relatÓrio e contas 2016 pág. 003fcf62ac6-847a-47e5-bf70-498228c7c6d4}.pdf · estados unidos,...

TRANSCRIPT

RELATÓRIO E CONTAS 2016pág. 003

—

ANNUAL REPORT 2016pag. 113

RELATÓRIOE CONTAS

2016PT

003BANC — Relatório e Contas, 2016

1. PRINCIPAIS INDICADORES 005

2. AMBIENTE ECONÓMICO 009

3. INDICADORES DE PERFORMANCE ECONÓMICA 019

4. GESTÃO DOS RISCOS 022

5. ÁREAS DE NEGÓCIO 028

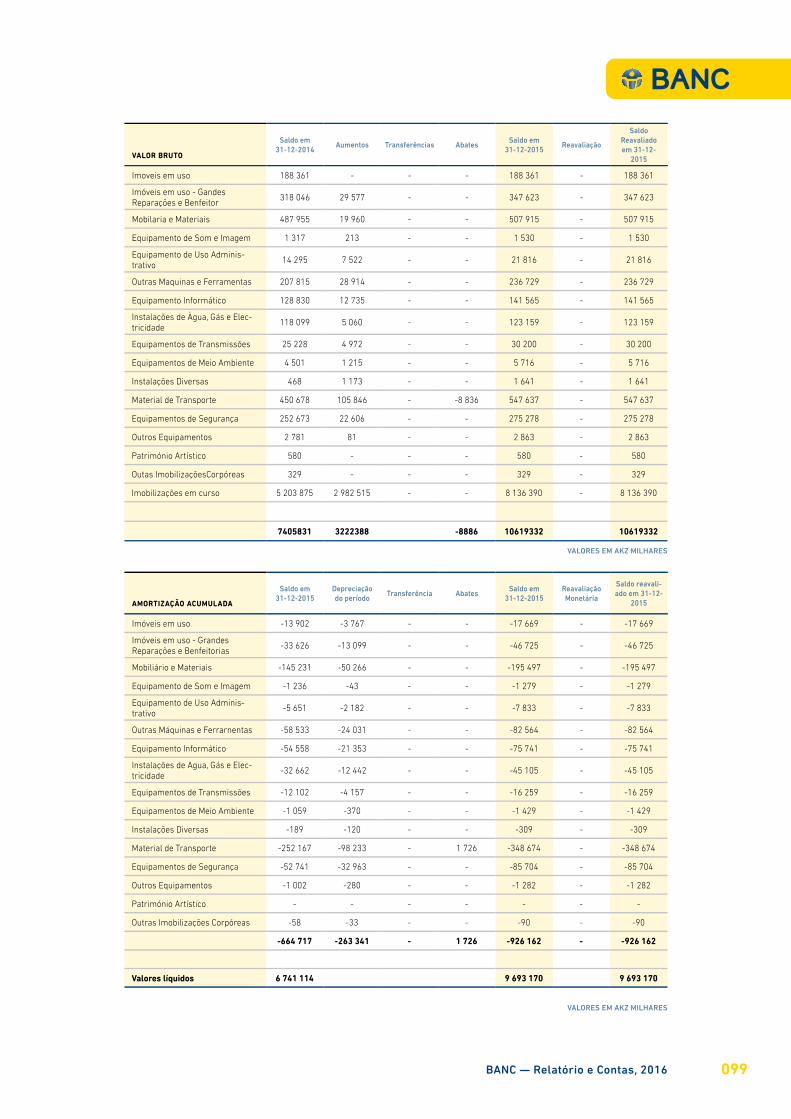

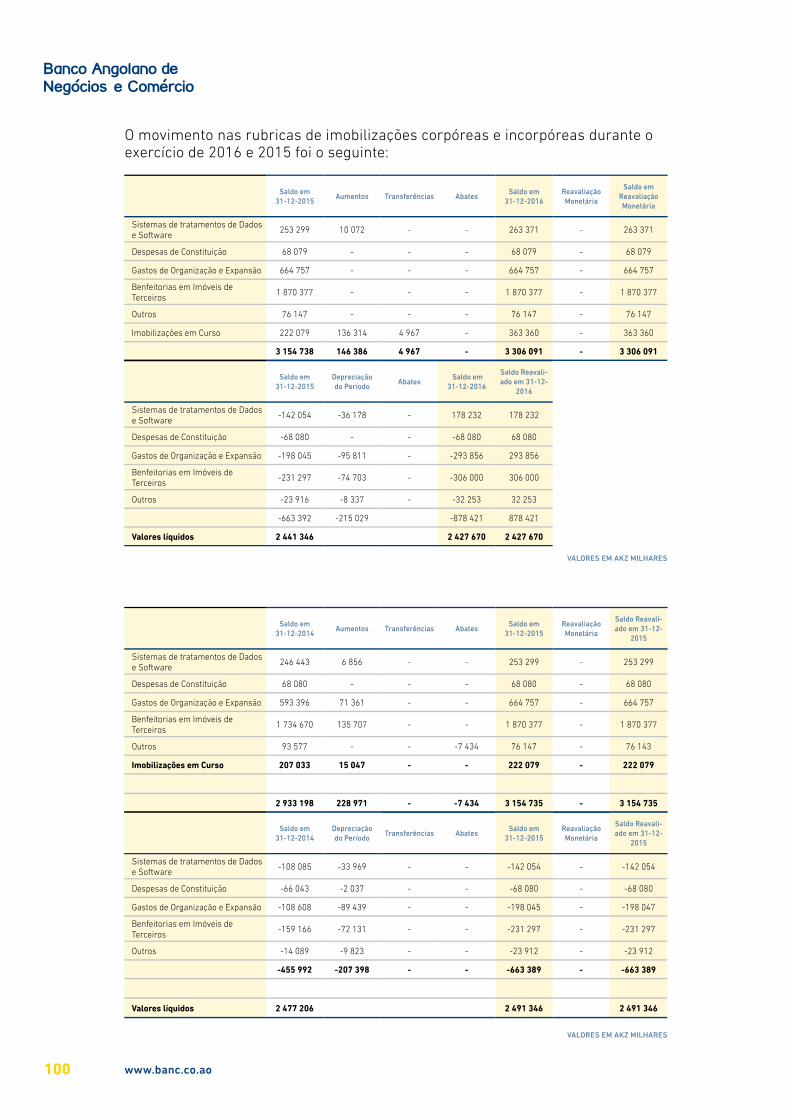

6. IMOBILIZADO 031

7. SECTOR DE MEIOS 033

8. OPERAÇÕES NACIONAIS E SOBRE O ESTRANGEIRO 036

9. RECURSOS HUMANOS 038

10. INFORMÁTICA - DESENVOLVIMENTO E SEGURANÇA 041

11. ANÁLISE FINANCEIRA 043

12. ANÁLISE ECONÓMICA 053

13. DEMONSTRAÇÕES FINANCEIRAS 059

14. RELATÓRIO DOS AUDITORES EXTERNOS 062

15. RELATÓRIO DO CONSELHO FISCAL 066

16. NOTAS ÀS CONTAS 070

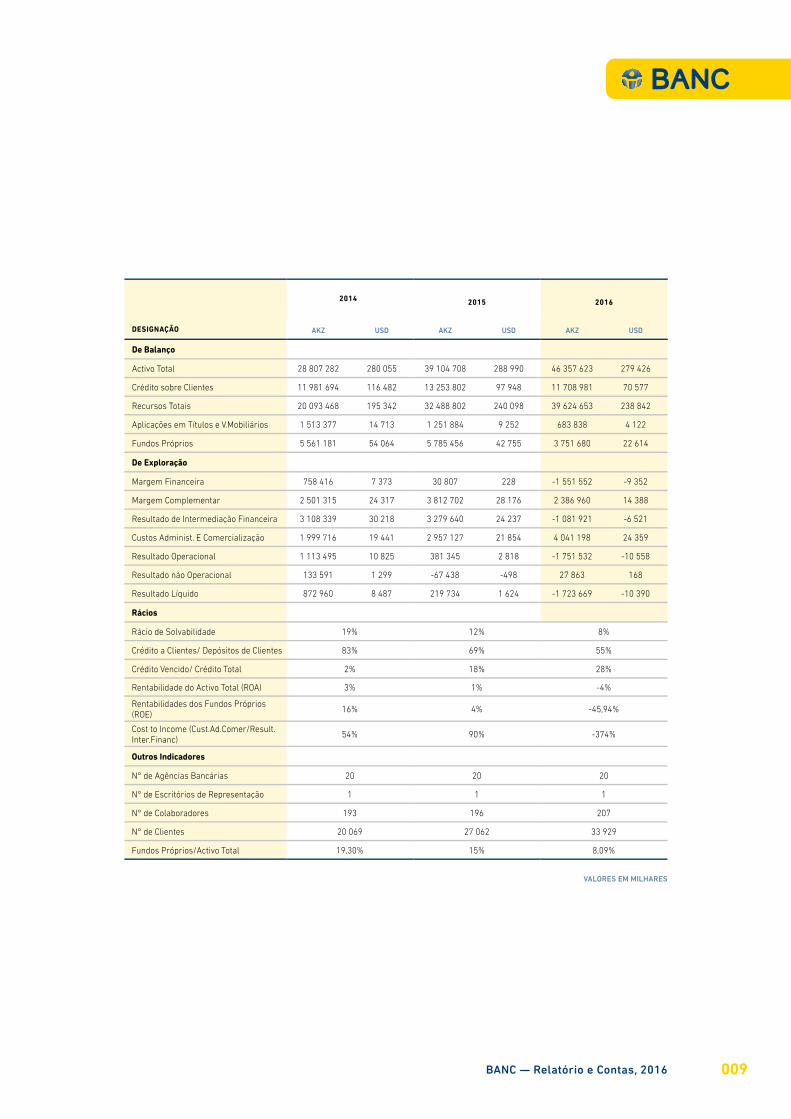

BANC — Relatório e Contas, 2016 005

1.PRINCIPAIS

INDICADORES

007BANC — Relatório e Contas, 2016

DESIGNAÇÃO

2014 2015 2016

AKZ USD AKZ USD AKZ USD

De Balanço

Activo Total 28 807 282 280 055 39 104 708 288 990 46 357 623 279 426

