fgv - rae revista de administração de empresas, 2016. volume 56, número 6

TRANSCRIPT

FÓRUM | FORUM

Varejo: Competitividade e inovaçãoDelane Botelho e Leandro Guissoni

Franchisor-franchisee relationship quality: Time of relationship and performanceLuís Fernando Varotto e Juracy Gomes Parente

Antecedentes da intenção de compra de marcas próprias: Um estudo no mercado emergenteLúcia Aparecida da Silva Borges, Dirceu Tornavoi de Carvalho e Cláudio de Souza Miranda

Os efeitos negativos da experiência e do controle no desempenho do vendedor Juliano Domingues da Silva, Valter da Silva Faia e Valter Afonso Vieira

ARTIGOS | ARTICLES

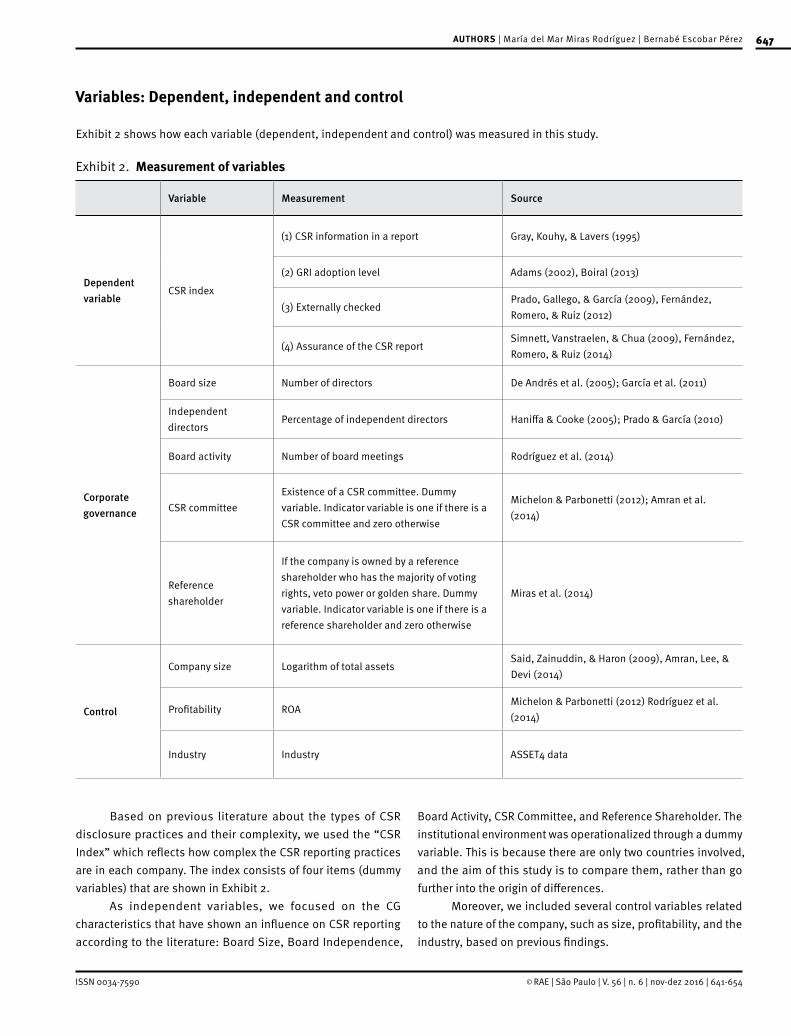

Does the institutional environment affect CSR disclosure? The role of governanceMaría del Mar Miras Rodríguez e Bernabé Escobar Pérez

The mediated effect of formal and informal control on governance formsNuria Rodríguez-López e M. Eva Diz-Comesaña

Creative marketing strategy and effective execution on performance in Pakistan Muhammad Ishtiaq Ishaq e Nazia Munazer Hussain

RESENHA | BOOK REVIEW

Behavioral Finance: Fatores psicológicos e decisões de investimentoThiago de Sousa Barros

INDICAÇÕES BIBLIOGRÁFICAS | BOOK RECOMMENDATIONS

Você é transdisciplinar?Míriam Ribeiro de Barros Shaw

Instituições e seu impacto no desempenho das empresasDavid Kallás

R$ 5

0,00

PESQUISA ECONHECIMENTOV. 56, N. 6,Novembro–Dezembro 2016

www.fgv.br/rae

ISSN 0034-7590www.fgv.br/rae

REDAÇÃOAnalista de Produção Editorial: Denise Francisco Cândido Assistente Administrativa: Eduarda Pereira Anastacio Copidesque (Português e Inglês): Paula Thompson |Márcia Nunes | Editage Tradução e revisão (Espanhol e Inglês): RAG Traduções | Fernando Effori

ADMINISTRAÇÃOResponsável: Ilda Fontes Assistente Administrativa: Eldi Francisca Soares Assistente de Marketing: Andréa Cerqueira Souza Jovem Aprendiz: Nathanael Robson Gouveia

DISTRIBUIÇÃOComunidade acadêmico-científica: 500 exemplaresNúmero de visitas ao site no período setembro-outubro: 44.221 visitantesEXEMPLAR AVULSO: R$ 50,00PONTOS DE VENDA: Livrarias da FGV e Livraria CulturaARTE/EDITORAÇÃO ELETRÔNICATypecomm | Comunicação + Design

PRODUÇÃO INDUSTRIALImpressão e Acabamento: Prol Editora GráficaData de Impressão: 11.11.2016Tiragem: 500 exemplares

PERIODICIDADE: Bimestral

INDEXADORESDOAJ - Directory of Open Access Journalswww.doaj.orgEbsco Publishing: Business Source Complete, Economia y Negocios, Fonte Acadêmicawww.ebscohost.comGale Cengage Learningwww.gale.cengage.comGoogle Scholarscholar.google.com.brOASISBR http://oasisbr.ibict.brPortal de Periódicos CAPESwww.periodicos.capes.gov.brProQuest Information and Learningwww.proquest.com.brREDIB - Red Iberoamericana de Innovación y Conocimiento Científicowww.redib.org/RePEcwww.repec.orgSistema de Información Científica Redalyc - Red de Revistas Científicas de América Latina y el Caribe, España y Portugalredalyc.uaemex.mxSciELO - Scientific Electronic Library Onlinewww.scielo.orgScopus | Elsevierwww.info.sciverse.com/scopusSHERPA/RoMEOwww.sherpa.ac.uk/romeoSPELL – Scientific Periodicals Electronic Librarywww.spell.org.brSumários Brasileiros de Revistas Científicaswww.sumarios.funpeerp.com.brThomson ReutersSSCI, JCRwww.thomsonreuters.comDIRETÓRIOSAcademicKeyswww.academickeys.comCabell’swww.cabells.comCLASE – Citas Latinoamericans en Sciencias Sociales y Humanidadeswww.dgbiblio.unam.mx/index.php/catalogosDiadorimdiadorim.ibict.brIBSS - International Bibliography of the Social Sciencewww.lse.ac.ukHAPI-Hispanic American Periodicals Índexhapi.ucla.eduLatindex - Sistema Regional de Información en Líneapara Revistas Científicas de América Latina, el Caribe,España y Portugalwww.latindex.orgROAD - The Directory of Open Access Scholarly Resourceshttp://road.issn.org/Ulrichs Periodical Directorywww.ulrichsweb.comWorldWideScience.Orghttp://worldwidescience.org/index.html

ATENDIMENTO AO ASSINANTE São Paulo e Grande São Paulo:+ 55 (11) 3799-7999 Fax: + 55 (11) 3799-7871 Av. 9 de Julho, 2029 - 01313 902São Paulo - SP - Brasil

e-mail: [email protected] | site: www.fgv.br/rae

RAE é membro e subscreve os princípios do Committee on Publication Ethics (COPE). http://publicationethics.org/

CORPO EDITORIAL CIENTÍFICOAlexandre de Pádua Carrieri (UFMG - Belo Horizonte - MG, Brasil), Allan Claudius Queiroz Barbosa (UFMG - Belo Horizonte - MG, Brasil), Ana Paula Paes de Paula (UFMG - Belo Horizonte - MG, Brasil), Anatalia Saraiva Martins Ramos (UFRN - Natal - RN, Brasil), André Lucirton Costa (USP/FEA-RP - Ribeirão Preto - SP, Brasil), Andre Luis de Castro Moura Duarte (INSPER - São Paulo - SP, Brasil), Andre Ofenhejm Mascarenhas (Zetesis - Sao Paulo - SP, Brasil), Andrea Lago da Silva (UFSCAR – São Carlos – SP, Brasil), Anielson Barbosa da Silva (UFPB - João Pessoa - PB, Brasil), Antonio Domingos Padula (UFRGS - Porto Alegre - RS, Brasil), Antonio Lopo Martinez (FUCAPE - Vitoria - ES, Brasil), Antonio Moreira de Carvalho (PUC Minas - Belo Horizonte - MG, Brasil), Antonio Navarro-García (Universidad de Sevilla - Sevilha, Espanha), Bento Alves da Costa Filho (Ibmec-DF - Brasília - DF, Brasil), Bill Cooke (University of York - Heslington, Reino Unido), Carlos Jesús Fernández Rodríguez (Universidad Autónoma de Madrid - Madrid, Espanha), Carlos L. Rodriguez (UNCW - Wilimigton - NC, Estados Unidos), Cesar Alexandre de Souza (USP-FEA - São Paulo SP, Brasil), Claudio R. Lucinda (USP/FEA-RP - Ribeirão Preto - SP, Brasil), Dario de Oliveira Lima Filho (UFMS - Campo Grande - MS, Brasil), Delane Botelho (FGV-EAESP - São Paulo - SP, Brasil), Denise Del Prá Netto Machado (FURB - Blumenau - SC, Brasil), Diego Rene Gonzales Miranda (Universidad EAFIT - Medellín, Colômbia), Diogo Henrique Helal (UFPB - Joao Pessoa - PB, Brasil), Domingo Garcia-Perez-de-Lema (UPCT - Cartagena, Espanha), Edgard Barki (FGV-EAESP - São Paulo - SP, Brasil), Edmilson de Oliveira Lima (UNINOVE - São Paulo - SP, Brasil), Eduardo Andre Teixeira Ayrosa (FGV-EBAPE - Rio de Janeiro - RJ, Brasil), Ely Laureano de Paiva (FGV-EAESP - São Paulo - SP, Brasil), Eric David Cohen (Ibmec-Rio - Rio de Janeiro - RJ, Brasil), Eric van Heck (Erasmus University - Rotterdam, Holanda), Fábio Frezatti (USP-FEA - São Paulo - SP, Brasil), Fernanda Finotti Perobelli (UFJF - Juiz de Fora - MG, Brasil), Francisco Javier Rondán Cataluña (Universidad de Sevilla - Sevilla, Espanha), Gláucia Maria Vasconcellos Vale (PUC-Minas - Belo Horizonte - MG, Brasil), Glicia Vieira (UFES - Vitoria - ES, Brasil), Graziela Comini (USP-FEA - São Paulo - SP, Brasil), Graziela Dias Alperstedt (UDESC - Florianópolis - SC, Brasil), Heitor Almeida (College of Business at Illinois - Champaign, Estados Unidos), Henrique Luiz Côrrea (CRUMMER - Flórida - FL, Estados Unidos), Janete Lara de Oliveira (UFMG - Belo Horizonte - MG, Brasil), João Luiz Becker (UFRGS - Porto Alegre - RS, Brasil), Jorge Verschoore (São Leopoldo – RS, Brasil), José Antônio Gomes Pinho (UFBA - Salvador - BA, Brasil), José Henrique de Faria (UFPR - Curitiba - PR, Brasil), José Mauro C. Hernandez (USP-EACH - São Paulo - SP, Brasil), Luciano Barin Cruz (HEC-Montréal - Québec, Canada), Luiz Artur Ledur Brito (FGV-EAESP - São Paulo - SP, Brasil), Maria Alexandra Cunha (FGV-EAESP - São Paulo - SP, Brasil), Maria Ceci Araújo Misoczky (UFRGS - Porto Alegre - RS, Brasil), Mário Aquino Alves (FGV-EAESP - São Paulo - SP, Brasil), Mario Sacomano Neto (UNIMEP - São Paulo - SP, Brasil), Marlei Pozzebon (HEC-Montréal - Québec, Canada e FGV-EAESP - São Paulo - SP, Brasil), Mateus Canniatti Ponchio (ESPM - São Paulo - SP, Brasil), Mauricio Reinert (UEM - Maringá - PR, Brasil), Patricia Mendonça (USP-EACH - São Paulo - SP, Brasil), Paulo Bastos Tigre (UFRJ - Rio de Janeiro - RJ, Brasil), Paulo Roberto Barbosa Lustosa (UnB - Brasília - DF, Brasil), Rafael Alcadipani (FGV-EAESP - São Paulo - SP, Brasil), Rafael Goldszmidt (FGV-EBAPE - Rio de Janeiro - RJ, Brasil), Ramón Valle Cabrera (Universidad Pablo de Olavide - Sevilha, Espanha), Rebecca Arkader (UFRJ - Rio de Janeiro - RJ, Brasil), Ricardo Ratner Rochman (FGV/EESP - São Paulo - SP, Brasil), Roberto Patrus Mundim Pena (PUC-Minas - Belo Horizonte - MG, Brasil), Rodrigo Bandeira-de-Mello (FGV-EAESP - São Paulo - SP, Brasil), Rodrigo Ladeira (UNIFACS - Salvador - BA, Brasil), Salomão Alencar de Farias (UFPE - Recife - PE, Brasil), Sérgio Bulgacov (FGV-EAESP - São Paulo - SP, Brasil), Sérgio Giovanetti Lazzarini (INSPER - São Paulo - SP, Brasil), Silvana Anita Walter (FURB - Blumenau - SC, Brasil), Sônia Maria Fleury (FGV-EBAPE - Rio de Janeiro - RJ, Brasil), Tales Andreassi (FGV-EAESP - São Paulo - SP, Brasil), Teresia D. L. van Ad. de Macedo-Soares (PUC-Rio - Rio de Janeiro - RJ, Brasil), Thomas Brashear Alejandro (University of Massachusetts Amherst - Amherst - MA, Estados Unidos), Vinicius Brei (UFRGS - Porto Alegre - RS, Brasil), Wilson Toshiro Nakamura (MACKENZIE – São Paulo – SP, Brasil).

