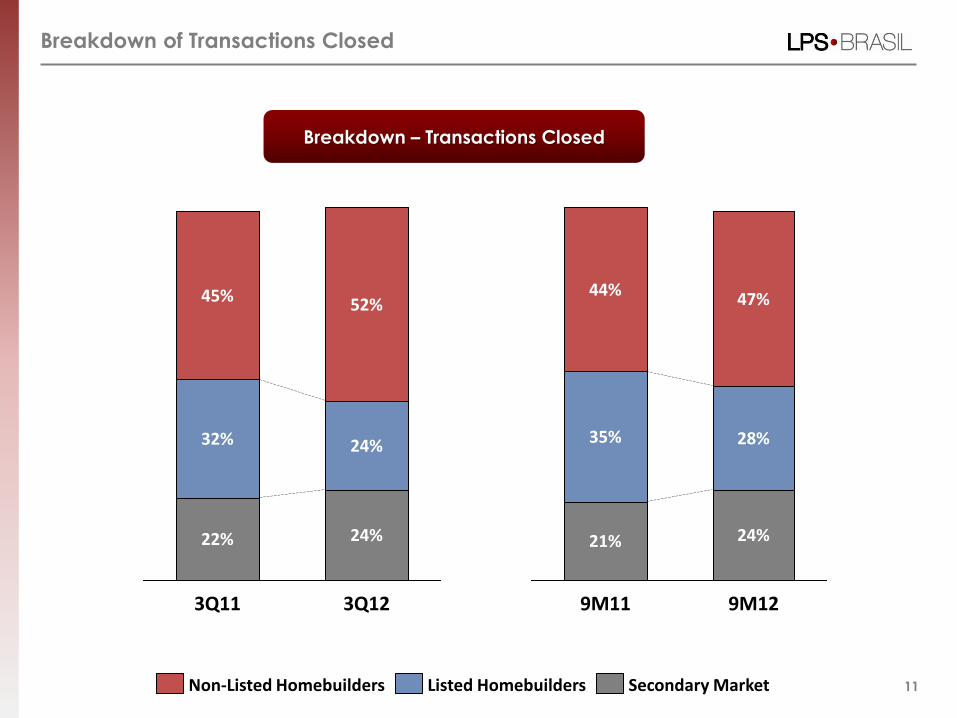

Breakdown of Transactions Closed

Breakdown – Transactions Closed

3Q12

24%

24%

52%

3Q11

22%

32%

45%

9M12

24%

28%

47%

9M11

21%

35%

44%

Secondary Market Listed Homebuilders Non-Listed Homebuilders

38,0

51,0

-25%

9M12 9M11

* Source: Lopes Market Intelligence. It considers vertical residential projects, business units and flat/hotels launched in the most important brazilian regions.

Launches and Transactions Closed – Primary Market 9M12

10,510,0

+5%

9M12 9M11

Launches 9M12 Market*

Transactions Closed – Primary Market 9M12

LPS

Despite the 25% decrease in the volume of launches of the market, LPS presented the same levels of launches as last year and growth in the volume of transactions

closed.

Launches 9M12 LPS

17,017,3

-1%

9M12 9M11

13

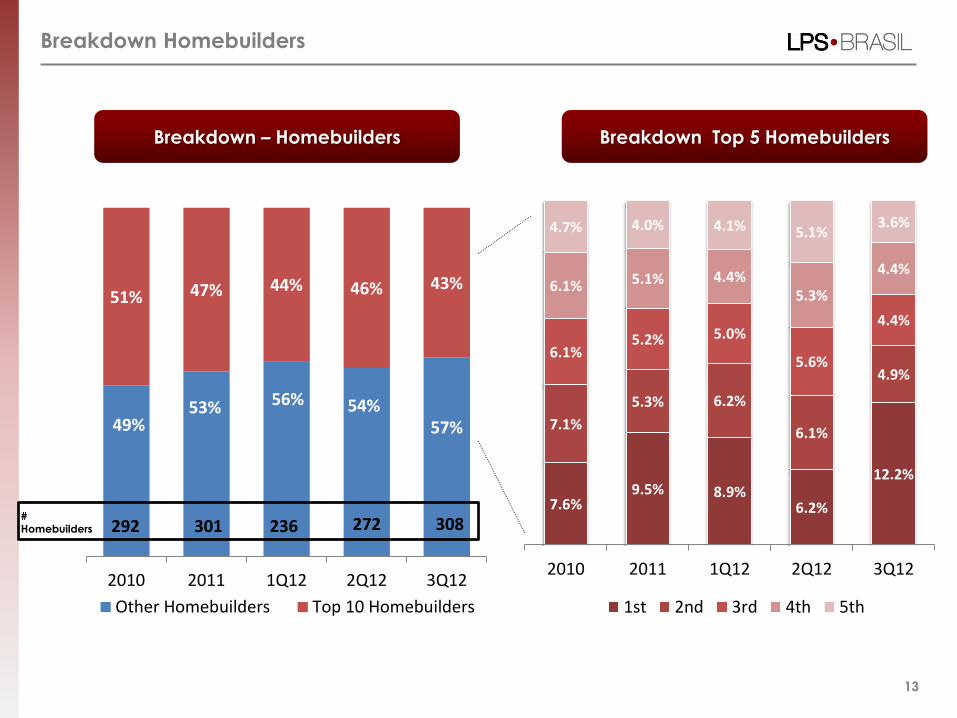

Breakdown Homebuilders

Breakdown Top 5 Homebuilders Breakdown – Homebuilders

49% 53% 56% 54%

57%

51% 47% 44% 46% 43%

2010 2011 1Q12 2Q12 3Q12

Other Homebuilders Top 10 Homebuilders

292 236 301 7.6%

9.5% 8.9% 6.2%

12.2%

7.1%

5.3% 6.2%

6.1%

4.9%

6.1% 5.2% 5.0%

5.6%

4.4%

6.1% 5.1% 4.4% 5.3%

4.4%

4.7% 4.0% 4.1% 5.1% 3.6%

2010 2011 1Q12 2Q12 3Q12

1st 2nd 3rd 4th 5th

# Homebuilders 272 308

LPS Brasil in the Mortgage Market

CrediPronto!

14

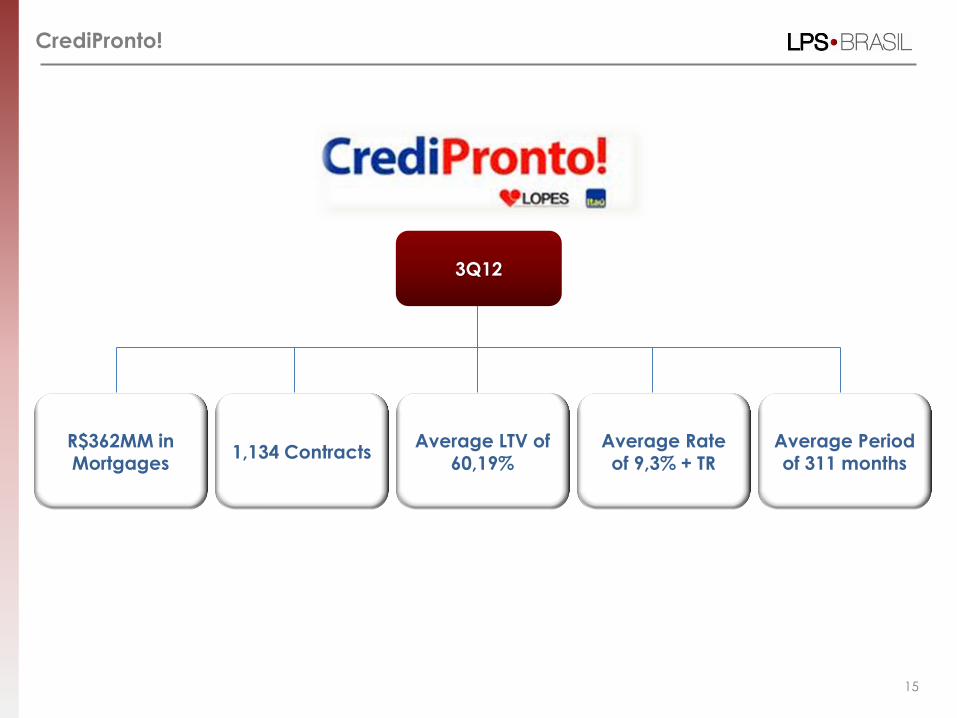

CrediPronto!

15

R$362MM in Mortgages

Average LTV of 60,19%

1,134 Contracts Average Period of 311 months

Average Rate of 9,3% + TR

3Q12

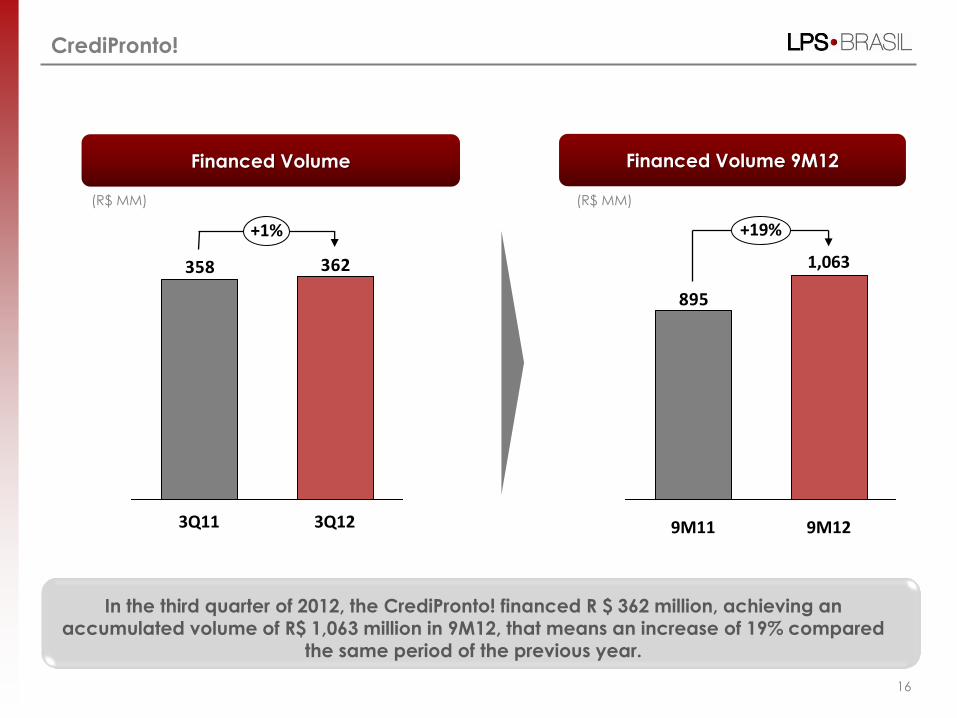

Financed Volume

CrediPronto!

(R$ MM)

16

(R$ MM)

Financed Volume 9M12

In the third quarter of 2012, the CrediPronto! financed R $ 362 million, achieving an accumulated volume of R$ 1,063 million in 9M12, that means an increase of 19% compared

the same period of the previous year.

362358

+1%

3Q12 3Q11

895

+19%

9M12

1,063

9M11

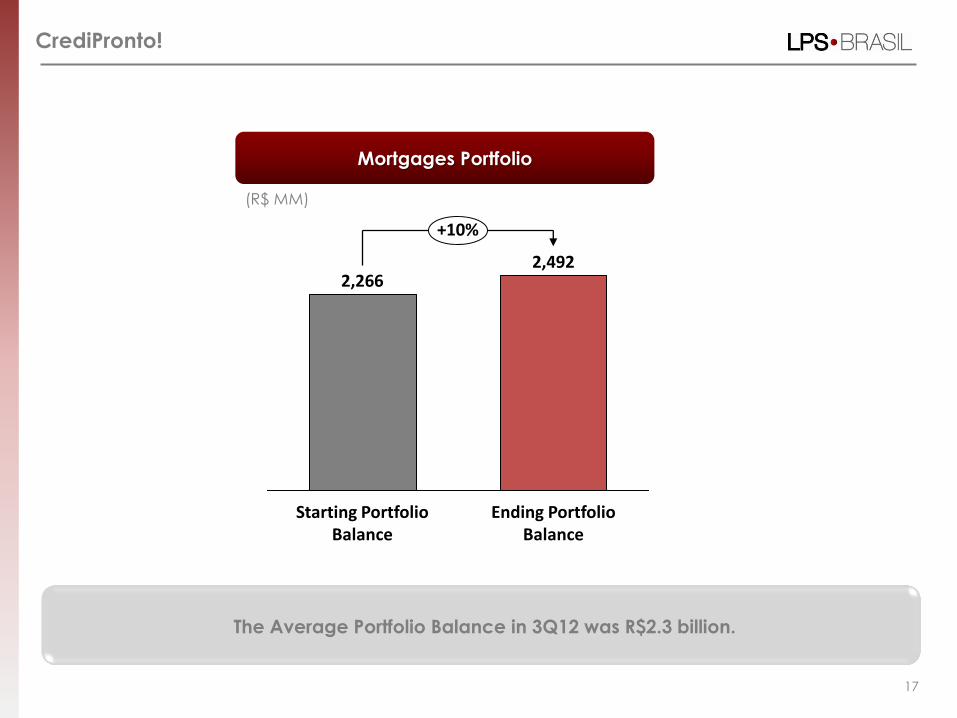

Mortgages Portfolio

CrediPronto!

The Average Portfolio Balance in 3Q12 was R$2.3 billion.

(R$ MM)

17

+10%

Ending Portfolio Balance

2,492

Starting Portfolio Balance

2,266

Ending Portfolio Balance

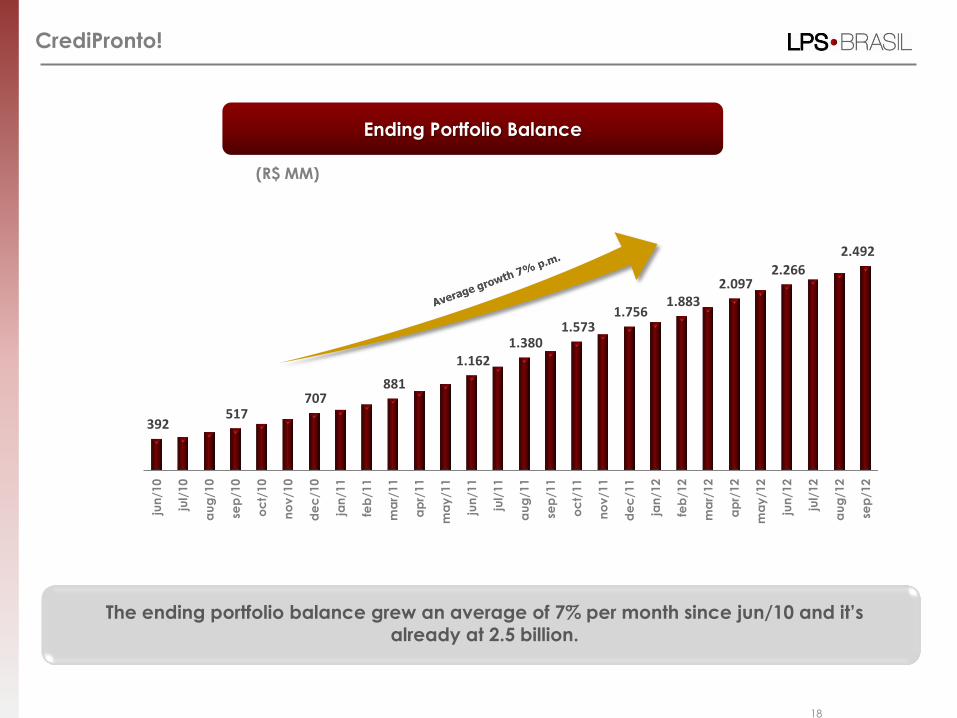

CrediPronto!

(R$ MM)

18

The ending portfolio balance grew an average of 7% per month since jun/10 and it’s already at 2.5 billion.

392 517

707 881

1.162 1.380

1.573 1.756

1.883 2.097

2.266

2.492

jun

/10

jul/

10

au

g/1

0

sep

/10

oc

t/10

no

v/1

0

de

c/1

0

jan

/11

feb

/11

ma

r/11

ap

r/11

ma

y/1

1

jun

/11

jul/

11

au

g/1

1

sep

/11

oc

t/11

no

v/1

1

de

c/1

1

jan

/12

feb

/12

ma

r/12

ap

r/12

ma

y/1

2

jun

/12

jul/

12

au

g/1

2

sep

/12

Financial Results

19

20

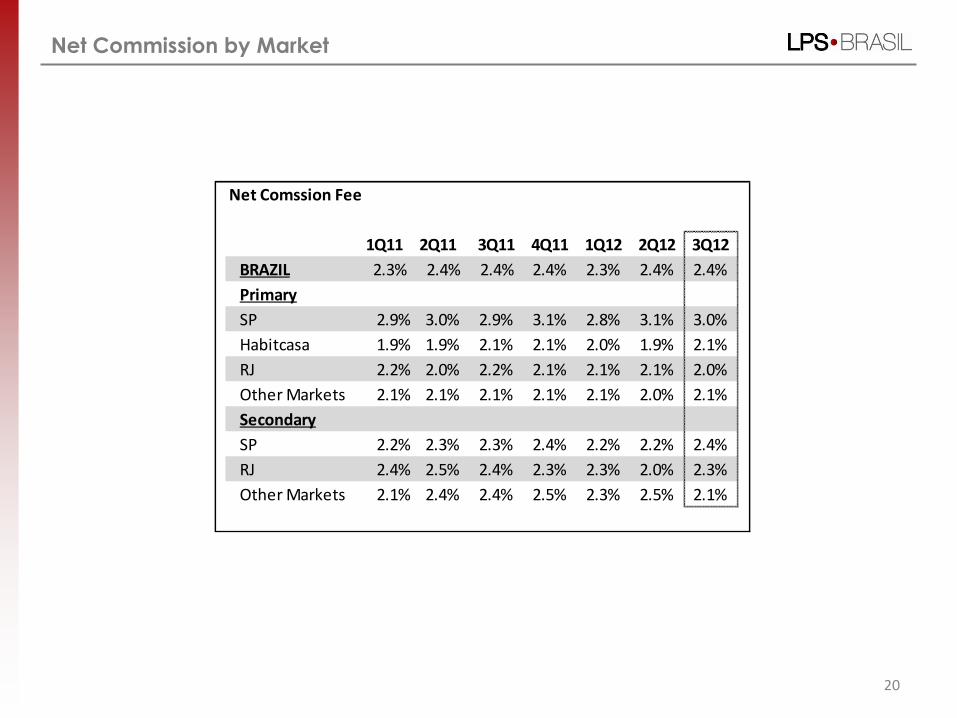

Net Commission by Market

Net Comssion Fee

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12

BRAZIL 2.3% 2.4% 2.4% 2.4% 2.3% 2.4% 2.4%

Primary

SP 2.9% 3.0% 2.9% 3.1% 2.8% 3.1% 3.0%

Habitcasa 1.9% 1.9% 2.1% 2.1% 2.0% 1.9% 2.1%

RJ 2.2% 2.0% 2.2% 2.1% 2.1% 2.1% 2.0%

Other Markets 2.1% 2.1% 2.1% 2.1% 2.1% 2.0% 2.1%

Secondary

SP 2.2% 2.3% 2.3% 2.4% 2.2% 2.2% 2.4%

RJ 2.4% 2.5% 2.4% 2.3% 2.3% 2.0% 2.3%

Other Markets 2.1% 2.4% 2.4% 2.5% 2.3% 2.5% 2.1%

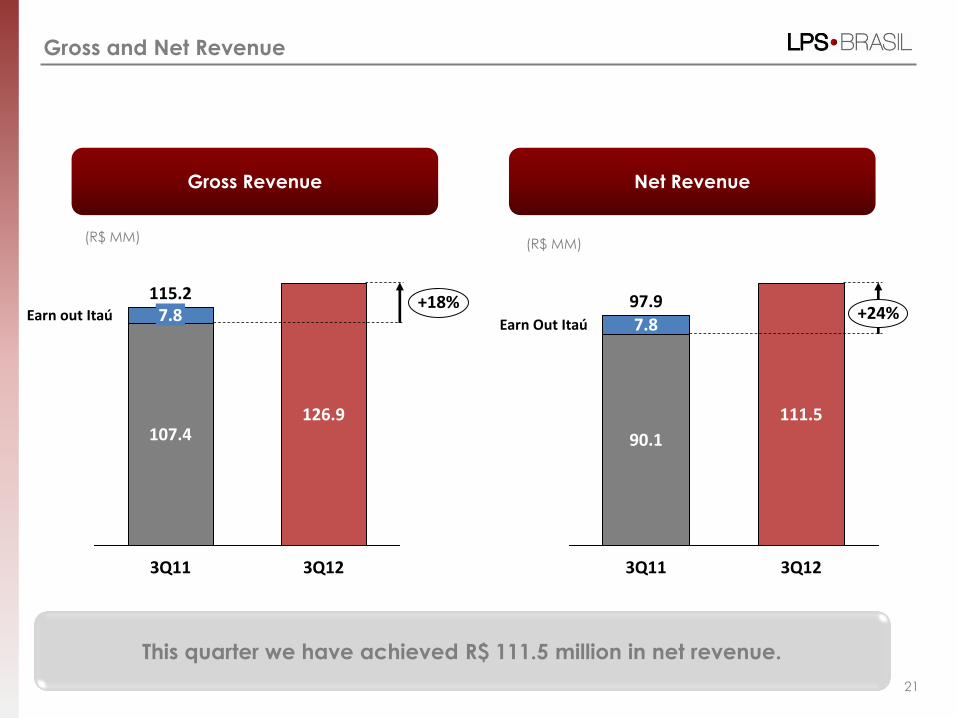

Gross and Net Revenue

Net Revenue

21

(R$ MM)

Gross Revenue

(R$ MM)

This quarter we have achieved R$ 111.5 million in net revenue.

+18% Earn out Itaú

3Q12

126.9

3Q11

115.2

107.4

7.8 +24% Earn Out Itaú

3Q12

111.5

3Q11

97.9

90.1

7.8

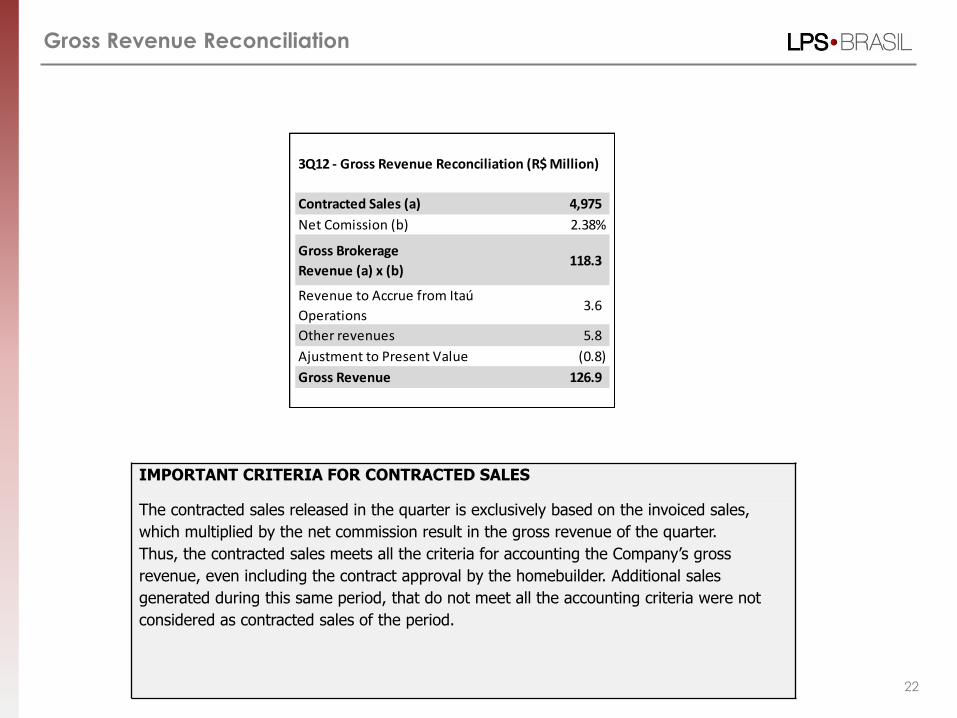

Gross Revenue Reconciliation

IMPORTANT CRITERIA FOR CONTRACTED SALES

The contracted sales released in the quarter is exclusively based on the invoiced sales,

which multiplied by the net commission result in the gross revenue of the quarter.

Thus, the contracted sales meets all the criteria for accounting the Company’s gross

revenue, even including the contract approval by the homebuilder. Additional sales

generated during this same period, that do not meet all the accounting criteria were not

considered as contracted sales of the period.

22

3Q12 - Gross Revenue Reconciliation (R$ Million)

Contracted Sales (a) 4,975

Net Comission (b) 2.38%

Gross Brokerage

Revenue (a) x (b)118.3

Revenue to Accrue from Itaú

Operations3.6

Other revenues 5.8

Ajustment to Present Value (0.8)

Gross Revenue 126.9

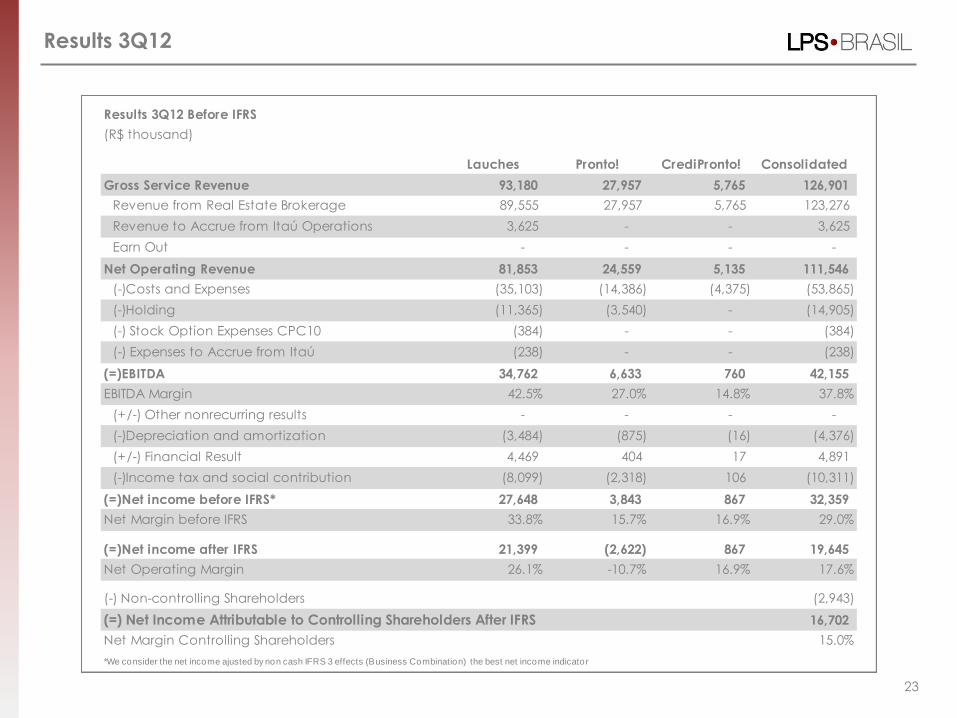

Results 3Q12

23

Results 3Q12 Before IFRS

(R$ thousand)

Lauches Pronto! CrediPronto! Consolidated

Gross Service Revenue 93,180 27,957 5,765 126,901

Revenue from Real Estate Brokerage 89,555 27,957 5,765 123,276

Revenue to Accrue from Itaú Operations 3,625 - - 3,625

Earn Out - - - -

Net Operating Revenue 81,853 24,559 5,135 111,546

(-)Costs and Expenses (35,103) (14,386) (4,375) (53,865)

(-)Holding (11,365) (3,540) - (14,905)

(-) Stock Option Expenses CPC10 (384) - - (384)

(-) Expenses to Accrue from Itaú (238) - - (238)

(=)EBITDA 34,762 6,633 760 42,155

EBITDA Margin 42.5% 27.0% 14.8% 37.8%

(+/-) Other nonrecurring results - - - -

(-)Depreciation and amortization (3,484) (875) (16) (4,376)

(+/-) Financial Result 4,469 404 17 4,891

(-)Income tax and social contribution (8,099) (2,318) 106 (10,311)

(=)Net income before IFRS* 27,648 3,843 867 32,359

Net Margin before IFRS 33.8% 15.7% 16.9% 29.0%

(=)Net income after IFRS 21,399 (2,622) 867 19,645

Net Operating Margin 26.1% -10.7% 16.9% 17.6%

(-) Non-controlling Shareholders (2,943)

(=) Net Income Attributable to Controlling Shareholders After IFRS 16,702

Net Margin Controlling Shareholders 15.0%

*We consider the net income ajusted by non cash IFRS 3 effects (Business Combination) the best net income indicator

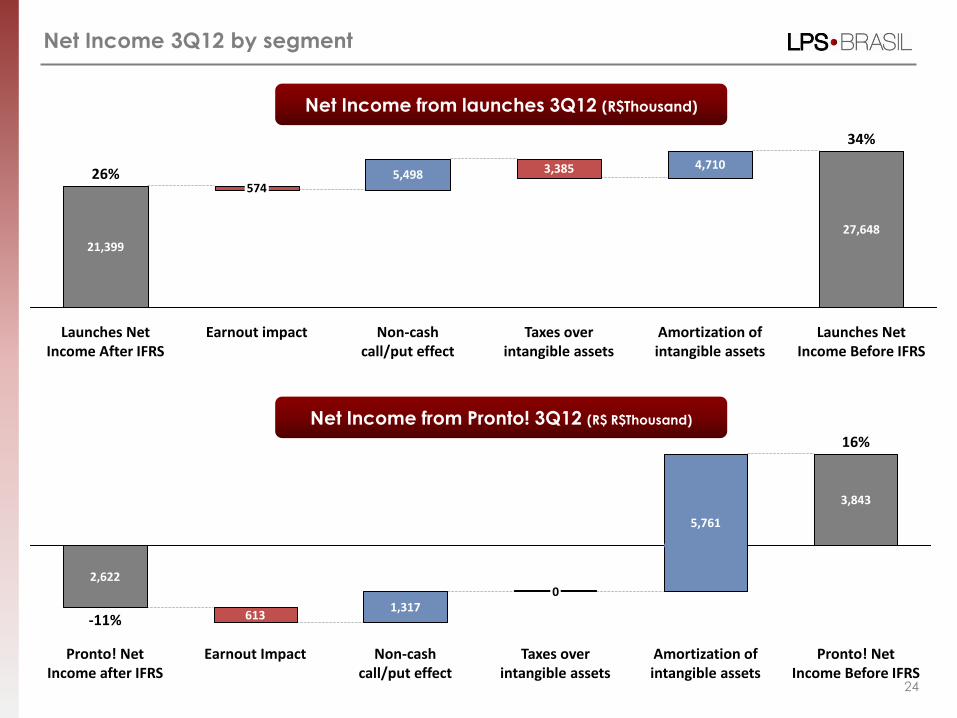

Net Income 3Q12 by segment

24

Launches Net Income Before IFRS

34%

27,648

Amortization of intangible assets

4,710

Taxes over intangible assets

3,385

Non-cash call/put effect

5,498

Earnout impact

574

Launches Net Income After IFRS

26%

21,399

Pronto! Net Income Before IFRS

16%

3,843

Amortization of intangible assets

5,761

Taxes over intangible assets

0

Non-cash call/put effect

1,317

Earnout Impact

613

Pronto! Net Income after IFRS

-11%

2,622

Net Income from launches 3Q12 (R$Thousand)

Net Income from Pronto! 3Q12 (R$ R$Thousand)

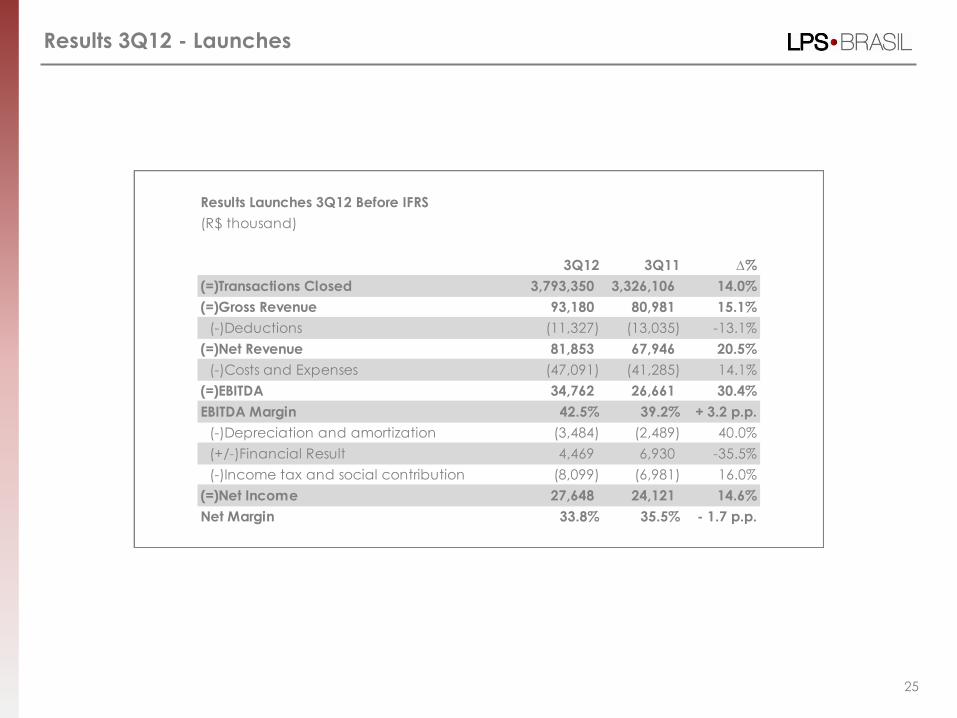

Results 3Q12 - Launches

25

Results Launches 3Q12 Before IFRS

(R$ thousand)

3Q12 3Q11 ∆%

(=)Transactions Closed 3,793,350 3,326,106 14.0%

(=)Gross Revenue 93,180 80,981 15.1%

(-)Deductions (11,327) (13,035) -13.1%

(=)Net Revenue 81,853 67,946 20.5%

(-)Costs and Expenses (47,091) (41,285) 14.1%

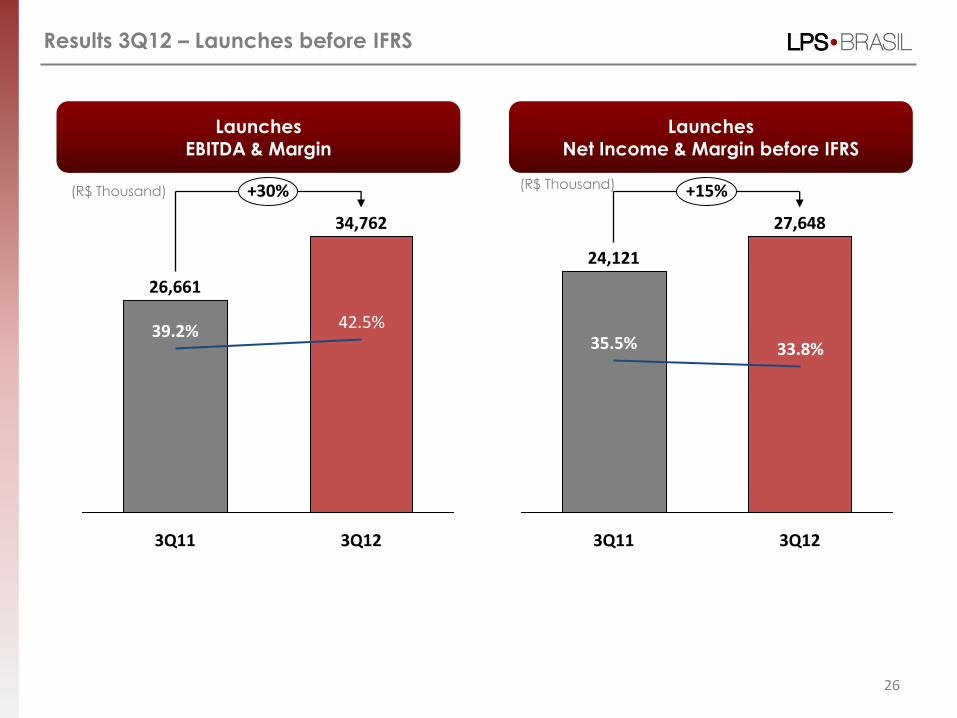

(=)EBITDA 34,762 26,661 30.4%

EBITDA Margin 42.5% 39.2% + 3.2 p.p.

(-)Depreciation and amortization (3,484) (2,489) 40.0%

(+/-)Financial Result 4,469 6,930 -35.5%

(-)Income tax and social contribution (8,099) (6,981) 16.0%

(=)Net Income 27,648 24,121 14.6%

Net Margin 33.8% 35.5% - 1.7 p.p.

26

Results 3Q12 – Launches before IFRS

Launches EBITDA & Margin

Launches Net Income & Margin before IFRS

+15%

3Q12

27,648

33.8%

3Q11

24,121

35.5%

(R$ Thousand) (R$ Thousand) +30%

3Q12

34,762

42.5%

3Q11

26,661

39.2%

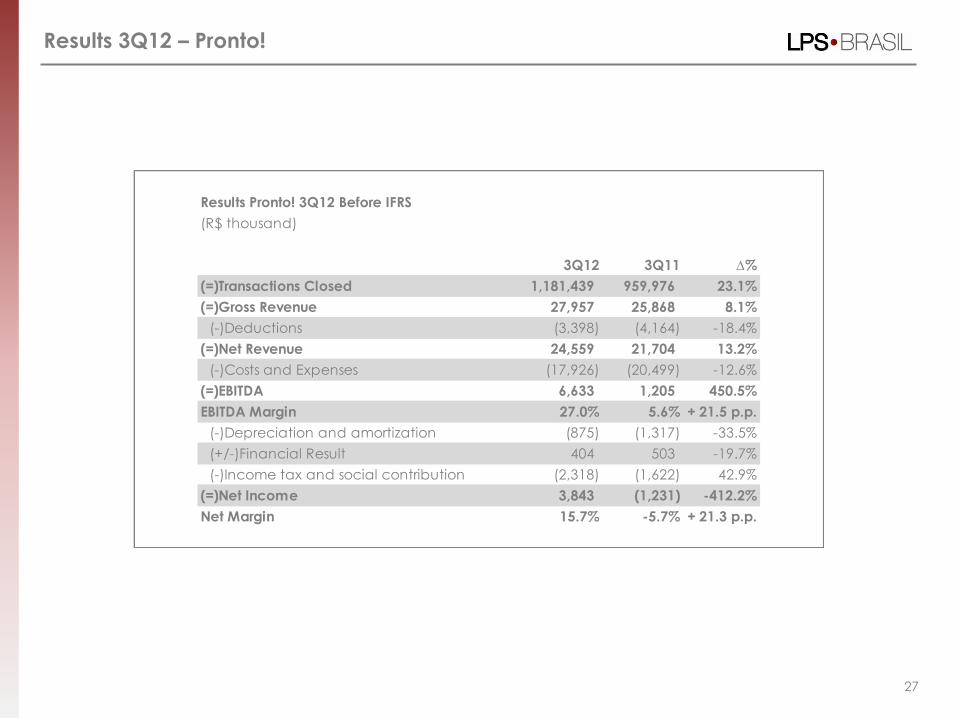

Results 3Q12 – Pronto!

27

Results Pronto! 3Q12 Before IFRS

(R$ thousand)

3Q12 3Q11 ∆%

(=)Transactions Closed 1,181,439 959,976 23.1%

(=)Gross Revenue 27,957 25,868 8.1%

(-)Deductions (3,398) (4,164) -18.4%

(=)Net Revenue 24,559 21,704 13.2%

(-)Costs and Expenses (17,926) (20,499) -12.6%

(=)EBITDA 6,633 1,205 450.5%

EBITDA Margin 27.0% 5.6% + 21.5 p.p.

(-)Depreciation and amortization (875) (1,317) -33.5%

(+/-)Financial Result 404 503 -19.7%

(-)Income tax and social contribution (2,318) (1,622) 42.9%

(=)Net Income 3,843 (1,231) -412.2%

Net Margin 15.7% -5.7% + 21.3 p.p.

28

Results 3Q12 – Pronto! Before IFRS

+450%

3Q12

6,633

27.0%

3Q11

1,205

5.6%

Pronto! EBITDA & Margin

Pronto! Net Income & Margin before IFRS

+412%

3Q12

3,843

15.7%

3Q11

-1,231

-5.7%

(R$ Thousand) (R$ Thousand)

29

Operational Expenses

* Does not consider IFRS

Evolution of Operational Expenses*

(R$ MM) +1%

3Q12

69.4

65.0

4.4

3Q11

68.5

64.8

3.7

Launches + Secondary (Pronto!)

CrediPronto!

Non recurring expenses 3Q12

(R$ million)

M&A Costs 2,0

Consulting Services 0,4

Total 2,4

EBITDA

EBITDA* Margin EBITDA¹(%)

(R$ MM)

30 * We consider the EBITDA, excluding other operating expenses (revenues), that considers IFRS non-cash, as the company

performance indicator

¹ The 2011 margin does not consider Itaú Earn Out net of taxes.

+92%

Earn Out Itaú

3Q12

42.2 (37.8%)

3Q11

29.5

21.9 (24.4%)

7.5

31

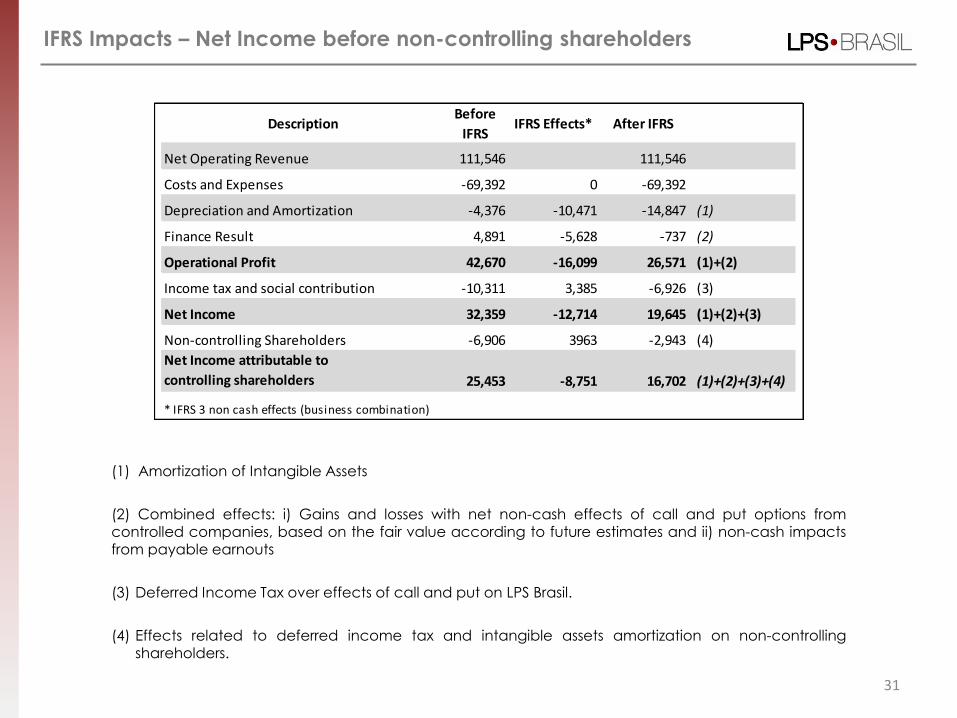

IFRS Impacts – Net Income before non-controlling shareholders

(1) Amortization of Intangible Assets

(2) Combined effects: i) Gains and losses with net non-cash effects of call and put options from controlled companies, based on the fair value according to future estimates and ii) non-cash impacts from payable earnouts

(3) Deferred Income Tax over effects of call and put on LPS Brasil.

(4) Effects related to deferred income tax and intangible assets amortization on non-controlling shareholders.

DescriptionBefore

IFRSIFRS Effects* After IFRS

Net Operating Revenue 111,546 111,546

Costs and Expenses -69,392 0 -69,392

Depreciation and Amortization -4,376 -10,471 -14,847 (1)

Finance Result 4,891 -5,628 -737 (2)

Operational Profit 42,670 -16,099 26,571 (1)+(2)

Income tax and social contribution -10,311 3,385 -6,926 (3)

Net Income 32,359 -12,714 19,645 (1)+(2)+(3)

Non-controlling Shareholders -6,906 3963 -2,943 (4)

Net Income attributable to

controlling shareholders 25,453 -8,751 16,702 (1)+(2)+(3)+(4)

* IFRS 3 non cash effects (business combination)

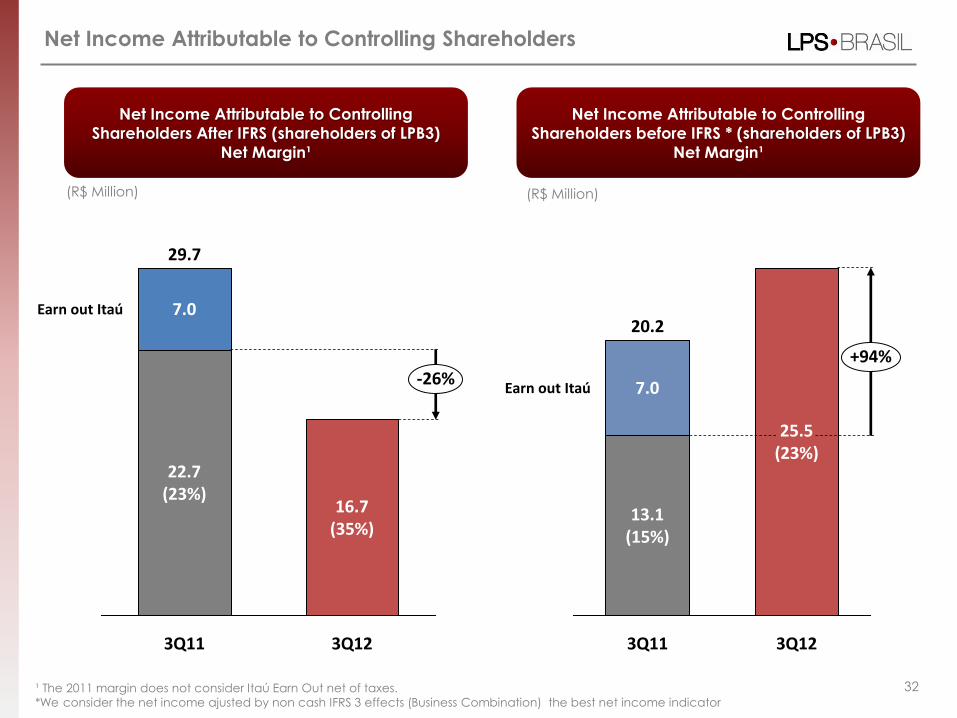

Net Income Attributable to Controlling Shareholders

Net Income Attributable to Controlling

Shareholders After IFRS (shareholders of LPB3)

Net Margin¹

(R$ Million)

32

Net Income Attributable to Controlling

Shareholders before IFRS * (shareholders of LPB3)

Net Margin¹

+94%

Earn out Itaú

3Q12

25.5 (23%)

3Q11

20.2

13.1 (15%)

7.0

(R$ Million)

-26%

Earn out Itaú

3Q12

16.7 (35%)

3Q11

29.7

22.7 (23%)

7.0

¹ The 2011 margin does not consider Itaú Earn Out net of taxes.

*We consider the net income ajusted by non cash IFRS 3 effects (Business Combination) the best net income indicator

3Q12 Earnings Conference Call

Portuguese English

Date: 11/14/2012, Wednesday Date: 11/14/2012, Wednesday

Time: 10h00 a.m. (BR Time) 07h00 a.m. (NY Time)

Time: 12h00 p.m. (BR Time) 09h00 a.m. (NY Time)

Telephone: (11) 2188 0155 Password: Lopes

Telephone Brazil: +55 (11) 2188 0155 Telephone US: (+1) 646 843 6054

Telephone other countries: (+44) 203 051 6929 Password: Lopes

Replay: Replay: http://webcall.riweb.com.br/lpsbrasil/ http://webcall.riweb.com.br/lpsbrasil/english/

CONTACTS

Marcello Leone CFO and IRO

Tel. +55 (11) 3067-0015

IR Tel. +55 (11) 3067-0218

E-mail: [email protected]

www.lopes.com.br/ir

Next Events

33