Crédito sobre Clientes 11 981 694 116 482 13 253 802 97 948 11 708 981 70 577

Recursos Totais 20 093 468 195 342 32 488 802 240 098 39 624 653 238 842

Aplicações em Títulos e V.Mobiliários 1 513 377 14 713 1 251 884 9 252 683 838 4 122

Fundos Próprios 5 561 181 54 064 5 785 456 42 755 3 751 680 22 614

De Exploração

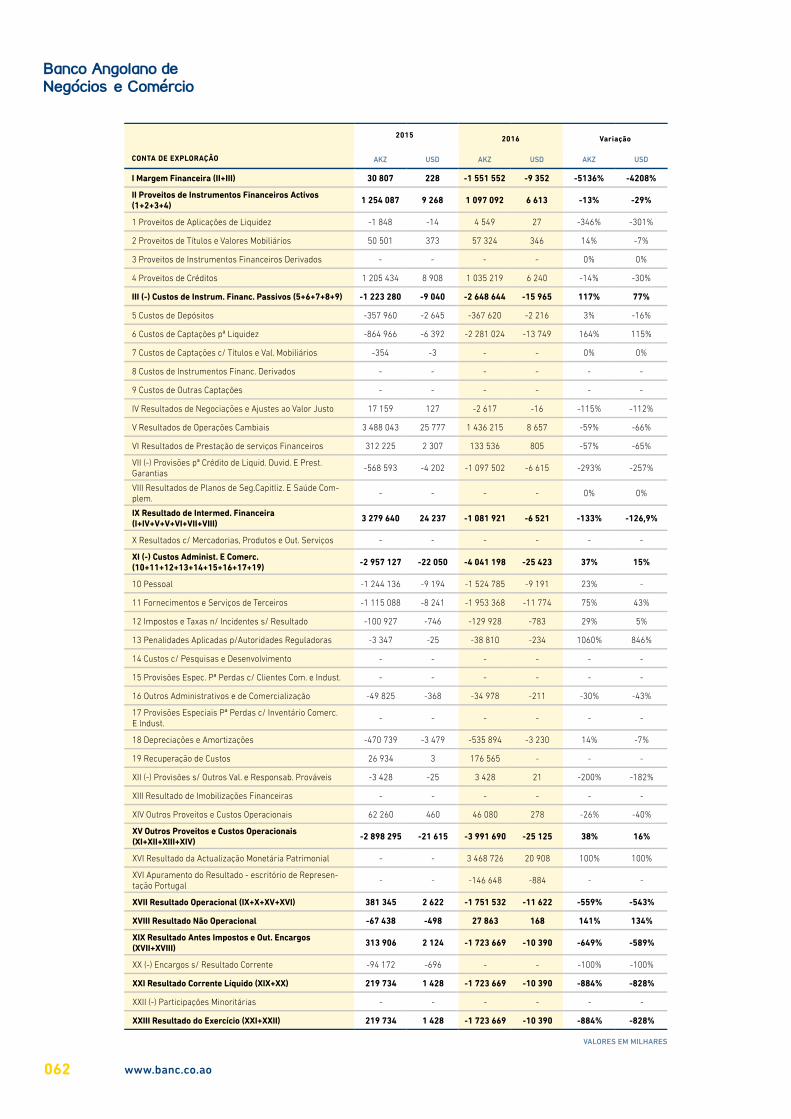

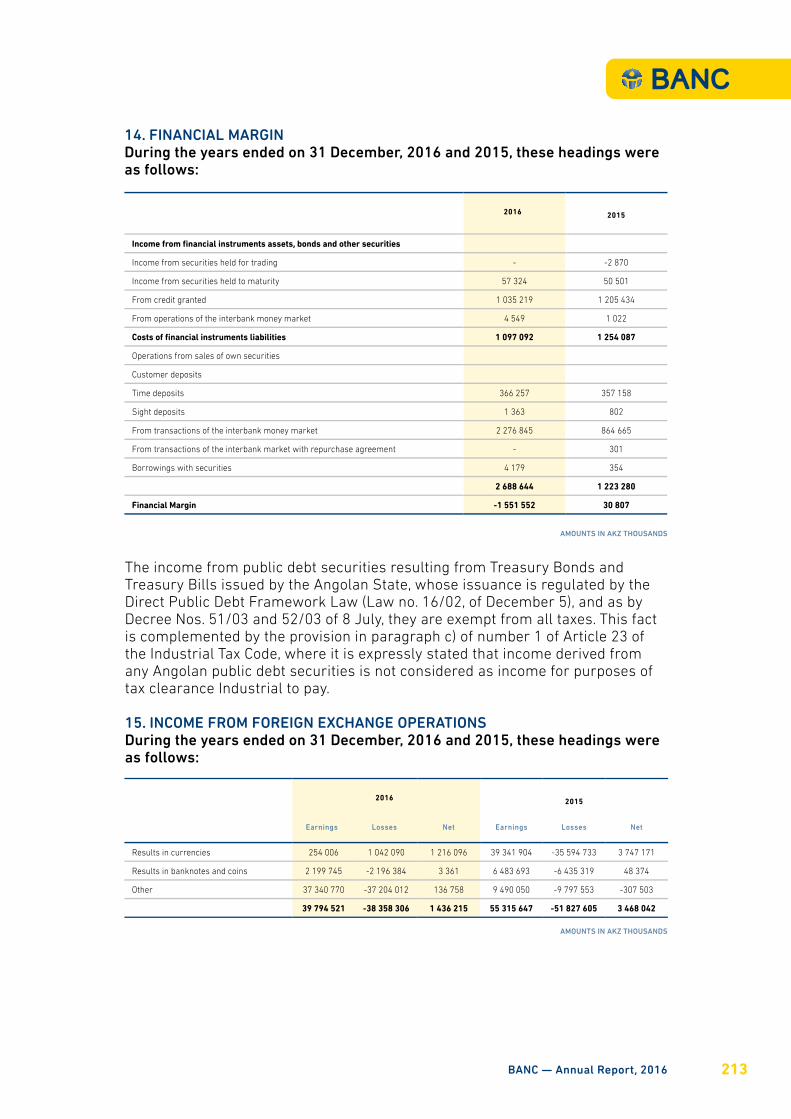

Margem Financeira 758 416 7 373 30 807 228 -1 551 552 -9 352

Margem Complementar 2 501 315 24 317 3 812 702 28 176 2 386 960 14 388

Resultado de Intermediação Financeira 3 108 339 30 218 3 279 640 24 237 -1 081 921 -6 521

Custos Administ. E Comercialização 1 999 716 19 441 2 957 127 21 854 4 041 198 24 359

Resultado Operacional 1 113 495 10 825 381 345 2 818 -1 751 532 -10 558

Resultado não Operacional 133 591 1 299 -67 438 -498 27 863 168

Resultado Líquido 872 960 8 487 219 734 1 624 -1 723 669 -10 390

Rácios

Rácio de Solvabilidade 19% 12% 8%

Crédito a Clientes/ Depósitos de Clientes 83% 69% 55%

Crédito Vencido/ Crédito Total 2% 18% 28%

Rentabilidade do Activo Total (ROA) 3% 1% -4%

Rentabilidades dos Fundos Próprios (ROE)

16% 4% -45,94%

Cost to Income (Cust.Ad.Comer/Result.Inter.Financ)

54% 90% -374%

Outros Indicadores

N° de Agências Bancárias 20 20 20

N° de Escritórios de Representação 1 1 1

N° de Colaboradores 193 196 207

N° de Clientes 20 069 27 062 33 929

Fundos Próprios/Activo Total 19,30% 15% 8,09%

VALORES EM MILHARES

BANC — Relatório e Contas, 2016 009

2.AMBIENTE ECONÓMICO

2.1 INTERNACIONAL

Durante o ano de 2016, a economia mundial pautou-se por uma linha de crescimento bastante volátil, oscilando entre períodos de grande produtividade e períodos de grande contracção na criação de riqueza. Este cenário teve forte reflexo no fortalecimento da actividade comercial internacional, nos períodos de maior estabilidade político/social, enquadradas com pequenas valorizações das matérias-primas, com especial destaque para o mercado petrolífero. Por outro lado, a perda de confiança dos investidores nas políticas de financiamento e de crédito à economia em ambiente de baixa valorização dos activos financeiros nas principais bolsas mundiais, como sejam as bolsas de Nova Iorque, de Tóquio e de Londres, afectaram grandemente a criação de emprego, e de novas empre- sas,o investimento empresarial e a criação de valor para as suas economias. Esta situação foi potencializada por factores negativos como o Brexit.

2.1.1 ECONOMIAS DESENVOLVIDAS A previsão de crescimento para 2017 atribuído às economias desenvolvidas é de 1,9%, o que equivale à estagnação da economia, pois em 2015 o nível de crescimento económico das economias desenvolvidas foi precisamente o mesmo (1,9%). Para isso, muito contribui o desempenho das economias dos Estados Unidos, Reino Unido, Canadá e Japão. Os Estados Unidos tiveram um crescimento de 3,2% em 2016, superando o crescimento obtido em 2015 em 0,3%. O Reino Unido acusou uma quebra de 0,3% relativamente ao crescimento de 2,2%, realizado em Dezembro de 2015, revelando uma economia em recessão, sofrendo as consequências do ambiente de incerteza e de alguma agitação político/económica em torno do Brexit. O Japão arrasta-se desde 2008 com uma economia que varia entre a recessão e a estagnação, o que se pode aferir do crescimento económico alcançado em 2016 na ordem dos 0,5%, que foi obtido igualmente no ano anterior.

2.1.2 ZONA EUROO relatório da Organização para a Cooperação e o Desenvolvimento Económico (OCDE), concluiu que em 2016 o desempenho económico do continente europeu foi fraco. Todavia, a Zona Euro observou um crescimento do Produto Interno Bruto (PIB) de 0,3% no primeiro trimestre de 2016, face a igual período do ano anterior, tendo elevado a produção de riqueza da região para 1,7%. Essa fase de maior expansão do crescimento do PIB teve o seu alicerce no aumento das exportações de bens verificadas nos sectores da Indústria e, em menor escala, dos serviços, que resultaram de um euro mais fraco, do aumento da procura por exportações de serviços, como turismo e viagens para a Zona Euro. Neste particular, destacaram-se as quatro maiores economias do euro, como sejam a Espanha, onde o Índice dos Gestores de Compras (PMI) aponta uma subida de 55,5 pontos no primeiro trimestre de 2016, seguidos da Alemanha com 55,2 pontos percentuais. Em França, o PMI avançou para 53,1 pontos e em Itália para os 55,2 pontos percentuais.

A agência de estatísticas da União Europeia, Eurostat, informou que o PIB dos 19 países cresceu 0,3% no mês de Junho, representando uma desaceleração face a igual período do ano anterior, onde o crescimento do PIB fixou-se em 0,6%. Esta fase de menor crescimento económico da Zona Euro coincidiu com

BANC — Relatório e Contas, 2016 011

a alta do desemprego, herdado da crise de 2008, elevada dívida pública e privada, problemas resultantes do elevado risco de crédito da banca europeia, uma política de maior controlo e acerto na subida das taxas de juros por parte do Banco Central Europeu e o impacto do problema dos refugiados, trazendo aumento das preocupações com a segurança, contribuindo para um clima de maiores incertezas, com fortes repercussões no investimento, na produtividade e nas políticas de reforma.

O terceiro e o quarto trimestre observaram um desempenho relativamente positivo, sendo que entre o mês de Julho e Setembro o crescimento económico da Zona Euro foi mais discreto, tendo em conta o impacto da pressão da saída do Reino Unido da União Europeia. O que resultou num crescimento de 0,3% sobre igual trimestre do ano anterior. O quarto trimestre foi bem melhor em termos de crescimento, tendo elevado o PIB para os 3,9%.

2.1.3 SAÍDA DO REINO UNIDO DA UNIÃO EUROPEIA - BREXITA saída do Reino Unido da União Europeia provocou o pânico no mercado imobiliário britânico, onde após vários anos de pleno crescimento, os sinais de instabilidade começaram a fazer-se sentir. Em consequência disso, os principais investidores do sector imobiliário inglês exigiram o retorno dos seus investimentos aos quatro fundos de investimento imobiliário, que asseguram o êxito dos investimentos feitos no sector imobiliário, garantindo o retorno do capital e dos lucros dos negócios realizados no mercado imobiliário inglês. A Standard Life, a Aviva Investors, a Henderson Global Investors e a M&G Investments juntas movimentam nove mil milhões de Libras Esterlinas de activos no imobiliário comercial. Não obstante, foram incapazes de gerar o retorno do investimento aos principais investidores do sector imobiliário, sendo obrigadas a encerrar temporariamente a sua actividade, originando uma queda na Bolsa de Valores de Londres.

A Libra esterlina atingiu o seu valor mais baixo face ao US Dólar em 31 anos, tendo registado uma descida de 15% depois do referendo. A desvalorização da Libra afectou grandemente o orçamento das famílias britânicas, reduzindo o seu poder de compra, contribuindo para um menor crescimento do consumo e da procura interna. Por esta razão, a criação de emprego reduziu-se para cerca de metade, muito embora a taxa de desemprego tenha baixado para 5%, a mais baixa dos últimos 11 anos.

Por outro lado, a desvalorização da Libra no mercado cambial favoreceu as empresas exportadoras de mercadorias, uma vez que os seus produtos exportados se tornaram mais competitivos no espaço europeu, o que teve impacto positivo na balança comercial britânica. O sector dos transportes foi, porém, a excepção, tendo acusado uma baixa de 0,8% no volume de vendas de automóveis, que terá resultado da incerteza verificada na forma como deverá ser feito o acesso do Reino Unido ao mercado único.

2.1.4 ECONOMIAS EMERGENTESAs economias emergentes tiveram um desempenho positivo em 2016, globalmente falando, pois aceleraram para os 4,3% do PIB. Todavia, o crescimento económico não foi uniforme em todos os países, a economia

www.banc.co.ao012

chinesa manteve o curso de desaceleração registando 6,7%, em Dezembro de 2016, face aos 6,9% do período homólogo. À semelhança de 2015, a Índia continua a ser o país que mais cresceu no mundo, tendo registado uma expansão de 7,6%, não obstante os efeitos da desaceleração da China.

A recessão foi a tónica dominante das economias da América Latina e Caribe, onde se destaca o Brasil cuja economia foi afectada por um clima de instabilidade política e convulsões sociais, aliadas a processos judiciais públicos sobre algumas das maiores empresas de produção petrolífera da região. O Brasil debate-se com um elevado déficit das contas públicas, agravadas pela má gestão dos recursos fiscais e pelo aumento da dívida pública, o que afectou o processo de expansão económica do país, fixando a retração do PIB em 3,3%. Os países emergentes do Médio Oriente obtiveram uma ligeira expansão, que não pôde ser mais robusta, em virtude da região ter sido bastante afectada por conflitos internos, tensões geopolíticas e pelo baixo preço do petróleo, fixando o seu crescimento em 2,9%. A Rússia continua em recessão profunda, que exige uma postura de equilíbrio e ajuste às sanções do Ocidente e aos preços baixos do petróleo, o que não favorece o crescimento da actividade económica. O crescimento do Sul da Ásia deverá atingir os 7,1% em 2016, o que espelha uma quebra de 1,1% face a 2015. Nesta região, o consumo das famílias revelou ser um dos indicadores de desempenho económico de maior destaque.

2.1.5 ECONOMIAS MENOS DESENVOLVIDASOs baixos preços das matérias-primas no mercado internacional resultando em menores receitas provenientes da exportação, aliadas à falta de divisas, à baixa produção de energia e à débil confiança dos investidores, amputou o crescimento económico dos países menos desenvolvidos. A Venezuela debateu-se em 2016 com uma inflação galopante e uma elevada taxa de desemprego, tendo sofrido uma forte contração do PIB de 9,7% em 2016. Angola, por sua vez, enfrenta o desafio da adaptação aos baixos preços das matérias-primas, com especial destaque para o petróleo, em paralelo com uma crise económica e cambial com fortes repecursões no volume de expor- tações e na subida generalizada dos preços dos produtos da cesta básica, conduzindo à estagnação da economia.

A Africa Subsariana cresceu 0,2%, fixando a sua expansão económica em 1,4% do PIB. A região foi afectada por muitos conflitos internos, instabilidade política, doenças infecciosas, ataques terroristas em grande escala, escassez de divisas e a saída massiva de capitais estiveram na base da dificuldade de consolidação de políticas e estratégias de promoção do emprego, produtividade e incremento da oferta de produtos e serviços diversificados. Outro factor de grande preocupação patente nos países menos desenvolvidos é a pressão da emigração para a europa e outros países mais desenvolvidos, o que reduziu a população activa.

2.1.6 MERCADO CAMBIALO mercado cambial internacional destacou-se pela forte valorização do US Dólar face às principais moedas de transacção nos mercados financeiros. Por esta razão, a média anual do EUR/USD em 2016 foi de 1,11, valor igual ao de 2015, o que revelou ser a média mais baixa dos ultimos anos. O factor “Trump” pode vir a ser determinante para a paridade entre o US Dólar e o Euro, a média prevista

BANC — Relatório e Contas, 2016 013

é de 1,05 (EUR/USD). Este facto aponta para o bom momento que a economia americana está a viver desde o segundo trimestre de 2015. O Índice do dólar DXY relativamente ao cabaz de moedas composto pelo Euro, o Iene, a Libra Esterlina o Franco suiço, o Dólar canadiano e a Coroa sueca, determinou no início de 2016, uma vantagem para o US Dólar de 99 pontos, que paulatinamente subiu acima dos 100 pontos no final do ano transacto. O US Dólar continuará a valorizar face ao Iene, passando dos actuais (JPY/USD) 115, para 120 ienes por cada dólar.

2.1.7 DESEMPREGOA taxa de desemprego baixou na maior parte dos países do globo, fruto de um percurso de expansão da economia mundial, consolidado durante o ano de 2016. Por esta razão o incremento do investimento nos sectores mais produtivos da economia mundial proporcionou o aumento da produtividade e da consequente exportação de produtos e serviços, com forte impacto na política de criação de novos postos de trabalho. O aumento do poder de compra das famílias resultou no incremento do consumo interno e externo que se traduziu na âncora da consolidação das políticas de emprego nas economias mais produtivas. É pertinente, dentro deste quadro, realçar a taxa de desemprego registada nos Estados Unidos da América que se fixou em 4,7% da população activa, face aos anteriores 4,80% do ano anterior. A taxa de desemprego da Zona Euro com excepção da Itália fixou-se em 9,6%, contra 12% apurado em Dezembro de 2015. O Brasil e a Itália apresentaram uma taxa de desemprego de 12%, à semelhança do que apuraram em igual período do ano anterior. As economias com pior desempenho nesta matéria são o Djibuti, com uma taxa de desemprego de 54%; a África do Sul, República do Congo, Angola e Palestina, todas com uma taxa de desemprego de 26%; e finalmente, o Lesoto, Macedónia, Grécia, Guiné Equatorial, Montenegro, Gabão e Espanha, com taxas de desemprego que variam entre os 25% a 18,5% da população activa.

2.1.8 RISCOS E CAUTELAS SOBRE A ECONOMIA MUNDIALA economia mundial padece de algumas situações de risco que se revestem de peso preocupante. Desde logo podemos destacar as consequências do Brexit, que poderão conduzir ao reforço dos níveis de protecionismo, perturbações políticas e espírito de independentismo, que poderá colocar em causa o projecto europeu. As eleições na Alemanha poderão ter forte impacto sobre a economia europeia em 2017. A fragilidade da banca europeia, com especial destaque para a banca Italiana, aliada com o volume de crédito de cobrança duvidosa, revelam ser um factor de enorme risco para a economia mundial.

Na qualidade de ser um dos países de maior poderio económico mundial, as alterações estruturais e a desaceleração económica da China, em linha com os ajustamentos das economias emergentes às fortes mudanças da economia mundial, prefiguram um ambiente de elevada incerteza que acarretarão riscos severos. Um factor de risco de instabilidade económica generalizada é a manutenção dos preços baixos das matérias-primas, uma vez que tanto os países em desenvolvimento como os países emergentes dependem muito das exportações das mesmas para a consolidação e expansão das suas economias. Por fim, destacamos as consequências do efeito “Trump” sobre toda a economia global. Torna-se muito preocupante a política de gestão das taxas de juro da Reserva Federal Americana (FED), que poderão fortalecer o US Dólar face às principais moedas de referência no mercado cambial internacional, tornando

www.banc.co.ao014

o crédito mais oneroso e o reembolso do crédito muito mais difícil. Este cenário aponta para o risco de uma “bolha” de crédito que poderá conduzir, entre outras coisas, ao colapso da economia americana, com consequências imprevisíveis para a economia mundial.

Com todos os factores de risco apontados acima, a economia mundial apresentou um percurso consistente com a desaceleração do seu crescimento económico, tendo fixado a sua evolução em 3% em Dezembro de 2016, contra 3,1% alcançados no período homólogo de 2015.

2.2 NACIONAL

Desde 2007 que a economia angolana se tem debatido com a desaceleração do crescimento do seu Produto Interno Bruto (PIB), sendo este um facto que antecede a grande crise imobiliária que eclodiu nos Estados Unidos da América em 2008. Na base deste percurso está sem dúvida a quebra progressiva dos preços das matérias-primas nos mercados internacionais. Neste âmbito podemos destacar a redução drástica do preço do petróleo, que teve como fortes consequências a redução das receitas, a menor disponibilidade de divisas, a necessária contenção das despesas do Estado e um menor estímulo deste na economia. O quadro que se gerou em função disso foi a forte redução das importações, com impacto na redução da capacidade produtiva das empresas que mais dependiam das mesmas para sustentarem a produção, resultando num grande número de falências.

O menor volume de importações obrigou as empresas nacionais a um maior esforço financeiro para cobrir a importação dos seus produtos comerciais, o que resultou no incremento do preço de venda dos mesmos, contribuindo grandemente para a subida dos preços. O poder de compra das famílias angolanas sofreu uma forte quebra face à subida da inflação no decorrer do ano de 2016. Este cenário desencadeou a necessidade de se apostar na diversificação da economia como uma das formas de combater a fraca produtividade, recuperando a produção nacional e a criação de mais emprego.

De acordo com o Fundo Monetário Internacional (FMI), os níveis da dívida pública angolana estão a atingir limites insustentáveis, uma vez que, de acordo com os cálculos daquele organismo, o índice da dívida pública relativamente ao PIB atinge os 70%. Tal facto tem sido uma enorme preocupação para o Estado angolano, que num cenário de receitas reduzidas, tem vindo a endividar-se junto da Banca. O que sujeitou o Estado a compromissos avultados para as gerações futuras e a inevitabilidade de uma política de austeridade fiscal.

O FMI estima que a economia angolana cresça 3,5% em 2016 menos 0,7% face a 2015. Este desempenho demonstra que a economia de Angola está em desaceleração. As dificuldades que o Estado angolano experimenta na implementação de políticas económicas eficazes, capazes de minimizar a burocracia excessiva, criar um ambiente propício ao investimento privado e o estabelecimento de negócios, fortalecendo o primado da lei, melhorando as infra-estruturas físicas e o capital humano, conduziram o FMI a prever a estagnação da economia em 2017.

BANC — Relatório e Contas, 2016 015

2.3 INFLAÇÃO

A taxa de inflação prevista pelo FMI para Angola para o 1º semestre de 2016, situava-se em 19,2% e no ano seguinte em 14%. Todavia, a dinâmica da evolução dos preços dos produtos da cesta básica obrigou o Fundo Monetário Internacional a rever as suas previsões no fim de ano. Por esta razão o FMI ajustou a sua previsão da taxa de inflação para 48% em 2016 e 32% para o ano de 2017.

Para 2016, os dados disponibilizados pelo BNA (Banco Nacional de Angola) relativamente à taxa de inflação mensal e acumulada nos últimos quatro meses do ano, revelam uma taxa média em torno dos 2,06%. Nos oito meses anteriores os níveis de inflação foram sempre mais elevados, sendo que a taxa de inflação média mensal foi de 3,42%. Com este trajecto de subida a taxa de inflação acumulada passou de 14,27% em 2015, para 41,95% em 2016.

2.4 TAXA DE CÂMBIO

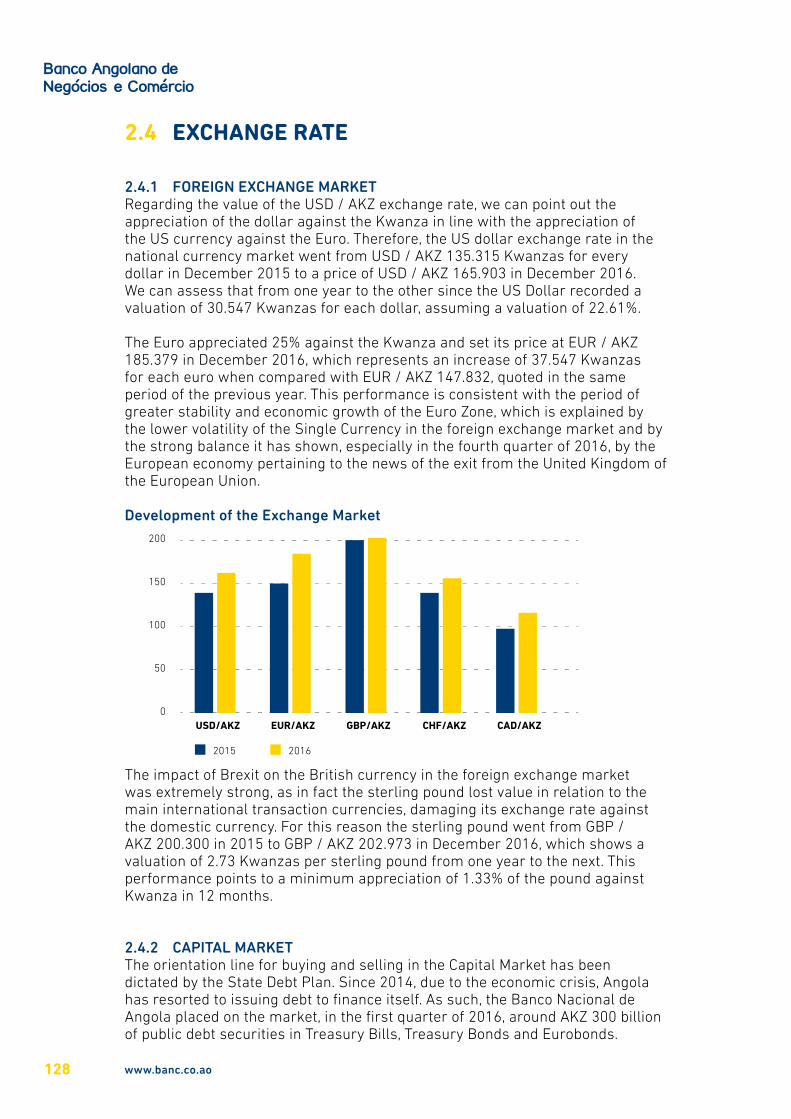

2.4.1 MERCADO CAMBIALQuanto ao valor do câmbio USD/AKZ, podemos assinalar a valorização do Dolar face ao Kwanza em linha com a valorização da moeda norte-americana face ao Euro. Assim sendo, a cotação do US Dólar no mercado cambial nacional passou de USD/AKZ 135,315 Kwanzas por cada dólar, em Dezembro de 2015, para uma cotação de USD/AKZ 165,903 em Dezembro de 2016. Podemos aferir que de um ano para o outro o US Dolar registou uma valorização de 30,547 Kwanzas por cada Dolar, pressupondo uma valorização de 22,61%.

O Euro valorizou 25% face ao Kwanza, tendo fixado a sua cotação em EUR/AKZ 185,379, em Dezembro de 2016, o que representa um incremento de 37,547 Kwanzas por cada euro comparando com EUR/AKZ 147,832, cotados em igual período do ano anterior. Este desempenho é consistente com o período de maior estabilidade e crescimento económico da Zona Euro, o que se explica pela menor volatilidade da moeda única no mercado cambial e pelo forte equilíbrio demonstrado, sobretudo no quarto trimestre de 2016, pela economia europeia face à notícia da saída do Reino Unido da União Europeia.

Evolução do Mercado Cambial250

200

150

100

50

0USD/AKZ

2015 2016

EUR/AKZ GBP/AKZ CHF/AKZ CAD/AKZ

www.banc.co.ao016

O impacto do Brexit sobre a moeda britânica no mercado cambial foi muito forte, pois de facto a Libra perdeu valor face às principais moedas de transação internacional, prejudicando a sua evolução cambial face à moeda nacional. Por essa razão a Libra passou de uma cotação de GBP/AKZ 200,300 em 2015, para uma cotação de GBP/AKZ 202,973, em Dezembro de 2016, o que denota uma valorização de 2,673 Kwanzas por Libra de um ano para o outro. Este desempenho aponta para uma valorização mínima de 1,33% da Libra face ao Kwanza em 12 meses.

2.4.2 MERCADO DE CAPITAISA linha de orientação para compra e venda no mercado de capitais tem sido ditada pelo Plano de Endividamento do Estado. Desde 2014, devido à crise económica, o país vem recorrendo à emissão de dívida para se financiar. Assim sendo, o Banco Nacional de Angola colocou no mercado, no primeiro trimestre de 2016, perto de AKZ 300 mil milhões de títulos da dívida pública em Bilhetes do Tesouro, Obrigações do Tesouro e Eurobonds.

O stock da dívida pública atingiu em 2015, USD 42,9 mil milhões, equivalentes a EUR 39 mil milhões de euros, o que corresponde a 48,7% do Produto Interno Bruto. Os juros da dívida interna irão custar aos cofres do Estado mais de AKZ 261.873 milhões, equivalentes a USD 1.578 milhões, enquanto os juros da dívida contraída no exterior do país irão custar ao Estado angolano cerca de AKZ 222.284 milhões, equivalentes a USD 1.339 milhões. No final do primeiro trimestre de 2016, o Banco Nacional de Angola colocou no mercado primário AKZ 74,6 mil milhões (USD 449,6 milhões) em Bilhetes do Tesouro (BT) e AKZ 17,2 mil milhões (EUR 97,7 milhões) em Obrigações do Tesouro (OT). As taxas de juro médias de emissão de BT oscilaram entre os 14,36% e os 17,12%, para as maturidades de 91 e 364 dias respectivamente, enquanto as OT fecharam com taxas de juro que variaram entre 7% e 7,77%, para as mesmas maturidades. No segmento de venda directa de títulos ao público, o Banco Nacional de Angola realizou só na última semana do mês de Março de 2016 vendas em torno de AKZ 1,7 mil milhões, equivalentes a EUR 9,7 milhões.

No final do mês de Dezembro de 2016, o Banco Nacional de Angola emitiu AKZ 44,6 milhões, equivalentes a EUR 257,1 milhões em Bilhetes do Tesouro e AKZ 26,4 mil milhões, equivalentes a EUR 152,2 milhões em Obrigações do Tesouro. Na última semana do ano, o BNA emitiu títulos da dívida pública que ascenderam a AKZ 70.791 milhões, equivalentes a EUR 379 milhões em Bilhetes do Tesouro e AKZ 22.266 milhões, equivalentes a EUR 119,2 milhões em Obrigações do Tesouro. Desse modo, o stock total da dívida angolana em 2016 atingiu AKZ 1.654,1 mil milhões, em linha com o OGE de 2015. É digno de nota que o Estado tenha emitido durante o ano de 2016 dívida no montante equivalente a 2,2 mil milhões de Euros, correspondentes a AKZ 402.750 milhões em Obrigações do Tesouro para o pagamento de despesas públicas atrasadas desde 2013.

De acordo com o Centro de Estudos e Investigação Científica da Universidade Católica (CEIC), o stock da dívida pública poderá atingir 75% do PIB em 2017. De acordo com os dados disponibilizados pelo Ministério das Finanças, o stock da dívida pública baixará para os 52,7% do PIB. Todavia, o Plano Anual de Endividamento do Estado angolano prevê para este ano necessidades

BANC — Relatório e Contas, 2016 017

de endividamento na ordem dos AKZ 4.667 mil milhões, equivalentes a USD 28,1 mil milhões para financiar as despesas previstas no Orçamento Geral do Estado para 2017.

Para cumprir este objectivo o Estado pretende acabar com o monopólio dos Bancos da praça nacional como investidores exclusivos do mercado de títulos. Em 2017 o Estado pretende alargar a base de investidores no concurso de financiamento da dívida pública. Além dos Bancos angolanos, existem outras instituições com apetência para o investimento que poderão contribuir para compra de dívida do Estado. Por esta razão o Estado pretende contar com a participação dos Fundos de Pensões, Seguradoras e outros fundos. Segundo a Agência Lusa, para o ano de 2017, o Estado prevê emitir Bilhetes do Tesouro no valor de AKZ 1.568 bilhões (USD 9,4 mil milhões), e Obrigações do Tesouro 1.803 bilhões (USD 10,8 mil milhões). Será, portanto, dentro desta base, que o stock da dívida angolana será incrementado, o que é consistente com a análise e previsão do Coordenador do CEIC.

As Reservas Internacionais Líquidas (RIL) de Angola para a cobertura de importações e a cobertura das dívidas do Estado angolano, sofreram uma quebra de 12%, tendo passado de USD 24.266 milhões, equivalentes a EUR 22.905 milhões, em Dezembro de 2015, para USD 21.399 milhões, equivalentes a EUR 20.204 milhões a 31 de Dezembro de 2016. O que se traduz em uma perda de USD 2.867 milhões, equivalentes a EUR 2.706,8 milhões. O valor das RIL em 2016 permitiu a Angola a cobertura de aproximadamente 7 meses de importações, o que é manifestamente pouco para gerar confiança nos investidores nacionais.

2.5 TAXAS DE JURO

A subida da taxa de inflação, medida pela alta generalizada dos preços dos produtos da cesta básica, aliada à forte redução do volume de importações, em consonância com a queda substancial das receitas petrolíferas, estiveram na base da reunião do Comité de Política Monetária do BNA (CPM) no mês de Dezembro de 2016. Nesta reunião foram analisados os sectores Fiscal, Monetário e Externo em linha com o comportamento da economia mundial. Dessa análise genérica da economia nacional no contexto internacional resultaram as seguintes decisões:

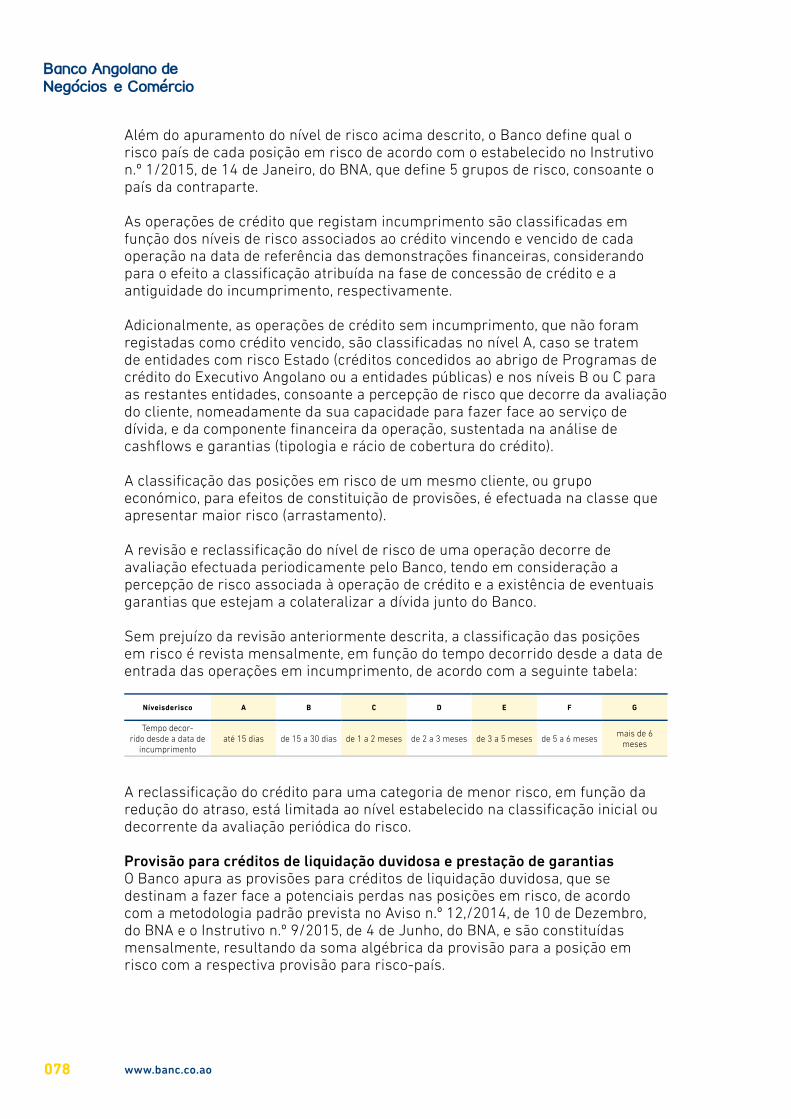

× Manter a Taxa Básica de Juro – Taxa BNA – em 16%, ao ano;

× Manter a Taxa de Juro da Facilidade Permanente de Cedência de Liquidez em 20%, ao ano;

× Manter a Taxa de Juro da Facilidade Permante de Absorção de Liquidez a sete dias em 7,25%, ao ano.

A Taxa de Juro de Redesconto passou de 12,5% em Dezembro de 2015 para 20% em igual período de 2016.

www.banc.co.ao018

Relativamente às taxas de juro praticadas no mercado interbancário (MMI), as operações de tomadas e cedências de liquidez tornaram-se mais atraentes do que as operações processadas no mercado de capitais.

Em Dezembro de 2016 a taxa de juro de referência Luibor para as operações de trinta dias fixou-se em 17,41%, contra os anteriores 11,44%, em igual período de 2015, o que demonstra uma evolução positiva de 52%, que se traduz num aumento de 5,97 pontos percentuais. Para as operações de 3 meses a taxa de referência Luibor fixou-se em 18,23% em Dezembro de 2016, contra 11,88% de Dezembro de 2015, o que representa uma evolução de 53,45%. A taxa de juro para as operações de cedência e tomada de liquidez por um período de 12 meses registaram uma evolução de 57%, tendo passado de uma taxa de juro de 12,84% em Dezembro de 2015, para 20,17% em igual período de 2016.

Os Bilhetes do Tesouro mereceram o maior destaque por parte do Estado angolano por serem títulos de curta maturidade, nos quais o retorno do capital aplicado é mais rápido. Assim sendo, em Dezembro de 2016, os Bilhetes do Tesouro com maturidades de 91 dias foram negociados à taxa de juro de 16,38%, contra 13,90% de igual período do ano anterior. No mesmo período os Bilhetes do Tesouro com maturidade de 182 dias foram negociados à taxa de juro de 23,92%, contra 14,95% praticada em Dezembro de 2015, pelo que podemos concluir que as taxas de juro de remuneração do capital aplicado observaram uma evolução entre os 18% e os 60% para as maturidades de duração mais longa.

As Obrigações do Tesouro nacional foram negociadas em menor volume do que os Bilhetes do Tesouro. Os investidores têm preferência pelos Bilhetes do Tesouro pois as Obrigações do Tesouro são títulos de remuneração de médio prazo, o que no actual contexto de crise económica e de contenção dos gastos não são tão atraentes para os investidores. As Obrigações do Tesouro com maturidades de dois, três, quatro e cinco anos foram negociados a taxas de juro de 7%, 7,25%, 7,50% e 7,75% respectivamente, à semelhança do que aconteceu no ano transacto.

Evolução do Mercado Cambial

25,00%

20,00%

15,00%

10,00%

5,00%

0,00%

1 DIA

2015 2016

1 M 3 M 6 M 9 M 12 M

BANC — Relatório e Contas, 2016 019

3.INDICADORES DE PERFORMANCE ECONÓMICA

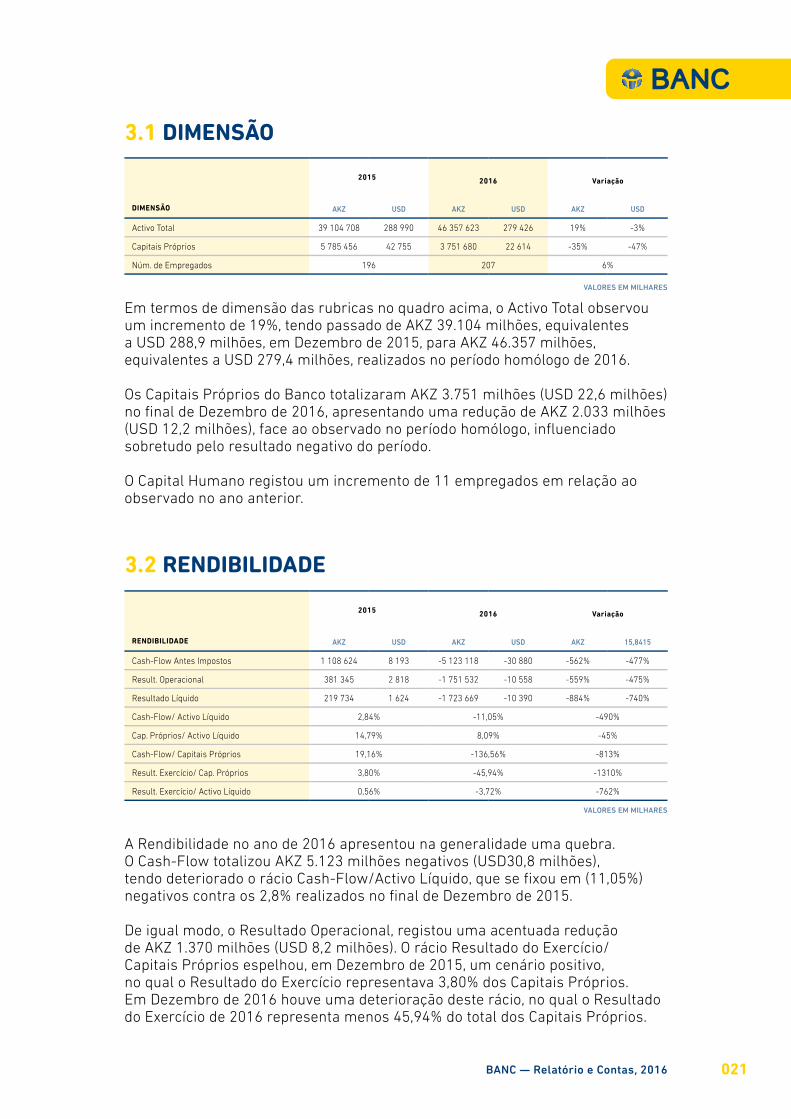

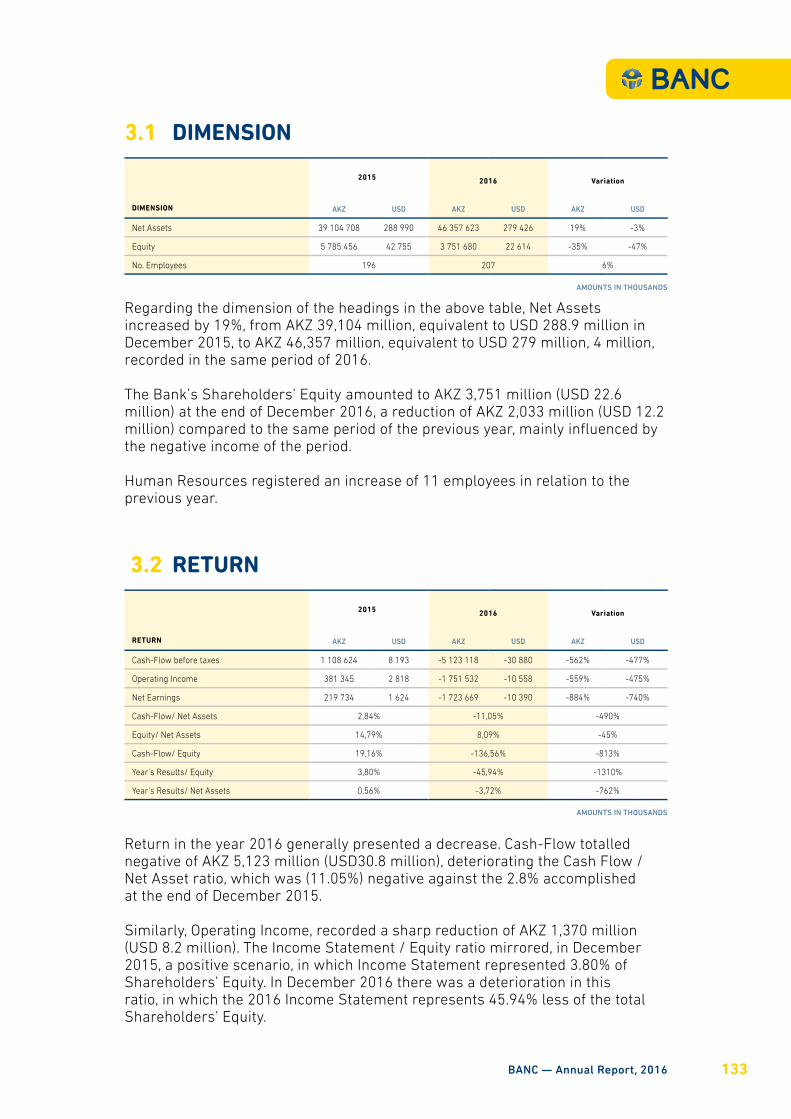

3.1 DIMENSÃO

DIMENSÃO

2015 2016 Variação

AKZ USD AKZ USD AKZ USD

Activo Total 39 104 708 288 990 46 357 623 279 426 19% -3%

Capitais Próprios 5 785 456 42 755 3 751 680 22 614 -35% -47%

Núm. de Empregados 196 207 6%

VALORES EM MILHARES

Em termos de dimensão das rubricas no quadro acima, o Activo Total observou um incremento de 19%, tendo passado de AKZ 39.104 milhões, equivalentes a USD 288,9 milhões, em Dezembro de 2015, para AKZ 46.357 milhões, equivalentes a USD 279,4 milhões, realizados no período homólogo de 2016.

Os Capitais Próprios do Banco totalizaram AKZ 3.751 milhões (USD 22,6 milhões) no final de Dezembro de 2016, apresentando uma redução de AKZ 2.033 milhões (USD 12,2 milhões), face ao observado no período homólogo, influenciado sobretudo pelo resultado negativo do período.

O Capital Humano registou um incremento de 11 empregados em relação ao observado no ano anterior.

3.2 RENDIBILIDADE

VALORES EM MILHARES

RENDIBILIDADE

2015 2016 Variação

AKZ USD AKZ USD AKZ 15,8415

Cash-Flow Antes Impostos 1 108 624 8 193 -5 123 118 -30 880 -562% -477%

Result. Operacional 381 345 2 818 -1 751 532 -10 558 -559% -475%

Resultado Líquido 219 734 1 624 -1 723 669 -10 390 -884% -740%

Cash-Flow/ Activo Líquido 2,84% -11,05% -490%

Cap. Próprios/ Activo Líquido 14,79% 8,09% -45%

Cash-Flow/ Capitais Próprios 19,16% -136,56% -813%

Result. Exercício/ Cap. Próprios 3,80% -45,94% -1310%

Result. Exercício/ Activo Líquido 0,56% -3,72% -762%

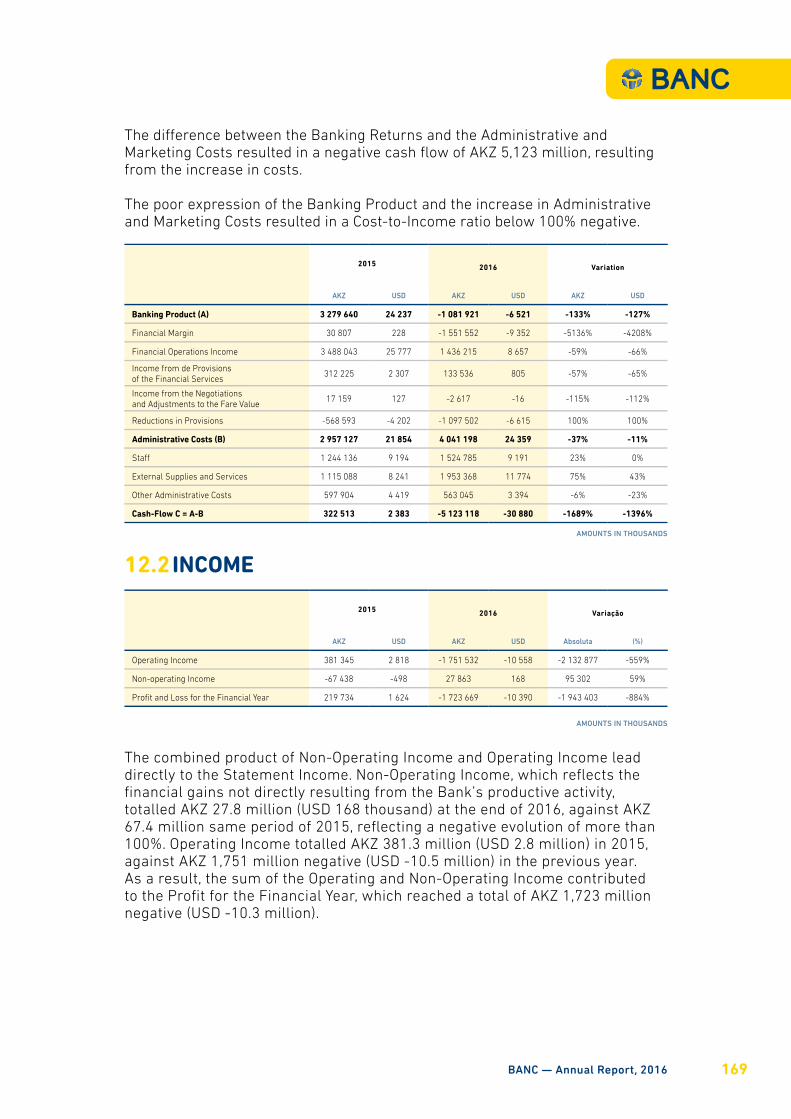

A Rendibilidade no ano de 2016 apresentou na generalidade uma quebra. O Cash-Flow totalizou AKZ 5.123 milhões negativos (USD30,8 milhões), tendo deteriorado o rácio Cash-Flow/Activo Líquido, que se fixou em (11,05%) negativos contra os 2,8% realizados no final de Dezembro de 2015.

De igual modo, o Resultado Operacional, registou uma acentuada redução de AKZ 1.370 milhões (USD 8,2 milhões). O rácio Resultado do Exercício/ Capitais Próprios espelhou, em Dezembro de 2015, um cenário positivo, no qual o Resultado do Exercício representava 3,80% dos Capitais Próprios. Em Dezembro de 2016 houve uma deterioração deste rácio, no qual o Resultado do Exercício de 2016 representa menos 45,94% do total dos Capitais Próprios.

BANC — Relatório e Contas, 2016 021

3.3 PRODUTIVIDADE E EFICIÊNCIA

PRODUTIVIDADE/ EFICIÊNCIA

2015 2016 Variação

AKZ USD AKZ USD AKZ USD

Activo Líq./ Núm.Empregados 199 514 1 414 223 950 1 350 12% -8%

Custos de Estrutura/ Activo Líq. 7,56% 8,72% 15%

VALORES EM MILHARES

A Produtividade expressa na relação entre o Activo Líquido/Número de Empregados, espelha uma subida de 12% sobre a cifra alcançada em Dezembro de 2015. Desse modo, o resultado do rácio passou de AKZ 199,5 milhões (USD 1,5 milhões), para AKZ 223,9 milhões (USD 1,3 milhões). Este resultado deve-se ao crescimento do Activo Líquido do Banco, que observou uma subida de 19% em Dezembro de 2016.

A eficiência observou um comportamento de sentido contrário ao que foi demonstrado em matéria de produtividade. O incremento do peso dos Custos de Estrutura sobre o Activo Líquido traduziu-se em um crescimento de 8,72% em relação ao período homólogo

3.4 PRUDENCIAIS

PRUDENCIAIS

2015 2016 Variação

AKZ USD AKZ USD AKZ USD

Rácio de Solvabilidade 12% 8% -31%

O Rácio de Solvabilidade registou um decréscimo de 31%, no final de Dezembro de 2016, posicionando-se em 8%. O comportamento observado deve-se essencialmente à redução dos Fundos Próprios.

www.banc.co.ao022

4.GESTÃO

DOS RISCOS

023BANC — Relatório e Contas, 2016

Durante a actividade de 2016, o Gabinete de Gestão de Risco (GGR) apresentou as seguintes inciativas:

a. Proposta da estrutura organizacional e metodológica:

Esta assenta nos seguintes vectores: (i) Identificação dos principais riscos. Neste sentido o GGR produziu questionários de auto-avaliação; (ii) Identi- ficação de “patamares” de riscos, consubstanciados em indicadores; (iii) Desenvolvimento de métodos de “medição” e “captura” de eventos; (iv) Produção de relatórios.

b. Elaboração da documentação que consubstancia a infra-estrutura indicada no ponto anterior.

Apresentou os seguintes documentos normativos: × Manual de Gestão do Risco;

× Políticas de Gestão do Risco do BANC;

× Metodologias de Avaliação de Riscos e Controlos (MARC);

× Modelo de Avaliação das Categorias de Risco;

× Modelo de Avaliação das Categorias de Controlo do Risco;

× Modelo de Avaliação da Solvabilidade e Liquidez;

Foi dada especial atenção ao documento “Modelo de Avaliação da Solvabilidade e Liquidez”, pois é nele que constam os patamares de risco onde se define o “apetite” de risco da instituição. O GGR considera que a implementação cabal deste documento depende da adopção de uma ferramenta informática que dote o Gabinete de meios para medir os eventos de risco.

Foram ainda produzidos os seguintes documentos: × Políticas de Gestão do Risco de Crédito do BANC;

× Gabinete de Gestão de Risco - Missão, Estrutura, Funcionamento e Competências;

× Manual Controlo Interno;

× Regulamento de Crédito do BANC.

A incidência deste conjunto documental na área de Crédito, parte da avaliação que o GGR faz sobre os riscos que potencialmente poderão causar impactos mais gravosos no capital do Banco.

Neste sentido, foi considerado que o novo Regulamento de Crédito é um documento estruturante. A principal alteração que vem introduzir é a adopção de um modelo de atribuição de notação de risco, baseado num modelo com critérios que já incorporam algumas noções da IAS/39, ou seja ponderando negativamente os créditos reestruturados e os sem garantias reais ou existindo sem estarem avaliadas.

www.banc.co.ao024

Foram entregues ao Comité de Gestão do Risco os seguintes Relatórios de Risco, produzidos pelo GGR:

× Relatório de avaliação de risco de crédito;

× Relatório de avaliação de risco de mercados e liquidez;

× Relatório de avaliação de risco operacional função contabilística;

O Comité de Gestão do Risco considerando os constrangimentos para a função resultantes da pressão legislativa que se tem vindo a acentuar, resolveu propôr ao Conselho de Administração a alocação de mais um colaborador à área de Gestão de Risco.

Foi revisto o documento de suporte “Ponto de Situação – Função de Compliance”, apresentado pelo Gabinete de Compliance.

Ficou decidido que os riscos de Compliance e de Reputação, caem sob a alçada do Comité de Gestão do Risco.

Relativamente aos Riscos de Compliance, deve ser dada atenção aos seguintes pontos:

× Conformidade com leis e regulamentos – Pretende determinar as possibilidades de incorrer em perdas devido à (i) não observância das normas que regulam a actividade da instituição, nomeadamente normas prudenciais; (ii) violação de outras leis ou regulamentos.

× Conformidade com códigos de conduta, práticas instituídas ou princípios éticos – Tem o objectivo de determinar as possibilidades de incorrer em perdas devido à violação de códigos de conduta, práticas instituídas ou princípios éticos.

× Responsabilidade perante terceiros – Aborda o risco de incorrer em sanções por prejuízos causados a terceiros, nomeadamente devido a (i) um comportamento negligente ou doloso; (ii) um relacionamento inapropriado com os clientes; (iii) incumprimento de contratos ou outro tipo de compromissos; (iv) incumprimento do dever de segredo.

× Grau de transparência - Determina o risco associado a um menor grau de transparência na actividade da instituição e nomeadamente nas transacções realizadas.

× Envolvimento em operações de branqueamento de capitais - Determina o risco da instituição se ver envolvida em operações de branqueamento de capitais.

× Relativamente ao Risco Reputacional, ficam sob alçada do Comité de Gestão do Risco os seguintes pontos:

BANC — Relatório e Contas, 2016 025

× Percepção do mercado – Pretende-se determinar a possibilidade de se verificar uma percepção negativa da imagem pública da instituição por parte do mercado (contrapartes, clientes, colaboradores, investidores, órgãos de imprensa, público em geral).

Ficou decidido pedir uma avaliação do sistema de Branqueamento de Capitais e Combate ao Financiamento do Terrorismo a ser conduzido por uma entidade externa.

O Gabinete de Gestão de Risco propôs, e tendo em atenção ao disposto no Aviso 7/2016 de 22 de Junho, quais as áreas de risco que deverão merecer maior priorização até ao final do ano e para o ano de 2017. Esta acção, é encarada ela própria, como uma avaliação de risco.

Em função da exposição dos activos e no sentido de os proteger o Comité de Gestão do Risco considera as seguintes áreas como sendo de:

Risco Muito Elevado (Riscos Materiais): × Crédito; × Gestão de Liquidez e Capital (Mercados);

Risco Elevado: × Mercados (Taxa de Juro e Cambial) × Operacional;

Risco em observação: × Compliance; × Estratégia.

O Gabinete de Gestão do Risco apresentou uma explanação sobre as mais recentes “peças legislativas” emanadas pelo BNA, com previsível impacto nos capitais próprios do Banco. Referimos a seguinte:

Aviso 2/2016, de 15 de Junho – Rácio de Solvabilidade Regulamentar. