INSTITUTIONAL PRESENTATION2Q18

ReinoUnido

Arabia Saudita

França

Coreia do Sul

Brasil

Alemanha

Canadá

Rússia

Japão

Índia

EUA

China

336

345

551

579585

653

712

1.090

1.101

1.541

4.2516.529

2017

World’s Largest Producers (TWh)

8th POSITION

Source: Global Energy Statistical Yearbook 2017

ELECTRICITY GENERATION

2

3Source: EPE - Empresa de Pesquisa Energética

NATIONAL CONSUMPTION

Outros*= Consumption Rural; Public Service; Public Lighting

National Consumption by Class Acumulated (TWh)

33,942,2

22,4 19,3

117,8

32,841,7

21,8 19,1

115,4

2 T 18 2 T 17

Residential Industrial Commercial Others* Total

(+ 3.5%)( + 1.1%)

(+ 1.2%)( + 2.5%)

( + 2.1 %)

4Source: ONS

39,8%

10

20

30

40

50

60

70

80

90

Jan Fev Mar Abr Mai Jun Jul Ago Set Out Nov Dez

2015

2016

2017

2018

RESERVOIRS LEVEL

Subsystem Southeast / Midwest(70% country storage )

ENERGY GENERATION 2017X 2018

5Source: ONS

HG –Hydraulic Generation TG–Thermal Generation

J F M A M J J A S O N D

HG_2017 HG_2018 TG_2017 TG_2018 Load_2017 Load_2018

63.863 MW average

65.611 MW average

PHSICAL GUARANTEE X HYDRO GENERATION

6

GSF – Generation Scaling Factor

53,9 54,658,4 60,0 60,5 60,8 59,5

56,1

46,445,7 45,8

49,051,1

54,8

42,9 42,737,4 36,2 37,1 37,8 39,8

44,5

49,6 51,9 53,748,9

43,138,9

0,796 0,781

0,640

0,603 0,612

0,6220,669

0,793

1,069 1,137

1,172

0,999

0,843 0,709

0,000

0,200

0,400

0,600

0,800

1,000

1,200

-

10

20

30

40

50

60

70

80

90

100

Physical Guarantee Hydro Generation GSFGW médio GSF

Source: CCEE

2012 2013 2014 2015 2016 2017 2T17 2T18

166,69

263,07

688,88

287,20

94,10

324,17 303,75 302,93

AVERAGE PRICE PLD - R$/MWh

Subsystem Southeast / Midwest

Yearly Average Monthly/Quarter Average

7

Source: CCEE

8

100% Hydro Generation

1,2 million customers

14.105 employees

22 plants

11.000 MW capacidade instalada

US$ 9,8 billion in liabilities

US$ 21,6 billion in assets

EBITDA of US$ 518 million

Debt/EBITDA: 19 x

43 customers

468 employees

3 plants

1.654,6 MW instaled /capacity

US$ 85,1 million in liabilities

US$ 2.7 billion in assets

EBITDA (UDM): US$ 103 million

Debt/EBITDA: 0,9 x

9

04/14/99

APRIL/ 01/99SPLIT UP

07/16/98

Privatized

11/05/97

HISTORICAL

10

CESP has the grant of three hydro generations acting on price regime. Total installed capacity is

1,654.6 MW.

11

14 1.540,0 941.8 jan/23/99 jul/11/28

2 87,0 47.5 apr/20/78 mar/09/21

2 27,6 13.3 may/05/72 may/20/20

PORTO PRIMAVERA

PARAIBUNA

JAGUARI

18 1.654,6 1.002 - -TOTAL

From December 22, 2016, the date of publication by MME - Ministry of Mines and Energy, of Ordinance No. 258, the physical guarantee

of the Porto Primavera HPP was reduced from 1,017 to 992.6 MW average, which added to the physical guarantees of the Paraibuna

and Jaguari, totals 1,056.6 average MW. On May 3, 2017, the MME published Ordinance No. 178, reducing from 2018 the physical

guarantee of the Porto Primavera HPP from 992.6 to 941.8 MW average, from the Paraibuna HPP from 50.0 to 47.5 MW average, and

from Jaguari HPP from 14.0 to 13.3 average MW. With this, the physical guarantee marketable in 2018 will increase from the current

1,056.6 to 1,002.6 average MW. The Company has already filed a lawsuit against the Federal Government to reverse the effects of

Administrative Rule 258/2016 and continues to make efforts to reverse the effects of these changes on its concession agreement.