COMITÊ DE POLÍTICA EDITORIALCarlos Osmar Bertero, Eduardo Diniz, Flávio Carvalho de Vasconcelos, Francisco Aranha, Luiz Artur Ledur Brito, Maria José Tonelli, Maria Tereza Leme Fleury, Tales Andreassi, Thomaz Wood Jr.

EDITORA-CHEFEMaria José Tonelli

EDITOR-ADJUNTOFelipe Zambaldi

EDITORA DE LIVROSRoseli Morena Porto

A RAE - Revista de Administração de Empresas foi impressa com papel proveniente de madeira certificada FSC e de outras fontes controladas. A certificação FSC e uma garantia ao meio ambiente e aos trabalhadores florestais.

Publicação bimestral da Fundação Getulio VargasEscola de Administração de Empresas de São Paulo

Apoio:

PESQUISA E CONHECIMENTO | V. 56, N. 6, NOVEMBRO-DEZEMBRO 2016

RAE – Revista de Administração de Empresas / Fundação Getulio Vargas.Vol. 1, n. 1 (maio/ago. 1961) - . - Rio de Janeiro: Fundação Getulio Vargas, 1961 - v.; 27,5cm.

Quadrimestral: 1961–1962. Trimestral: 1963–1973. Bimestral: 1974–1977.Trimestral: 1978–1992. Bimestral: 1992–1995. Trimestral: 1996–2010.Bimestral: 2011–.

Publicada: São Paulo: FGV-EAESP, 1988–

ISSN 0034-7590

1. Administração de empresas – Periódicos. I. Fundação Getulio Vargas. II. Escola de Administração de Empresas de São Paulo.

A RAE – Revista de Administração de Empresas adota a Licença de Atribuição (CC-BY) do Creative Commons (https://creativecommons.org/licenses/by/4.0/br) em todos os trabalhos publicados, exceto, quando houver indicação específica de detentores de direitos autorais.

CDD 658CDU 658

Novembro/Dezembro 2016

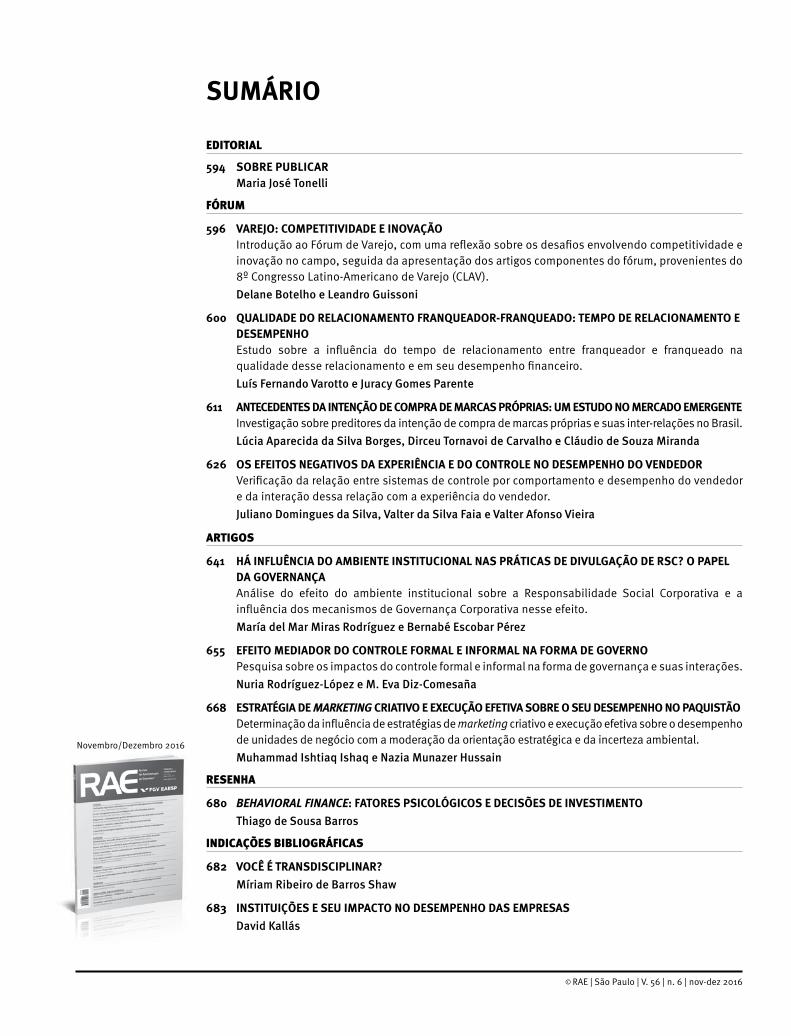

SUMÁRIO

EDITORIAL

594 SOBRE PUBLICAR Maria José Tonelli

FÓRUM

596 VAREJO: COMPETITIVIDADE E INOVAÇÃO Introdução ao Fórum de Varejo, com uma reflexão sobre os desafios envolvendo competitividade e

inovação no campo, seguida da apresentação dos artigos componentes do fórum, provenientes do 8º Congresso Latino-Americano de Varejo (CLAV).

Delane Botelho e Leandro Guissoni

600 QUALIDADE DO RELACIONAMENTO FRANQUEADOR-FRANQUEADO: TEMPO DE RELACIONAMENTO E DESEMPENHO

Estudo sobre a influência do tempo de relacionamento entre franqueador e franqueado na qualidade desse relacionamento e em seu desempenho financeiro.

Luís Fernando Varotto e Juracy Gomes Parente

611 ANTECEDENTES DA INTENÇÃO DE COMPRA DE MARCAS PRÓPRIAS: UM ESTUDO NO MERCADO EMERGENTE Investigação sobre preditores da intenção de compra de marcas próprias e suas inter-relações no Brasil. Lúcia Aparecida da Silva Borges, Dirceu Tornavoi de Carvalho e Cláudio de Souza Miranda

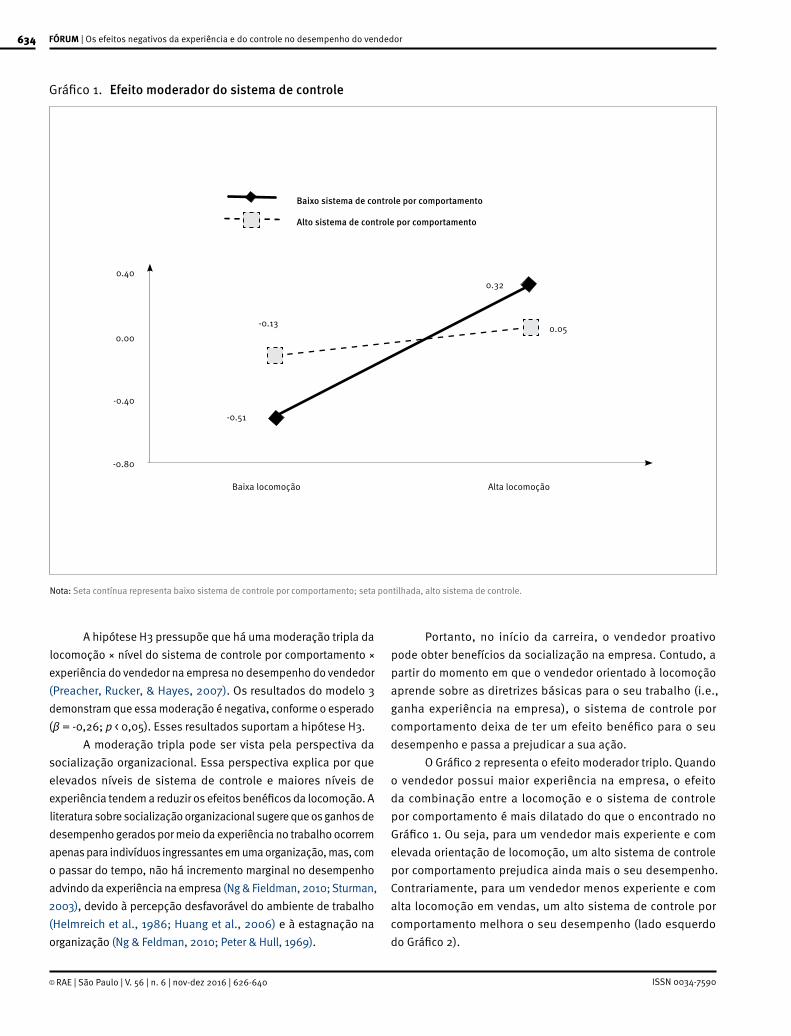

626 OS EFEITOS NEGATIVOS DA EXPERIÊNCIA E DO CONTROLE NO DESEMPENHO DO VENDEDOR Verificação da relação entre sistemas de controle por comportamento e desempenho do vendedor

e da interação dessa relação com a experiência do vendedor. Juliano Domingues da Silva, Valter da Silva Faia e Valter Afonso Vieira

ARTIGOS

641 HÁ INFLUÊNCIA DO AMBIENTE INSTITUCIONAL NAS PRÁTICAS DE DIVULGAÇÃO DE RSC? O PAPEL DA GOVERNANÇA

Análise do efeito do ambiente institucional sobre a Responsabilidade Social Corporativa e a influência dos mecanismos de Governança Corporativa nesse efeito.

María del Mar Miras Rodríguez e Bernabé Escobar Pérez

655 EFEITO MEDIADOR DO CONTROLE FORMAL E INFORMAL NA FORMA DE GOVERNO Pesquisa sobre os impactos do controle formal e informal na forma de governança e suas interações. Nuria Rodríguez-López e M. Eva Diz-Comesaña

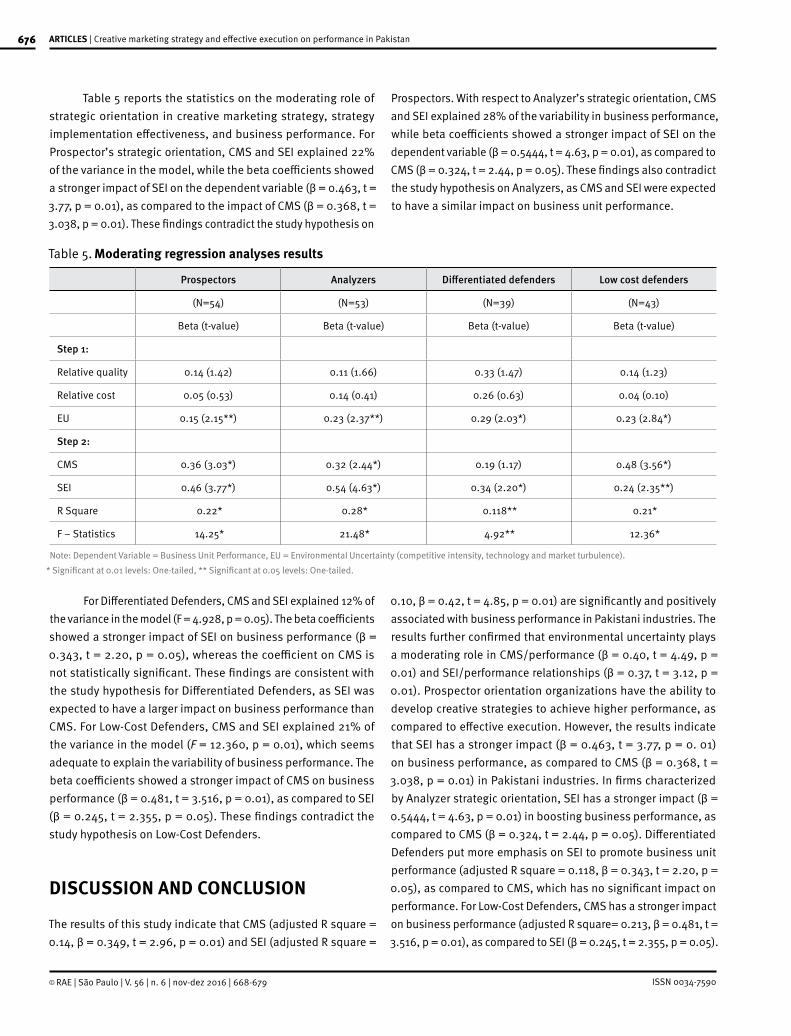

668 ESTRATÉGIA DE MARKETING CRIATIVO E EXECUÇÃO EFETIVA SOBRE O SEU DESEMPENHO NO PAQUISTÃO Determinação da influência de estratégias de marketing criativo e execução efetiva sobre o desempenho

de unidades de negócio com a moderação da orientação estratégica e da incerteza ambiental. Muhammad Ishtiaq Ishaq e Nazia Munazer Hussain

RESENHA

680 BEHAVIORAL FINANCE: FATORES PSICOLÓGICOS E DECISÕES DE INVESTIMENTO Thiago de Sousa Barros

INDICAÇÕES BIBLIOGRÁFICAS

682 VOCÊ É TRANSDISCIPLINAR? Míriam Ribeiro de Barros Shaw

683 INSTITUIÇÕES E SEU IMPACTO NO DESEMPENHO DAS EMPRESAS David Kallás

© RAE | São Paulo | V. 56 | n. 6 | nov-dez 2016

ISSN 0034-7590© RAE | São Paulo | V. 56 | n. 6 | nov-dez 2016

November/December 2016

CONTENTSEDITORIAL

594 ABOUT PUBLISHING Maria José Tonelli

FORUM

596 RETAIL: COMPETITIVENESS AND INNOVATION An introduction to the Fórum de Varejo (Retail Forum) including a reflection about the challenges

involving competitiveness and innovation in the field, followed by the articles comprised in the forum, which were presented in the 8º Congresso Latino-Americano de Varejo (8th Latin American Retail Congress [CLAV]).

Delane Botelho and Leandro Guissoni

600 FRANCHISOR-FRANCHISEE RELATIONSHIP QUALITY: TIME OF RELATIONSHIP AND PERFORMANCE A study about the influence of relationship duration on relationship quality and financial performance

in the franchisee-franchisor relationship. Luís Fernando Varotto and Juracy Gomes Parente

611 PREDICTORS OF STORE BRAND PURCHASE INTENTION: A STUDY IN THE EMERGING MARKET An investigation about predictors of store brand purchase intention and the interrelations between them. Lúcia Aparecida da Silva Borges, Dirceu Tornavoi de Carvalho and Cláudio de Souza Miranda

626 THE NEGATIVE EFFECTS OF EXPERIENCE AND CONTROL ON SALESPERSON’S PERFORMANCE The article examines the relationship between salesperson behavior-based control systems and

salesperson performance, as well as the interaction between that interaction and salesperson experience. Juliano Domingues da Silva, Valter da Silva Faia and Valter Afonso Vieira

ARTICLES

641 DOES THE INSTITUTIONAL ENVIRONMENT AFFECT CSR DISCLOSURE? THE ROLE OF GOVERNANCE An analysis of the effect of institutional environment on corporate social responsibility, as well as

the influence of corporate governance on that effect. María del Mar Miras Rodríguez and Bernabé Escobar Pérez

655 THE MEDIATED EFFECT OF FORMAL AND INFORMAL CONTROL ON GOVERNANCE FORMS A study about the impacts of formal and informal control on governance form and its interactions. Nuria Rodríguez-López and M. Eva Diz-Comesaña

668 CREATIVE MARKETING STRATEGY AND EFFECTIVE EXECUTION ON PERFORMANCE IN PAKISTAN Determining the influence of creative marketing and effective implementation strategies on business

units’ performance, as well as the moderating effects of strategic orientation and environment uncertainty. Muhammad Ishtiaq Ishaq and Nazia Munazer Hussain

BOOK REVIEW

680 BEHAVIORAL FINANCE: PSYCHOLOGICAL FACTORS AND INVESTMENT DECISIONS Thiago de Sousa Barros

BOOK RECOMMENDATIONS

682 ARE YOU MULTIDISCIPLINARY? Míriam Ribeiro de Barros Shaw

683 INSTITUTIONS AND THEIR IMPACT ON THE PERFORMANCE OF COMPANIES David Kallás

ISSN 0034-7590 © RAE | São Paulo | V. 56 | n. 6 | nov-dez 2016

SUMARIO

Noviembre/Diciembre 2016

EDITORIAL

594 SOBRE PUBLICAR Maria José Tonelli

FORO

596 COMERCIO MINORISTA: COMPETITIVIDAD E INNOVACIÓN Introducción al Foro de Comercio Minorista, con una reflexión sobre los desafíos relacionados a la

competitividad e innovación en el campo, seguida de presentación de los artículos que componen el foro, provenientes del 8º Congresso Latino-Americano de Varejo (8º Congreso Latinoamericano de Comercio Minorista [CLAV]).

Delane Botelho y Leandro Guissoni

600 CALIDAD DE LAS RELACIONES FRANQUICIADOR-FRANQUICIADO: TIEMPO DE RELACIONES Y DESEMPEÑO Estudio sobre la influencia del tiempo de relación entre franquiciador y franquiciado en la calidad

de esa relación y en su desempeño financiero. Luís Fernando Varotto y Juracy Gomes Parente

611 ANTECEDENTES DE LA INTENCIÓN DE COMPRA DE MARCAS PROPIAS: UN ESTUDIO EN EL MERCADO EMERGENTE

Investigación sobre predictores de la intención de compra de marcas propias y sus interrelaciones en Brasil. Lúcia Aparecida da Silva Borges, Dirceu Tornavoi de Carvalho y Cláudio de Souza Miranda

626 LOS EFECTOS NEGATIVOS DE LA EXPERIENCIA Y DEL CONTROL EN EL DESEMPEÑO DEL VENDEDOR Verificación de la relación entre sistemas de control por comportamiento y desempeño del vendedor

y de la interacción de esa relación con la experiencia del vendedor. Juliano Domingues da Silva, Valter da Silva Faia y Valter Afonso Vieira

ARTÍCULOS

641 ¿EL ENTORNO INSTITUCIONAL INFLUYE EN LAS PRÁCTICAS DE REVELACIÓN DE INFORMACIÓN DE LA RSC? EL PAPEL DEL GOBIERNO CORPORATIVO

Análisis del efecto del ambiente institucional sobre la Responsabilidad Social Corporativa y la influencia de los mecanismos de Gobernanza Corporativa en ese efecto.

María del Mar Miras Rodríguez y Bernabé Escobar Pérez

655 EFECTO MEDIADOR DEL CONTROL FORMAL E INFORMAL EN LA FORMA DE GOBIERNO Investigación sobre los impactos del control formal e informal en la forma de gobernanza y sus interacciones. Nuria Rodríguez-López y M. Eva Diz-Comesaña

668 ESTRATEGIA DE MARKETING CREATIVO Y EJECUCIÓN EFECTIVA SOBRE SU DESEMPEÑO EN PAQUISTÁN Determinación de la influencia de estrategias de marketing creativo y ejecución efectiva sobre

el desempeño de unidades de negocio con la moderación de la orientación estratégica y de la incertidumbre ambiental.

Muhammad Ishtiaq Ishaq y Nazia Munazer Hussain

RESEÑA

680 BEHAVIORAL FINANCE: FACTORES PSICOLÓGICOS Y DECISIONES DE INVERSIÓN Thiago de Sousa Barros

RECOMENDACIONES BIBLIOGRÁFICAS

682 ¿USTED ES TRANSDISCIPLINARIO? Míriam Ribeiro de Barros Shaw

683 INSTITUCIONES Y SU IMPACTO EN EL DESEMPEÑO DE LAS EMPRESAS David Kallás

594

ISSN 0034-7590© RAE | São Paulo | V. 56 | n. 6 | nov-dez 2016

RAE | Revista de Administração de Empresas | FGV/EAESP

EDITORIALDOI: http://dx.doi.org/10.1590/S0034-759020160601

SOBRE PUBLICAR

O RAEpub, novo manual de publicação da RAE-Revista de Administração de Empresas, traz diretrizes para publi-cação e indica aos autores as principais dimensões que

compõem a avaliação dos artigos submetidos à Revista. Vale retomar sinteticamente o processo: o primeiro passo é dado na triagem inicial realizada pelo editor-chefe, que avalia o poten-cial de publicação do texto e o encaminha, se for o caso, para avaliação dos editores científicos, especialistas na área temáti-ca. Como o campo das Ciências Sociais cresceu enormemente nessas últimas décadas, nós nos tornamos, como diz Boaventu-ra de Souza Santos, “ignorantes especializados”. Por esse mo-tivo, o corpo editorial científico abrange especialistas para essa multiplicidade temática. O segundo passo é dado pelo editor científico, que pode recomendar a rejeição do artigo ou enca-minhá-lo para o processo de blind-review. Essa etapa inclui a avaliação por pareceristas, que sugerem aperfeiçoamento para o artigo, e pode envolver várias rodadas até que ele seja aceito para publicação. O papel dos avaliadores, nesse caso, é suge-rir mudanças que visam, com base na sua experiência e em seu conhecimento, ao aperfeiçoamento do artigo (Rai, 2016), entre-tanto eles não decidem sobre sua aprovação ou rejeição. O edi-tor científico recomenda (ou não) a publicação, e a decisão fi-nal é do editor-chefe. Se aceito, a terceira fase inclui a revisão gramatical.

Esse é o processo, mas qual a importância da avaliação? Afinal, por que é essencial realizá-la? Ao longo dos anos, a co-munidade científica aprimorou a avaliação dos artigos e, conse-quentemente, dos periódicos: bons artigos reforçam a qualida-de dos periódicos, que atraem a submissão de bons artigos. No Brasil, na área de Administração, Turismo e Contabilidade, esse processo se consolidou a partir de 2002, com as diretrizes para avaliação de periódicos da Coordenação de Aperfeiçoamen-to de Pessoal de Nível Superior (Capes) e a participação ativa de diversos professores pesquisadores de todo o país. Ainda que muitos questionem esse processo, em essência, a avalia-ção dos periódicos reforça a busca pela qualidade da produção científica dos programas de pós-graduação (Trzesniak, 2016).

Embora possamos ser repetitivos, quais as qualidades que são valorizadas em artigos científicos? Basicamente, contri-buições para o campo de pesquisa que preencham lacunas teó-ricas após exaustivas e atualizadas revisões da literatura. São considerados os artigos que apresentem um quadro teórico bem

articulado, procedimentos metodológicos claramente descritos, com conclusões relevantes para teoria e prática. Similaridades, evidentemente, devem ser evitadas. Muitos autores reproduzem conteúdo sem a devida citação, em geral dos próprios artigos, o que leva à sua rejeição. Quando se trata de similaridade com dis-sertações, teses ou artigos em congressos, entretanto, o artigo não é rejeitado. Descrito dessa forma, tais critérios parecem sim-ples e objetivos, mas os esforços para obter tais resultados não são fáceis. No primeiro semestre de 2016, foram submetidos 500 artigos à Revista, porém apenas 20 foram aceitos para publica-ção. Isso não deve servir para desestimular, mas sim reafirmar a importância da qualidade da pesquisa. Nunca é demais refor-çar a necessidade de rigor nos procedimentos metodológicos e de revisões teóricas substantivas, que dão sustentação para pes-quisas de qualidade. O rigor, entretanto, não deve matar a cria-tividade, que contribui para o desenvolvimento do conhecimen-to, para a revisão de conceitos cristalizados em verdades e/ou para a solução dos complexos problemas que vivemos (Eisenhar-dt, Graebner, & Sonenshein, 2016).

O último número da RAE apresenta três artigos aprova-dos no Fórum de Varejo, em parceria com o 8º Congresso Lati-no Americano de Varejo (CLAV), selecionados por Delane Bote-lho e Leandro Guissoni. A edição traz outros três artigos, além da resenha sobre o livro “Finanças comportamentais: Quando a economia encontra a psicologia”, de Júlio Lobão, e as indi-cações bibliográficas sobre “transdisciplinaridade” e “institui-ções e desempenho de empresas”.

Boa leitura!

Maria José Tonelli | Editora-chefe

Professora da Fundação Getulio Vargas, Escola de Administração de Empresas de São Paulo – São Paulo – SP, Brasil

REFERÊNCIAS

Eisenhardt, K. M., Graebner, M. E., & Sonenshein, S. (2016). Grand challenges and inductive methods: Rigor without rigor mortis. Academy of Management Journal, 59(4), 1113-1123. doi:10.5465/amj.2016.4004

Rai, A. (2016). Writing a virtuous review. MIS Quarterly, 40(3), 3-10.

Trzesniak, P. (2016). Um Qualis em quatro tempos: Histórico e sugestões para Administração, Ciências Contábeis e Turismo. RC&F-Revista Contabilidade & Finanças, 27(72), 279-290.

ISSN 0034-7590

RAE | Revista de Administração de Empresas | FGV/EAESP 595

© RAE | São Paulo | V. 56 | n. 6 | nov-dez 2016

EDITORIALDOI: http://dx.doi.org/10.1590/S0034-759020160601

ABOUT PUBLISHING

R AEpub, the new publication manual of the RAE-Revista de Administração de Empresas of FGV/EAESP, brings publishing guidelines and shows authors the

main dimensions that form the evaluation process of articles submitted to the Journal. It is worth briefly recalling the process: the first step is the initial selection by the editor-in-chief, who evaluate the text’s publication potential and forwards it, if suitable, for review by the scientific editors, specialists in the thematic area. Because the field of Social Sciences has grown massively in the last few decades, we have become, as Boaventura de Souza Santos says, “specialized ignorants”. Therefore, the editorial body includes specialists for this thematic multiplicity. The second step is taken by the scientific editor, who may recommend rejecting the article or forwarding it to the blind-review process. This phase includes an evaluation by reviewers, who suggest certain improvements to the article, and may even involve various rounds until it is accepted for publication. The role of reviewers, in this case, is to suggest changes that, based on their experience and knowledge, are aimed at improving the article (Rai, 2016); however, they do not decide on its approval or rejection. The scientific editor recommends (or not) its publication, and the editor-in-chief has the final decision. If the article is accepted, the third phase includes a grammar review.

This is the process, but what is the importance of the review? After all, why is it essential to conduct it? Over the years, the scientific community has enhanced the review of articles and, thereby, of journals: good articles reinforce the quality of journals, which attract the submission of good articles. In Brazil, in the area of Administration, Tourism and Accounting, this process has become consolidated since 2002, with the guidelines for periodicals issued by the Coordenação de Aperfeiçoamento de Pessoal de Nível Superior (Capes) and the active participation of various professors engaged in research across the country. Even though many people question this process, in essence, the assessment conducted by periodicals reinforces the pursuit of quality of graduate programs’ scientific production (Trzesniak, 2016).

Although we may sound repetitive, what qualities are appreciated in scientific articles? Basically, contributions to the field of research which can fill theoretical gaps after exhaustive, up-to-date literature reviews. Articles considered for publication

are the ones that present a well articulate theoretical framework, clearly described methodological procedures, and conclusions that are relevant both for theory and practice. Similarities should be avoided. Many authors reproduce contents without proper citation, usually of their own articles, which causes their rejection. When similarities concern dissertations, theses or articles presented at congresses, however, the article is not rejected. Described in this way, these criteria seem simple and straightforward, but the efforts to achieve such results are not easy. In the first semester of 2016, 500 articles were submitted to the Journal, but only 20 were accepted for publication. This should not serve to discourage, but rather reaffirm the importance of research quality. One can never overstress the need of rigor in methodological procedures and substantive theoretical reviews, which underpin quality research. Rigor, however, must not kill creativity, which contributes to developing knowledge, reviewing concepts that have crystalized into truths, and/or solving the complex problems we experience (Eisenhardt, Graebner, & Sonenshein, 2016).

RAE’s latest issue presents three articles approved at the Fórum de Varejo (Retail Forum) in partnership with the 8º Congresso Latino-Americano de Varejo (8th Latin American Retail Congress [CLAV]), selected by Delane Botelho and Leandro Guissoni. The issue brings three other articles, in addition to a review of Júlio Lobão’s book Finanças Comportamentais: Quando a economia encontra a psicologia, and book recommendations on “transdisciplinarity” and “institutions and the performance of companies”.

Enjoy your reading!

Maria José Tonelli | Editor-in-chief

Professor at Fundação Getulio Vargas, Escola de Administração de Empresas de São Paulo – São Paulo – SP, Brazil

REFERENCES

Eisenhardt, K. M., Graebner, M. E., & Sonenshein, S. (2016). Grand challenges and inductive methods: Rigor without rigor mortis. Academy of Management Journal, 59(4), 1113-1123. doi:10.5465/amj.2016.4004

Rai, A. (2016). Writing a virtuous review. MIS Quarterly, 40(3), 3-10.

Trzesniak, P. (2016). Um Qualis em quatro tempos: Histórico e sugestões para Administração, Ciências Contábeis e Turismo. RC&F-Revista Contabilidade & Finanças, 27(72), 279-290.

596

ISSN 0034-7590© RAE | São Paulo | V. 56 | n. 6 | nov-dez 2016 | 596-599

DELANE [email protected] da Fundação Getulio Vargas, Escola de Administração de Empresas de São Paulo – São Paulo – SP, Brasil

LEANDRO [email protected] da Fundação Getulio Vargas, Escola de Administração de Empresas de São Paulo – São Paulo – SP, Brasil

FÓRUMArtigo convidado

VAREJO: COMPETITIVIDADE E INOVAÇÃO8º CONGRESSO LATINO-AMERICANO DE VAREJO (CLAV 2015)“Competitividade e Inovação” foi o tema do 8º Congresso Latino-Americano de Varejo (CLAV) realizado na FGV/EAESP em 29 e 30 de outubro de 2015. Desde 2008, ano do primeiro CLAV, as características principais do congresso têm-se fortalecido: i) discussão científica de temas de varejo com implicações para o mercado; ii) reflexão sobre temas de vanguarda para o vare-jo; iii) interação entre profissionais de mercado e acadêmicos, seja pelo formato de painéis de executivos, como maneira de se colocar em discussão as demandas de conhecimento do mer-cado, seja pela submissão de artigos executivos e casos de ensino; iv) relevância não apenas aos pesquisadores e palestrantes experientes da academia, mas também àqueles que estão iniciando, com o tradicional consórcio doutoral e a banca de iniciação científica para alunos de graduação; v) internacionalização: ao longo destes anos, o CLAV tem priorizado a vinda de pesquisadores reconhecidos na academia internacional, como editores de periódicos de alto impacto no varejo, e a atração de artigos estrangeiros, com sessões de apresentação exclusi-vamente em inglês. Ao longo de sua história, o CLAV tem recebido apoio das três principais agências de fomento brasileiras: Capes, CNPq e FAPESP. A realização do CLAV é do GVcev (Cen-tro de Excelência em Varejo da FGV/EAESP), o qual reúne professores, alunos dos cursos da gra-duação e pós-graduação da FGV/EAESP e de outras instituições de ensino/pesquisa.

Nos últimos anos, o varejo vem sofrendo mudanças expressivas no cenário internacio-nal, o que reflete nas discussões dos profissionais e dos pesquisadores de administração. No contexto de país emergente, deve-se esperar interesse renovado ao varejo, já que esse setor é um catalizador de desenvolvimento não apenas de negócios, mas também dos aspectos so-ciais. Por esse motivo, o CLAV reflete o ambiente acadêmico e de negócios do Brasil e da Amé-rica Latina, proporcionando aos participantes do evento melhor entendimento do varejo, com enfoque nas transições pelo qual o varejo global e nacional vem passando.

COMPETITIVIDADE E INOVAÇÃO NO VAREJOO crescimento nos mercados emergentes tem atraído atenção de consumidores, fabricantes de bens de consumo e varejistas (Kumar, Sunder, & Sharma, 2015). Entretanto, o ambiente de negó-cios no varejo em alguns desses mercados, como o Brasil, tem apresentado momentos de fragilida-de em virtude de problemas econômicos e políticos principalmente a partir de 2014. Gupta, Malho-tra, Czinkota, e Foroudi (2016) sugerem a importância da conexão entre inovação e competitividade, identificando que a competitividade de uma empresa permite que seus gestores inovem nas prá-ticas mercadológicas. Estudos e práticas para essa busca nos mercados consumidores podem im-pactar o resultado de empresas no varejo e potencialmente influenciar o desenvolvimento econômi-co no país, motivando, portanto, a escolha do tema do CLAV-2015 de “Competitividade e Inovação”.

Embora exista consenso de que a inovação envolve aplicação de novas ideias que estimu-lam o desempenho financeiro, o termo apresenta interpretações que dependem do contexto em que ela ocorre. Os conceitos iniciais derivam da teoria econômica ou teoria das organizações e são fundamentados na lógica centrada em manufatura. Inovação na indústria de serviços, incluin-

RAE-Revista de Administração de Empresas | FGV/EAESP

DOI: http://dx.doi.org/10.1590/S0034-759020160602

597

ISSN 0034-7590

AUTORES | Delane Botelho | Leandro Guissoni

© RAE | São Paulo | V. 56 | n. 6 | nov-dez 2016 | 596-599

do o varejo, tem recebido pouca atenção na literatura (Hristov & Reynolds, 2015). Empresas alcançam a vantagem competitiva por meio de iniciativas de inovação, que são manifestadas em novos produtos, serviços, processos ou novas abordagens com base em estratégias e atividades de marketing (Porter, 1990). Defini-ções tradicionais descrevem o varejo como “negócio que vende produtos e serviços para consumidores finais” (Rosenberg, 1993; Levy & Weitz, 1996, p. 419), então o varejo e o escopo de suas ati-vidades parecem simples e muitas vezes tornam a área carente de contribuições sobre como suas organizações podem ser mais competitivas e inovar (Peterson & Balasubramanian, 2002). Al-guns autores (como Pantano, 2014; Hristov & Reynolds, 2015) descrevem os varejistas como adotantes de tecnologias e inova-ção, e não desenvolvedores de novas tecnologias como ocorre em outras indústrias. E a adoção se dá muitas vezes como meio de aumentar sua capacidade de compreensão de mercados e tendências futuras, em vez de prover uma experiência mais va-liosa para o cliente. Ao introduzir uma nova tecnologia, o varejis-ta sempre questiona até que ponto ela seria usada pelo consumi-dor ou o gestor obteria dados para prever tendências ou facilitar sua tomada de decisão. Mas, apesar disso, pesquisas com con-sumidores indicam a sua crescente procura de inovação no pon-to de venda (Cox et al., 2016).

Apesar disso, como qualquer atividade de negócios, o varejo evolui e inova com o tempo. Avanços tecnológicos e mu-danças no comportamento do consumidor, impulsionados pe-los novos dispositivos e pela mídia, continuam a transformá-lo. As mudanças têm sido mais intensas com a disseminação da in-ternet, mídias sociais e aparelhos móveis, provendo aos consu-midores acesso mais fácil a informações e fontes de compras. Clientes mais jovens terão maiores expectativas de usar canais de compras on-line influenciados pelas mídias sociais (Cox et al., 2016). Varejistas têm desenvolvido aplicativos para melho-rar e estender a experiência de compra desses usuários para além da loja física (Grewal, Roggeveen, Runyan, Nordfält, & Lira, in press). Muitos consumidores têm acesso a uma variedade de ferramentas de mídia via smartphones e tablets, que lhes dão acesso instantâneo a blogs e conteúdos e informação, e podem usar aplicativos para encontrar os preços mais baixos ou des-cobrir o que os amigos estão comprando, tornando mais fácil a busca de opções alternativas e tornando-os mais sensíveis aos preços. Uma abordagem da gestão da inovação para o varejo, principalmente para tais clientes, consiste em envolvê-los no novo processo de desenvolvimento de produtos/serviços para melhorar o resultado final e o nível de qualidade. Por isso, mui-tos estudos (Greer & Lei, 2012; Kohler et al., 2011) centram-se em estratégias na participação dos consumidores no processo de cocriação para que seu conhecimento seja aproveitado em

novos produtos (Pantano, 2014), explorando novas tecnologias, principalmente por meio da internet.

Por outro lado, o crescente envelhecimento da popula-ção levará à demanda por mais conveniência e disponibilidade local dos produtos, o que implica que a demanda por loja física de varejo continua (Cox et al., 2016). Mas tal demanda pode ter características experienciais, num novo modelo, em que o pon-to de venda aumenta o envolvimento do cliente, permitindo-lhe interagir com produtos e obter informação sobre a melhor ma-neira de usá-los. Por exemplo, numa loja de móveis, o cliente pode ser capaz de “entrar” nas dimensões de sua sala de estar e ver como o mobiliário novo fica mais bem adequado, podendo mudar virtualmente design, cores e padrões. Essa experiência na loja física, portanto, requer tecnologia e inovação.

Essa combinação de experiências on-line e na loja física remete ao termo multicanalidade. O tema de diversificação de canais em marketing não é novo, mas a evolução no número de canais que devem ser considerados numa estratégia varejista pa-rece ser uma mudança disruptiva (Grewal et al., in press), ainda mais se eles forem usados pelo consumidor de maneira indis-tinta, originando o termo omnichannel. Com a entrada de canais mobile, smartphones e mídias sociais, e com a integração deles e de outros meios ao canal off-line, passa-se da forma multicanal para o modelo de varejo omnichannel. Diferentemente da multi-canalidade, que considera apenas os canais de venda do vare-jo, no ambiente omnichannel, há ênfase na interação entre ca-nais e marcas, ou seja, há interações entre comprador, marca e varejista. Esse novo modelo de negócios, portanto, tem um foco menor no canal utilizado e maior na interação entre o compra-dor e a marca (Verhoef, Kannan, & Inmane, 2015). Adicionalmen-te, tais mudanças são impulsionadas por novos softwares a elas relacionados: aplicativos, pagamentos móveis, cupons digitais, serviços baseados em geolocalização etc. Mas, quando o varejis-ta adiciona novos canais para o cliente, ele também precisa revi-sar ou adicionar novos sistemas de logística para garantir que o produto seja entregue. Inovações como o uso de carros autodiri-gíveis e robotização, por exemplo, já estão sendo usadas para re-duzir custos de entregas e custos operacionais, quando se traba-lha com o conceito de multicanalidade (Cox et al., 2016).

Em termos de multicanalidade, há uma grande oportuni-dade para o varejo brasileiro, e o volume de dados já transacio-nados pelo e-commerce atesta isso. O Brasil é o único país da América Latina que figura entre os dez maiores mercados mun-diais do e-commerce. Se, por um lado, fica claro que o shopper brasileiro está se tornando multicanal, por outro é possível dizer que hoje ele ainda não tem uma experiência completa de compra omnichannel, visto que, de modo geral, os varejistas brasileiros ainda não se adequaram a esse ambiente. Pequenos varejistas,

598

ISSN 0034-7590

FÓRUM | Varejo: Competitividade e inovação

© RAE | São Paulo | V. 56 | n. 6 | nov-dez 2016 | 596-599

por exemplo, geralmente não apresentam presença digital forte, portanto devem se desenvolver no ambiente on-line, enquanto empresas maiores têm de garantir que os consumidores recebam suas ofertas de forma padrão em todos os canais. É em época de crise que as tais oportunidades são vislumbradas em busca de garantir a competitividade atual e futura. O varejo formal brasilei-ro representa apenas 15,5% do produto interno bruto (PIB), sen-do que, em países como Estados Unidos, representa 28%. Isso significa que a maior formalização do varejo deve contribuir para o aumento da participação no PIB, com implicações para a com-petitividade das empresas que atuam no setor.

Sempre haverá os efeitos colaterais da inovação. Mídias so-ciais on-line e móveis, por exemplo, oferecem oportunidades para os varejistas se comunicarem de forma personalizada, principal-mente com os jovens, mas também acarretam desafios associa-dos a potenciais ameaças à privacidade do consumidor (Aguirre, Mahr, Grewal, Ruyter, & Wetzels, 2015). Portanto, tais inovações re-querem transparência sobre quando e como os dados do consu-midor são coletados. A disseminação das práticas de personali-zação da comunicação faz com que os consumidores sejam mais conscientes de que as empresas coletam suas informações on-line e off-line. Isso provavelmente provoca maior ceticismo em relação ao varejista, o que pode ser problemático numa época em que há também uma crise de confiança entre consumidores e empresas.

Em se tratando de inovação no varejo, o setor também tem papel importante nas questões de sustentabilidade, em razão de seu poder econômico global e sua posição privilegiada entre ofer-ta e demanda. Os varejistas podem influenciar tanto a produção quanto os padrões de consumo (Delai & Takahashi, 2013). Tam-bém podem influenciar em suas cadeias de abastecimento como resultado de suas estratégias de sustentabilidade, moldando de-cisões e atividades, como o desenvolvimento de novos produtos, estratégias de recursos humanos, aspectos de distribuição e pa-drões de embalagem. No lado da demanda, os varejistas podem influenciar os consumidores no modo como eles compram, usam e descartam os produtos. Nessa perspectiva, a pesquisa em vare-jo tem evoluído e também buscado oferecer contribuições para a competitividade das organizações envolvidas, com potencial im-pacto no desenvolvimento econômico no país, principalmente com a preocupação atual sobre os problemas econômicos e políti-cos citados aqui. Portanto, o propósito do CLAV 2015 foi criar con-dições para discutir contribuições para a literatura sobre compe-tividade e inovação no varejo, assim como para as organizações de varejo e seus consumidores, com artigos apresentados em di-versas trilhas acadêmicas: estratégias varejistas, eficiência e tec-nologia, fator humano nas organizações varejistas, relacionamen-to, parcerias e suplly chain, responsabilidade e sustentabilidade e comportamento do consumidor.

FÓRUM RAE DE VAREJO – ARTIGOS

Como já é de costume, os melhores artigos do CLAV-2015 em avaliação double blind review são considerados para publica-ção no Fórum RAE de Varejo. Este fórum discute assuntos re-lacionados ao tema “Competitividade e Inovação” e apresenta estudos que contribuem tanto para a literatura quanto para as práticas varejistas.

A relação entre competitividade e inovação contribui para que as organizações varejistas aperfeiçoem os modelos de ne-gócio ou levam a propor novos modelos que as tornem mais lu-crativas, prósperas e gerem valor aos stakeholders mesmo em momento adverso, como mencionado em relação ao Brasil. Em relatório sobre o varejo no Brasil, a Euromonitor (2016) indica um modelo de negócios no varejo que tem crescido mesmo em am-biente turbulento: o de franquias, que apresentou em 2015 au-mento de 8% de faturamento e 10% no número de lojas franquea-das em relação ao ano de 2014, incluindo 131 novas marcas que adotaram o modelo em 2015. O artigo “Franchisor-franchisee re-lationship quality: Time of relationship and performance”, de Va-rotto e Parente (2016), analisa, com base em 342 franqueados, como o relacionamento entre franqueadores e franqueados se desenvolve ao longo do tempo e de que maneira esse processo influencia a qualidade de relação e o desempenho financeiro na questão franqueador-franqueado. Os resultados indicam que o tempo tem efeito moderador positivo nesse aspecto e apresen-tam implicações para a prática na gestão de franquias, pois os franqueadores devem buscar desenvolver iniciativas que permi-tam sustentar a relação depois do seu estágio inicial, chamado de honeymoon, após o primeiro ano de relacionamento, e o cui-dado com o estágio crossroads, após oito anos.

A necessidade de que as organizações varejistas sejam inovadoras, produtivas e alcancem níveis satisfatórios de com-petitividade é mais evidente em períodos de adversidades no ambiente econômico. Conforme relatório apresentado pela Mckinsey (Donatelli, Hoefel, Resstom, & Stul, 2016) e que foi desenvolvido com a proposta de investigar o comportamento do consumidor em época de desaceleração da economia, os consumidores no Brasil têm buscado economizar em suas com-pras no varejo e passam a prestar mais atenção em preços e promoções de produtos. Quando objetivam manter o consumo de suas marcas preferidas, buscam varejistas que as ofereçam com preço menor, porém, mais da metade dos consumidores que já optaram por marcas de menores preços alega que não tem intenção de voltar a consumir as marcas mais caras. Se-gundo a mesma pesquisa, apenas 18% dos clientes que opta-ram por marcas mais baratas compraram marcas próprias dos varejistas, enquanto na América Latina, em geral, o resultado

599

ISSN 0034-7590

AUTORES | Delane Botelho | Leandro Guissoni

© RAE | São Paulo | V. 56 | n. 6 | nov-dez 2016 | 596-599

foi de 26% e em países classificados como maduros chega a 60%. Isso é explicado pela baixa representatividade das mar-cas próprias no Brasil. Contudo, é esperado aumento de inova-ções de marca própria e do seu papel no varejo brasileiro. O ar-tigo “Antecedentes da intenção de compra de marcas próprias: Um estudo no mercado emergente”, de Borges, Carvalho, e Mi-randa (2016), explora preditores da intenção de compra de mar-cas próprias com base na imagem da loja, no risco percebido e na atitude em relação a elas. Os resultados mostram que o ris-co percebido e a imagem da loja são fortes preditores da ima-gem da marca própria. O primeiro construto (risco percebido) inclui variáveis de risco de desempenho e financeiro. O segun-do construto (imagem da loja) compreende variáveis como qua-lidade do produto, sortimento e atmosfera de loja. Como im-plicação para varejistas que gerenciam suas marcas próprias, o estudo identifica que, melhorando esses fatores menciona-dos, a atitude e a intenção de compra desses produtos podem ser influenciadas positivamente, o que contribui para sua com-petitividade.

Uma das atividades que muitas vezes executivos que atuam no varejo consideram a mais relevante para a competiti-vidade das organizações envolve a gestão de pessoas, incluin-do equipes e pessoal para dar suporte a vendas e ao atendi-mento ao consumidor final. Especificamente, os sistemas de incentivo e controle dos vendedores podem influenciar a satis-fação dos consumidores e o desempenho de vendas da organi-zação (Kraus, Haumann, Ahearne, & Wieseke, 2015). No artigo “Os efeitos negativos da experiência e do controle no desem-penho do vendedor”, Silva, Faia, e Vieira (2016) identificam a relação entre o perfil de locomoção do vendedor, isto é, da proatividade do vendedor, e o desempenho de vendas a par-tir da proposta de investigação sobre os efeitos do sistema de controle por comportamento, incluindo como as organizações monitoram, controlem, avaliam e compensam os vendedores. Como resultado da pesquisa empírica com base nos dados de 138 vendedores no varejo, os autores mostram que o alto nível do sistema de controle por comportamento reduz o efeito en-tre a orientação para locomoção do vendedor e seu desempe-nho. Como implicação para o varejo, os autores sugerem que os gestores de vendedor no varejo proporcionem oportunidades para que eles expressem suas opiniões e participem de estra-tégias e ações de vendas. Ainda, identificam que, com o passar do tempo e de acordo com a experiência do vendedor, os ges-tores devem flexibilizar as normas rígidas de controle por com-portamento e inserir mecanismos de controle diversos, como o sistema de controle por resultados.

Esperamos que este Fórum RAE estimule pesquisas adi-cionais no varejo sobre os vários tópicos aqui identificados.

REFERÊNCIASAguirre, E., Mahr, D., Grewal, D., de Ruyter, K., & Wetzels, M. (2015). Unrav-

eling the personalization paradox: The effect of information collection and trust-building strategies on online advertisement effectiveness. Journal of Retailing, 91(1), 34-49. doi:10.1016/j.jretai.2014.09.005

Borges, L. A. da S., Carvalho, D. T., & Miranda, C. de S. (2016). Anteceden-tes da intenção de compra de marcas próprias: Um estudo no mercado emergente. RAE-Revista de Administração de Empresas, 56(6), 611-625. doi:10.1590/S0034-759020160604

Cox, A., Hay, G., Econometrics, C., Hogarth, T., Brown, G., Writing, G. B., & Limmer, H. (2016). Productivity in the retail sector: Challenges and op-portunities. Recuperado de http://www.employment-studies.co.uk/system/files/resources/files/ukces0816d.pdf

Delai, I., & Takahashi, S. (2013). Corporate sustainability in emerging mar-kets: Insights from the practices reported by the Brazilian retailers. Jour-nal of Cleaner Production, 47, 211-221. doi:10.1016/j.jclepro.2012.12.029

Donatelli, M., Hoefel, F., Resstom, S., & Stul, F. (2006, jun.). Meet the new Brazilian consumer. Mckinsey Consumer Packaged Goods and Retail. Recuperado de www.mckinsey.com/industries/consumer-pack-aged-goods/our-insights/meet-the-new-brazilian-consumer

Euromonitor International Report. (2016, abr.). Retailing in Brazil. Recupe-rado de http://www.euromonitor.com/retailing-in-brazil/report

Grewal, D., Roggeveen, A. L., Runyan, R. C., Nordfält, J., & Lira, M. E. V. (in press). Retailing in today’s world: Multiple channels and oth-er strategic decisions affecting firm performance. Journal of Retail-ing and Consumer Services. Recuperado de http://ac.els-cdn.com/S0969698916000023/1-s2.0-S0969698916000023-main.pdf?_tid=6bd10618-a4e5-11e6-a258-00000aab0f27&acdnat=1478521774_f85f5389cfaf648d960b2d87e0fed58c

Grewal, D., & Levy, M. (2009). Emerging issues in retailing research. Journal of Retailing, 85(4), 522-526. doi:10.1016/j.jretai.2009.09.007

Gupta, S., Malhotra, N. K., Czinkota, M., & Foroudi, P. (2006). Marketing innovation: A consequence of competitiveness. Journal of Business Re-search, 69(12), 5671-5681. doi:10.1016/j.jbusres.2016.02.042

Hristov, L., & Reynolds, J. (2015). Perceptions and practices of innovation in retailing: Challenges of definition and measurement. International Jour-nal of Retail & Distribution Management, 43(2), 126-147. doi:10.1108/ijrdm-09-2012-0079

Kraus, F., Haumann, T., Ahearne, M., & Wieseke, J. (2015). When sales man-agers and salespeople disagree in the appreciation for their firm: The phenomenon of organizational identification tension. Journal of Retail-ing, 91(3), 486-515. doi:10.1016/j.jretai.2015.03.001

Kumar, V., Sunder, S., & Sharma, A. (2015). Leveraging distribution to max-imize firm performance in emerging markets. Journal of Retailing, 91(4), 627-643. doi:10.1016/j.jretai.2014.08.005

Levy, M., & Weitz, B. (1996). Essentials of retailing. Boston, EUA: Irwin Mc-Graw-Hill.

Pantano, E. (2014). Innovation drivers in retail industry. International Jour-nal of Information Management, 34(3), 344-350. doi:10.1016/j.ijinfo-mgt.2014.03.002

Peterson, R. A., & Balasubramanian, S. (2002). Retailing in the 21st cen tury: Reflections and prologue to research. Journal of Retailing, 78(1), 9-16. doi:10.1016/S0022-4359(01)00062-8

Porter, M. E. (1990). The Competitive Advantage of Nations. Harvard Busi-ness Review. Recuperado de https://hbr.org/

Rosenberg, J. M. (1993). Dictionary of business and management. New York, EUA: John Wiley & Sons.

Silva, J. D., Faia, V. da S., Vieira, V. A. (2016). Os efeitos negativos da ex-periência e do controle no desempenho do vendedor. RAE-Revista de Administração de Empresas, 56(6), 626-640. doi:10.1590/S0034-759020160605

Varotto, L. F., & Parente, J. G. (2016). Franchisor-franchisee relationship quality: Time of relationship and performance. RAE-Revista de Adminis-tração de Empresas, 56(6), 600-610. doi:10.1590/S0034-759020160603

Verhoef, P. C., Kannan, P. K., & Inman, J. J. (2015). From multi-channel re-tailing to omni-channel retailing: Introduction to the special issue on multi-channel retailing. Journal of Retailing, 91(2), 174-181. doi:10.1016/j.jretai.2015.02.005

600

ISSN 0034-7590© RAE | São Paulo | V. 56 | n. 6 | nov-dez 2016 | 600-610

LUÍS FERNANDO [email protected] at Universidade Nove de Julho, Diretoria de Ciências Gerenciais – São Paulo – SP, Brazil

JURACY GOMES PARENTE [email protected] at Fundação Getulio Vargas, Escola de Administração de Empresas de São Paulo – São Paulo – SP, Brazil

FORUMSubmitted 03.02.2016. Approved 08.11.2016Evaluated by double blind review process. Scientific Editors: Delane Botelho and Leandro Guissoni

FRANCHISOR-FRANCHISEE RELATIONSHIP QUALITY: TIME OF RELATIONSHIP AND PERFORMANCEQualidade do relacionamento franqueador-franqueado: Tempo de relacionamento e desempenhoCalidad de las relaciones franquiciador-franquiciado: Tiempo de relaciones y desempeño

ABSTRACTFranchise literature disputes how the relationship between franchisors and franchisees develops over time. Traditional lifecycle theory views relationships following an ascendant curve, in which relationship quality and performance strengthen over time. Another perspective better reflects the peculiarities of the franchisor-franchisee relationship, indicating that relationship quality in franchise systems follows a U-shaped curve. There is also limited research on the moderating effect of time on the relationship between relational variables and outcomes. This study sheds light on the influence of relationship duration on relationship quality and financial performance in the franchisee-franchi-sor relationship. Using a self-report survey from a sample of 342 franchisees, mean and regression analyses are conducted to test relationships. Results confirm the time effect on franchisor-franchisee relationship quality and performance, but the hypothesized shape of relationship phases is only par-tially confirmed. Moreover, time has a positive moderating effect on the impact of relationship quality on financial performance. KEYWORDS | Franchise, relationship quality, financial performance, U–curve theory, time of relationship.

RESUMOA literatura sobre franquia diverge acerca de como o relacionamento entre franqueadores e franqueados se desenvolve ao longo do tempo. A teoria tradicional do ciclo de vida considera que os relacionamentos seguem uma curva ascendente, na qual a qualidade do relacionamento e o desempenho fortalecem-se com o tempo. Outra perspectiva reflete melhor as peculiaridades do relacionamento entre franquea-dor e franqueado, indicando que a qualidade do relacionamento em um sistema de franquia segue uma curva em forma de U. Ademais, há um número limitado de pesquisas sobre o efeito moderador do tempo sobre o relacionamento entre variáveis relacionais e resultados. Este estudo lança luzes sobre a influência da duração do relacionamento sobre a qualidade do relacionamento e sobre o desempenho financeiro, no relacionamento entre franqueador e franqueado. Utilizando uma pesquisa de auto relato com uma amostra de 432 franqueados, foram realizadas análises de regressão e de média para testar os relacionamentos. Os resultados confirmam o efeito do tempo sobre o desempenho e a qualidade do relacionamento entre franqueador e franqueado, mas o formato hipotético das fases do relacionamento foi apenas parcialmente confirmado. Além disso, o tempo tem um efeito moderador positivo sobre o impacto da qualidade do relacionamento no desempenho financeiro.PALAVRAS-CHAVE | Franquia, qualidade de relacionamento, desempenho financeiro, teoria da curva em U, tempo de relacionamento.

RESUMENLa literatura sobre franquicias disputa cómo se desarrollan las relaciones entre los franquiciadores y franquiciados con el transcurso del tiempo. La teoría del ciclo de vida tradicional ve las relaciones siguiendo una curva ascendente en la que la calidad y el desempeño se fortalecen con el pasar del tiempo. Otra perspectiva refleja mejor las peculiaridades de las relaciones franquiciador-franquiciado, indicando que la calidad de las relaciones en los sistemas de franquicias sigue una curva en U. También hay investigaciones limitadas sobre el efecto moderador del tiempo en las relaciones entre variables relacionales y resultados. Este estudio arroja una luz sobre la influencia de la duración de las relaciones sobre la calidad y el desempeño financiero en las relaciones de franquiciados-franquiciadores. Utili-zando una encuesta de autoinforme de una muestra de 342 franquiciados, se conducen análisis de medias y de regresión para probar las relaciones. Los resultados confirman el efecto del tiempo en la calidad y desempeño de las relaciones franquiciadores-franquiciados, pero la forma hipotética de las fases de las relaciones está confirmada sólo parcialmente. Además, el tiempo tiene un efecto moderador positivo en el impacto de la calidad de las relaciones sobre el desempeño financiero.PALABRAS CLAVE | Franquicia, calidad de relaciones, desempeño financiero, teoría de la curva U, tiempo de relaciones.

RAE-Revista de Administração de Empresas | FGV/EAESP

DOI: http://dx.doi.org/10.1590/S0034-759020160603

601

ISSN 0034-7590

AUTHORS | Luís Fernando Varotto | Juracy Gomes Parente

© RAE | São Paulo | V. 56 | n. 6 | nov-dez 2016 | 600-610

INTRODUCTION

Franchising is one of the fastest developing forms of business in the world, and a rich field for studies in marketing and other relevant areas, such as economics, law, management, finance, and entrepreneurship (Grewal, Iyer, Javalgi, & Radulovich, 2011), due to its varied possibilities on governance formats and inter-organizational behaviors (Dant, Grünhagen, & Windsperger, 2011). The success of the franchise system depends on the performance of inter-organizational behaviors in the franchisor-franchisee dyad over time (Grayson, 2007; Heide & Wathne, 2006). Indeed, satisfactory relationships between franchisor and franchisees have long been recognized as critical to the success of the franchise system (Watson & Johnson, 2010).

The measure of franchise performance includes both non-financial (e.g., relationship quality) and financial indicators of performance (e.g., sales growth and profitability) (Venkatraman & Ramanujam, 1986, 1987). Although the relevance of the franchisor-franchisee relationship is evident, there are few studies concerning how this relationship develops over time (Dant, Li, & Wortzel, 1995; Dant, 2008). Indeed, relationship marketing shifted its focus from discrete transactions to long-term relationships (Jap & Ganesan, 2000), raising the need to distinguish between short-term transactions and long-term relational exchanges (Dwyer, Schurr, & Oh, 1987). Therefore, the influence of time, as well as its role on relational and outcome variables, are relevant issues.

In numerous studies, the concept of time is considered as the relationship duration (Athanasopoulou, 2009), and most theories focus on the relationship between organizational buyers and sellers (Dwyer et al., 1987) or on the behavior of the individual representing each organization (Ring & Ven, 1994). Literature in relationship marketing, under the traditional lifecycle theory (Blut et al., 2011; Dant & Nasr, 1998; Dwyer et al., 1987), sees relationships in franchises following an ascendant curve, in which relationship quality and performance strengthen over time and relationship variables are potentially affected by relationship duration (Jap & Anderson, 2007). In fact, buyer-seller relationships are the base for the traditional relationship lifecycle theory, whose study first originated in the U.S. during the early 1980s, initially focusing on the distribution channels approach and, later, on the buyer-supplier relationship. Focusing on business relationships, economic exchanges, and efficiency, research on buyer-seller relationships seeks to explain governance structures and the nature of dyadic behavior in the market-channel context (Möller & Halinen, 2000).

However, buyer-seller relationships may not adequately represent the relationship pattern for franchisor-franchisee relationships, since franchise relationships do not resemble a traditional business-to-business (B2B) exchange relationship

(Grace & Weaven, 2011). Indeed, franchisee-franchisor relationships should be analyzed in the context of inter-organizational exchange, as well as within the context of inter-personal interactions, given their social and subjective nature (Dant, Weaven, & Baker, 2013), whose relationship building parallels marriage analogies (Doherty & Alexander, 2004). Most studies in the marriage context suggest a U-shaped pattern, with high marital happiness in the early years of marriage, a decline in marital happiness during the middle years, and a rise in marital happiness in the later years (VanLaningham, Johnson, & Amato, 2001). Blut et al. (2011) propose that relationships in franchise systems follow a similar logic to the U-shaped curve of marriage contexts. This alternative pattern would explain the evolution of relational variables in franchising better than the traditional lifecycle theory. Given this controversy, this study sheds light on the influence of relationship duration on relationship quality and financial performance in the franchisee-franchisor relationship.

The success of the franchise system depends not only on the relationship quality performance for franchisors and franchisees, but also on the financial performance achieved by these two major players (Brown & Dev, 1997). Considering a broader conceptualization of performance in franchising, this study also investigates the influence of time of relationship upon financial indicators of performance (Venkatraman & Ramanujam, 1986), such as sales growth and profitability (Venkatraman & Ramanujam, 1987). Although financial performance has been acknowledged as a consequence of relationship quality (Athanasopoulou, 2009), there have been few studies that analyze the relationship between nonfinancial measures—such as relationship quality—and financial performance (Banker, Potter, & Srinivasan, 2005). Huntley (2006) finds evidence of the link between relationship quality and profitable outcomes in B2B relationships; however, this issue is still relatively unexplored in the franchise context. Consequently, the present work also seeks to elucidate and address this important issue.

LITERATURE REVIEW AND PROPOSED HYPOTHESESFranchising and relationship constructs

Franchising can be defined as contractual arrangements that represent a form of relational exchange (Grünhagen & Dorsch, 2003), characterized by a long-term continuous perspective, involved in complex relationships, where the survival of the relationship takes precedence over any single exchange (Strutton, Pelton, & Lumpkin, 1995). The satisfactory relationship between franchisor and franchisees has long been recognized as critical to

602

ISSN 0034-7590

FORUM | Franchisor-franchisee relationship quality: Time of relationship and performance

© RAE | São Paulo | V. 56 | n. 6 | nov-dez 2016 | 600-610

the success of a franchise system, where satisfactory relationships specifically mean that franchising provides benefits for the entire network (Watson & Johnson, 2010). Initial research into franchises focuses on the choice of franchising as an organizational form, grounding its assumptions predominantly on either resource scarcity or agency theory. However, over time, the focus of research has moved toward understanding the relationship between franchisors and franchisees (Watson & Johnson, 2010).

Franchisors are expected to provide services for their franchisees, such as training, research and development, advertising and marketing support, management assistance, and supply provision (Watson & Johnson, 2010), which are relevant for system promotion and uniformity (Monroy & Alzola, 2005). Positive or negative franchisee evaluation of these services over time affects both their satisfaction and dissatisfaction, leading to greater trust or ensuing conflict in the relationship, with affects the perception of the franchisee’s relationship quality (Chiou, Hsieh, & Yang, 2004).

Relationship quality is a crucial concept in the development of long-term and mutually beneficial relationships (Athanasopoulou, 2009), and, for some authors, represents the strength and magnitude of a relationship (Dant et al., 2013; Monroy & Alzola, 2005). Analyzing the franchise context, Monroy & Alzola (2005) introduce the concepts of transactional and relationship quality as different but interdependent constructs. Transactional quality is related to short-term business performance, considering two dimensions for franchisees (i.e., contents and assistance), which include attributes such as training, support, information, supply, financial facilities, management assistance, and accessibility, and also two dimensions for franchisors (i.e., formality and identity), which include business development, training attendance, payment accomplishment, uniformity, and transparency. Relationship quality, on the other hand, is related to the long-term performance of franchise partners. It includes variables such as trust, commitment, and relationship, and requires time to be developed and consolidated. Therefore, transactional quality “guarantees a satisfactory business start-up, constituting the first step in the development of a long-term relationship” (Monroy & Alzola, 2005, p. 598)

Relationship quality, according to mainstream academic research, is considered an overall assessment of relationship strength, and treated as a global or higher-order construct that reflects a combination of multiple first-order factors (Palmatier, 2008), which capture different but related facets of a relationship (Palmatier, Dant, Grewal, & Evans, 2006). Relationship quality’s most cited dimensions in academic research are trust, commitment, and satisfaction (Athanasopoulou, 2009; Palmatier et al., 2006).

Trust is one of the most relevant constructs in relationship marketing (Anderson & Narus, 1990; Doney & Cannon, 1997; Ganesan, 1994; Mohr & Spekman, 1994; Morgan & Hunt, 1994), and

is tied to the belief in partner integrity and predictability (Morgan & Hunt, 1994). Under this view, a company acts in order to generate positive results and does not take unexpected actions which may harm their partners (Anderson & Narus, 1990). This is an important factor in building long-term relationships (Ganesan, 1994), since in the presence of trusted long-term idiosyncratic investments can be made with limited risk (Doney & Cannon, 1997).

Commitment is related to the intention and desire of the parties to maintain a given relationship in the future (Wilson, 1995). In marketing literature, commitment is associated to survival, performance (Anderson & Weitz, 1992; Geyskens, Steenkamp, Scheer, & Kumar, 1996; Morgan & Hunt, 1994) and successful long-term relationships (Walter, Mueller, & Helfert, 2000). Therefore, commitment is associated to the partners’ intention to continue the relationship, and their willingness to accept short-term sacrifices in order to achieve long-term benefits (Morgan & Hunt, 1994) by means of relationship survival and stability (Anderson & Weitz, 1992; Dwyer et al., 1987).

Satisfaction is the most popular construct in empirical studies of channel relationship models (Geyskens, Steenkamp, & Kumar, 1999), and is typically positively linked to the continuity of long-term relationships, and negatively linked to conflicts in the relationship (Anderson & Narus, 1990). Satisfaction is related to the perceived discrepancy between prior expectations and actual profits (economic perspective) or to an emotional response to the overall working relationship with the channel partner (non-economic perspective) (Crosby, Evans, & Cowles, 1990; Geyskens et al., 1999). Within the franchise context, satisfaction has been tied to the franchisee’s commitment and intention to remain in the relationship (Chiou et al., 2004).

Successful inter-organizational relationships are a critical issue in terms of financial performance (Palmatier, Dant, & Grewal, 2007), since firms with higher levels of cooperation and reduced conflict are more willing to improve innovations, expand markets, and reduce costs (Cannon & Homburg, 2001). In fact, good relationships, trust in partners, and commitment should improve organizational performance, given that, in an environment of this nature, exchanges produce greater satisfaction and efficiency (Wang & Yang, 2013). There are many key drivers of inter-organizational relationship performance. Palmatier et al.(2007) claim that at least four main theories dominate attempts to understand these drivers—commitment-trust theory (Morgan & Hunt, 1994), the perception of dependence (Bucklin & Sengupta, 1993), transaction cost economics (Williamson, 1979), and the perspective of relational norms (Kaufmann & Dant, 1992).

Therefore, although performance has been measured from various viewpoints, depending on the research questions, disciplinary focus, and data availability, the main focus has been

603

ISSN 0034-7590

AUTHORS | Luís Fernando Varotto | Juracy Gomes Parente

© RAE | São Paulo | V. 56 | n. 6 | nov-dez 2016 | 600-610

towards business economic performance, which is reflected by dimensions such as sales growth, net income growth, return on investment, profitability, relative market position, and market share (Venkatraman & Ramanujam, 1987). In franchise literature, financial performance has been measured mainly by franchise profitability, annual sales, and sales growth (Soontiens & Lacroix, 2009).

Following the work of Blut et al (2011), this study operation-alizes the measure of financial performance using the informant’s perceived performance rather than objective measures of perfor-mance. Accordingly, it also focuses on the franchisee’s perception of sales growth and profitability in order to measure perceived financial performance.

Time, as a variable, is included in numerous studies as relationship duration, and the role of time in relationships can be analyzed from more than one vantage point (Athanasopoulou, 2009). Indeed, the concept of relationship dynamics is explained by a multitude of theories adapted from sociology, as to explain relationship development in inter-organizational contexts (Ring & Ven, 1994). One of these points of view is the episodic perspective, under which relationships follow a cycle, replete with a construction, development, and a likely end (Athanasopoulou, 2009). Time is seen as a series of phases or periods in which relationship variables change according to time phases (Dwyer et al., 1987; Morgan & Hunt, 1994; Wilson, 1995). Traditional lifecycle theory sees relationships proceeding through a sequence of phases (Dwyer et al., 1987), typically differentiated as (1) formation, (2) exploration, (3) maturity, and (4) termination.

Following traditional lifecycle theory, after the first experiences between the parties in the initial relationship phase, relational variables, such as cooperation and dependence, are assessed more favorably over time. As the relationship matures, the ties between partners strengthen, thus increasing their interdependence (Blut et al., 2011). Life-cycle theory has produced empirical results that suggest that numerous relational variables follow an inverted U-shaped curve (Jap & Anderson, 2007). However, Blut et al. (2011) find that this life-cycle configuration may not extend to other inter-organizational arrangements that differ from those based on traditional buyer-seller relationships, such as franchisor-franchisee relationships. These researchers, in contrast to the life cycle theory, suggest that relational constructs in the franchise context may follow a U-shaped curve over time, with a “honeymoon” initial phase, following stages of “routine,”

“crossroads,” and “stabilization.” Blut et al. (2011) find evidence of a U-shaped curve in variables such as satisfaction, trust, commitment, and performance.

Therefore, following the perspective of Blut et al. (2011), this study examines if relationship quality and financial performance do follow a U-shaped curve, leading to the following hypotheses:

H1a: The relationship between relationship quality and time follows a U-shaped curve, which is high in the first and fourth phase, and low in the second and third phase.

H1b: The relationship between financial performance and time follows a U-shaped curve, which is high in the first and fourth phase, and low in the second and third phase.

The moderating role of time on the effects of relational variables, such as trust and commitment, on relational outcomes has been examined in business-to-consumer contexts, but it has been somewhat neglected in B2B settings (Victoria Bordonaba-Juste & Polo-Redondo, 2008). In fact, only the moderating role of relationship time in the effects of trust and commitment on satisfaction and the intention to continue a relationship were tested by Victoria Bordonaba-Juste and Polo-Redondo (2008), but the moderating role of time on the effect of relational variables, such as relationship quality, on financial performance is still unexplored.

In longer relationships, parties benefit from mutual expe-rience and variables, such as trust, commitment, communication, and cooperation. Over time, bonds become stronger and the rela-tionship closer (Athanasopoulou, 2009). There are also evidences that, in general, long-term relationships are more profitable than short-term ones (Reichheld & Teal, 2001).

Therefore, during the lifetime of a relationship, relational variables, such as relationship quality, should receive better assessments, as well as financial performance evaluations, by partners in long-term relationships than in short-term ones. From this point of view, the following hypothesis is also tested:

H2: The effect of relationship quality on financial performance is stronger in long-term relationships than in short-term ones.

METHODOLOGY

Sampling procedures

The sample for this investigation was drawn from the list of franchisees of three Brazilian franchisors within the educational and fast food segments. These franchisors provided the researcher with a list of franchisee stores and their e-mail addresses. The questionnaire was tested and revised prior to general administration. In total, 1237 franchisees were invited to participate in an on line survey. To encourage participation, we emphasized the premise of confidentiality, as franchisors would only have access to aggregate data. A total of 348 usable surveys were obtained, representing a response rate of 28.1%. To reinforce confidentiality, responses were obtained in an anonymous fashion. Examination of sample characteristics

604

ISSN 0034-7590

FORUM | Franchisor-franchisee relationship quality: Time of relationship and performance

© RAE | São Paulo | V. 56 | n. 6 | nov-dez 2016 | 600-610

indicates that females represent 54.4% of respondents and 70.0% of the franchisees operate only one unit. There is no significant difference among the franchisees’ profile of the three franchise networks. A Mahalanobis distribution analysis to identify outliers was performed, and six elements that presented difference in behavior were eliminated, leaving 342 questionnaires.

Measures employed and psychometric assessment

Relationship quality was measured by the same scale used by Dant et al. (2013), in a study which measures the perceived relationship quality between franchisors and franchisees. Three scales measure satisfaction, trust, and commitment, and all three scales are seven-point Likert-type scales, from 1 (strongly disagree) to 7 (strongly agree).

Perceived financial performance is measured by means of a Likert-type scale derived from Venkatraman & Ramanujam (1987) and Griffith et al. (2006), which measures the constructs

of franchisee sales growth and profitability. These scales were originally developed and applied in English. For this reason, they were translated into Portuguese and subsequently validated. Both are five-point Likert-type scale, from 1 (much worse) to 5 (much better), with a defined neutral point anchored with a response of 3 (equal). In these questionnaires, franchisees provide answers regarding their sales growth and profitability in comparison with similar stores in the region.

Time of relationship is measured as the number of months of the relationship between the franchisees and their respective franchisors. For testing, the sample is distributed in four groups (phases), following the parameters adopted by Blut et al. (2011):

1. Honeymoon—ends after one year2. Routine—ends after four years3. Crossroads—ends after eight years4. Stabilization—begins after eight years

Table 1 shows reliability analysis for the scales above.

Table 1. Reliability analysis

Construct Item Factor loading

Composite reliability

Cronbach’s Alpha

Commitment

We are very committed to the relationship with our franchisor 0.887 0.96 0.96I enjoy working with this franchisor 0.823I feel as though the franchisor and I are “in it together” 0.894It feels like the franchisor and I are constantly doing something for each other 0.810I feel that the values of this franchise system match my own 0.874We try our best to maintain our relationship with our franchisor 0.807We feel proud to belong to this franchise system 0.862We intend to continue functioning as a franchisee of our franchisor 0.667We have a mutually beneficial relationship 0.834The franchisor and I get along well together 0.855The franchisor and I tend to share similar values 0.843

Satisfaction

Overall we consider our relationship with the franchisor to be: Satisfying 0.847 0.96 0.94Overall we consider our relationship with the franchisor to be: Friendly 0.806Overall we consider or relationship with the franchisor to be: Considerate 0.860Overall we consider our relationship with the franchisor to be: Cordial 0.874Overall we consider our relationship with the franchisor to be: Supportive 0.873Overall we consider our relationship with the franchisor to be: Fair 0.906Overall we consider our relationship with the franchisor to be: Healthy 0.893

Trust

I can rely on my franchisor to keep the promises they make to me 0.894 0.96 0.96I can count on my franchisor to be honest in its dealings with me 0.928My franchisor can be counted on to do what is right 0.899My franchisor is sincere in its dealings with me 0.918My franchisor is a company that I have great confidence in 0.865My franchisor is a company that stands by its word 0.917

Sales growth Compared to other stores in this region, its sales growth is (if you have more than one unit measure the average): 0.934 0.91 0.80

Profitability Compared to other stores in this region, its profitability is (if you have more than one unit measure the average) 0.892

605

ISSN 0034-7590

AUTHORS | Luís Fernando Varotto | Juracy Gomes Parente

© RAE | São Paulo | V. 56 | n. 6 | nov-dez 2016 | 600-610

RESULTS AND DISCUSSION

The mean analysis statistical technique is applied to investigate the differences in the means of relationship quality and financial performance variables along the proposed relationship phases (hypotheses H1a and H1b). This technique is used to determine if the means of the variables associated with relationship quality and financial performance are significantly different within the four tested phases of the relationship. Regression analysis is used to test the influence of the time of relationship in the link between relationship quality and performance (hypothesis H2).