HPP INSTALLED

CAPACITY

Nº OF

UNITS

PHISICAL GARANTEE

MW Average

OPERATION

START

CONCESSION

END

12

(R$ million)June/30/2018

Occurrences / HPPTrês

IrmãosIlha

SolteiraJupiá Total

Amount of Plants 3,529 2,166 642 6,337

Provision - Contingent Assets / Impairment - -1,657 -338 -1995

Sub Total – Dec 31, 2014 3,529 509 304 4,342

Provision 4T15 -1,812 -379 -201 -2392

Balance of Available Assets to Reversal 1,717 129 103 1,949

Amount on dispute in Court 6,690 915 647 8,252

Base Period Apr-13 Jun-15 Jun-15

AVAILABLE ASSETS FOR REVERSAL

13

OPERATIONAL PERFORMANCE

2011 2012 2013 2014 2015 2016 2017 2T18

41.056 42.353

35.946

29.171 24.067

9.434 9.474

2.150

9.470

2.190

9.256

Energy Production X Physical Guarantee (GWh)

34.304

Physical Guarantee: 1.081 MW = 9.469 GWh Annual ; 4.696 1H17

14

32.399

21.282

34.304

34.304

2012 2013 2014 2015 2016 2017 2018

0,925 0,925 0,931 0,920

0,939 0,938 0,938

0,898

0,898

Source: ONS

0,0165

June/2018

15

Forced Unavailability Equivalent Rate – TEIFa

OPERATIONAL SITUATION

0,0251

0,0165

0,0095

0,0101

0,0097

0,0160

0,0048

0,0055

0,0057

2012 2013 2014 2015 2016 2017 2018

16

Capital Increase R$ 3.2 billions

Term: 10 yearsGrace Period: 5

years (for principal)

To match its cash flow generation with its debtservice, CESP has launched a comprehensivecapital restructuring plan with the following maincomponents:

Privatization of CTEEP – R$ 1.2 billionJul/2006

Public Offering of Preferred Class B Shares (PNB) – R$ 2.0 billion

Jul/2006

Bonds OperationsUS$220 million = R$ 488 million - Aug/2006US$350 million = R$750 million - Jan/2007

FIDC III – R$ 650 millionAug/2006

FIDC IV – R$ 1.25 billionJun/2007

Funds Involved in the Restructuring - R$ 6.3 billion

1.2

2.0

1.2

0.65

1.25

C

T

E

E

P

P

U

B

L

I

C

O

F

F

E

R

B

O

N

D

S

FIDC III

F

I

D

CIV

17

39.832 41.353

32.29228.538

20.901

10.177 11.131

5.092

84,7392,29

139,61

189,25

164,93178,15 181,49

192,51

5.480

3.330

Average Prices R$/MWh

Invoiced Amount GWh

3.526

18

4.420

2.053

Gross Revenue

R$ million

GROSS REVENUE & PRICES

920

787 9541.287

1.866

935 604 429 461

794985

1.068

1.449

893

587423 459

841943

959

1.061

856

435441

908

937

1.106

1.104

842

426456

3.819

1.750

69,162,2

78,4

85,5

58,954,6

26,3 52,6

EBITDA Margin (%)

2011 2012 2013 2014 2015 2016 2017 2018

726 842 1.1451.704

780 481 362 394

700875

940

1.300

748

468358 391

735831

867

939

715

374353

796805

951

913

708

345394

1.467

2.957

2.043 2.086

3.063

4.017

1.740

908

389 4133.354

Evolution of Net Revenue

3.904

Net Revenue & EBITDA

4.856

EBITDA (R$ million)

2.951

19

1.668

785

20

Customer Portfolio (MW average)

CONTRACTED ENERGY

2018 2019 2020 2021 2022 2023 2024

22%230

22%230

22%230

22%230

26%230

41%230

62%230

78%832

78%839

78%824

78%819 74%

646

59%330 38%

140

Distribuidores Mercado Livre

21

Prices R$/MWh (june/2018)

CONTRACT PRICES

2018 2019 2020 2021 2022 2023 2024

229,74 235,15 235,82 235,81 235,81 235,81 235,82

182,09 186,06 186,21 187,02

200,25

178,45

142,25

Distribuidores Mercado Livre

2011 2012 2013 2014 2015 2016 2017 6M18

1.771

2.223

1.694 1.7011.868

1.295

464 436

2011 2012 2013 2014 2015 2016 2017 6M18

1.330 1.283

1.038 922

802

568 466 468

2011 2012 2013 2014 2015 2016 2017 6M18

7,66,3

5,14,0

6,9

10,69,3 8,5

Costs & Operational Expenses

R$ million

Personnel Expenses/Net Revenue(%)

Employees

22

23

Debt Charges + Monetary Variation

(Excluding Exchanges Variation) R$ million

2011 2012 2013 2014 2015 2016 2017 6M18

443

380 391

309

213

9976

13

24

R$ million

2012 2013 2014 2015 2016 2017 6M18

129

86

32

75

13 9 6

Capital Investment

25

EBITDA Margin 26.2% 50.6% -24.4 pp

Operational Revenue 459 422 8.8%

Net Operational Revenue 391 358 9.4%

EBITDA Adjusted 102 181 - 43.4%

Net Income 341 67 410.3%

Financial Results (43) (1.5) 2,809%

R$ million

FINANCIAL HIGHLIGTHS

26

EBITDA Margin 52.6% 58.7% -6.1 pp

Operational Revenue 921 852 9.3%

Net Operational Revenue 785 720 9.1%

EBITDA Adjusted 413 422 -2.2%

Net Income 337 139 142.0%

Financial Results - 31 + 39 -

R$ million

FINANCIAL HIGHLIGTHS

27

28

(R$ million)

PROVISIONS FOR LEGAL RISKS

Balance 1Q18 3.081

Monetary Correction and interest 100

Payments -8

Deposits in payments -25

Agreements with MS Estate -583

Provision and Reversal -394

Balance 2Q18 2.171

COURT LAWSUITS

29

Base: June/2018

Of the amounts related to lawsuits filed against CESP (judicial liabilities), 85% of them refer to theUHE Porto Primavera and are concentrated in lawsuits, most of which are filed in courts affiliatedto the Mato Grosso do Sul State.

Probability Quantity of

Lawsuits

Amount

06/2018

Relevant

Lawsuits

Amount

06/2018

PROBABLY 1,129 R$ 2.2 23 R$ 1.5

POSSIBLE 1,639 R$ 2.1 38 R$ 1.6

REMOTE 579 R$ 6.7 16 R$ 6.6

TOTAL 3,347 R$ 11.0 77 R$ 9.8

( R$ billion)

2009 2010 2011 2012 2013 2014 2015 2016 2017 2T18

30

Local Currency

Evolution by Currency(R$ billion)

5,3

4,54,2

3,7

3,0

-94%

2,8 2,2 2,1 1,7 1,1 0,7 1,0 0,9 0,9 0,9

Debt / EBITDA ratio

2,8

65% 63% 69% 66% 75% 74%

35%

37%

31%

34%

25%26%

Foreign Currency

51%

49%

1,7

FINANCIAL DEBT

32%97%

0,8

68%98%

0,40,3

3% 2%

FINANCIAL DEBT

31

June 30/2018 R$ 337.4 million

Debt in Foreign Currency

US$ 85.1 million (R$ 328.1 million)

Funcesp R$ 2,00,6%

Others R$ 1,20,4%

BNDES BradyR$ 326,996,8%

Eletrobrás R$ 7,32,2%

2018 2019 After 2019

205

FINANCIAL DEBT PROFILE

32

June, 30/2018 R$337.4 million

Local Currency

210

2%

3

36%

2%

98% 98%

99%

64%

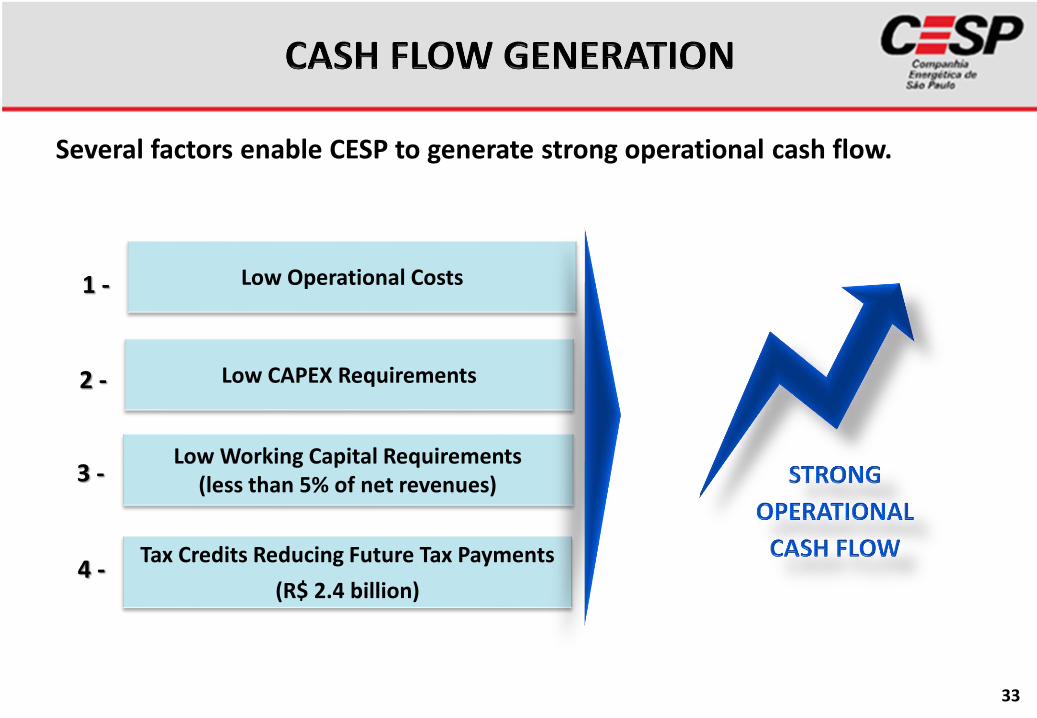

1 -

2 -

3 -

4 -

Low Operational Costs

Low CAPEX Requirements

Low Working Capital Requirements (less than 5% of net revenues)

Tax Credits Reducing Future Tax Payments

(R$ 2.4 billion)

Several factors enable CESP to generate strong operational cash flow.

33

34

35

TOTAL CAPITAL COMMON x PREFERRED

Common (ON); 33,3%

Preferred (Class A);

2,3%

Preferred (Class B);

64,4%

Preferred; 2/3

Common 1/3

36

Common (ON) & Preferred (PNA + PNB)

Market; 5%

SP State; 95%

Market

87%

SP State13%

ON PNA + PNB

37Source : ITAU

June 2018 (%)

CONTROL GROUP

SHAREHOLDERS ON PNA PNB TOTAL

FAZENDA DO ESTADO DE SÃO PAULO 94.1 - 7.2 36.0

COMPANHIA PAULISTA DE PARCERIAS - - 6.5 4.2

OUTHER 1.1 - - 0.4

SUBTOTAL 95.2 - 13.7 40.6

FREE FLOAT

ELETROBRÁS 0.1 90.2 - 2.0

HSBC BANK PLC LONDON - - 9.5 6.1

SQUADRA INVESTIMENTOS - - 5.0 3.2

MORGAN STANLEY 4.4 2.8

UBS AG LONDON - - 5.4 3.4

WESTERN ASSET DTVM - - 4.7 3.0

OUTHER 4.7 9.8 57.3 38.9

SUBTOTAL 4.8 100 86.3 59.4

TOTAL 100 100 100 100

Main Shareholders

38

5,066

4.8

100.0

86.3

5.3

7.4

182.0

33.3

2.3

64.4

109.2

7.4

210.9

1,452

163

3,451

59.4 194.7 3,211 100.0 327.5

R$ million

June 30/2018

70

163

2,978

39

11,00

12,00

13,00

14,00

15,00

16,00

17,00

18,00

19,00

20,00

21,00

CESP6 SHARES QUOTATION

From Jan 1st/2018 to June 30th/2018

Source: AE Broadcast

IEE –Electric Energy Index IBOV – Bovespa Index

40

From Jan/2003 – July 2018

CESP CORPORATE RATING

41

Prime AAA AAA

AA+

High Grade AA

AA-

A+

Upper Medium Grade A

A-

BBB+

Lower Medium Grade BBB bbb-

BBB-

BB+

Speculative BB BB-

BB- Ba2

B+

Highly Speculative B

B-

CCC+

Insolvency Risk CCC

CCC-

Substancial Risk CC

Insolvency Probability C

SD

Default DDD

DD

D

jan/03 jul/03 jan/04 jan/06 jul/06 jan/07 jul/07 jan/08 jul/08 jan/09 jul/09 jul/10 jan/11 jul/11 ago/12 abr/13 fev/14 mai/14 dez/15 fev/16 jun/16 mai/17 Jan/18 Jul/18

S&P Local S&P Global S&P Stand Alone (SACP) Moody´s Global

Inve

stim

en

t G

rad

eD

isti

nct

ly

Spe

cula

tive

Pre

do

min

antl

y

Spe

cula

tive

42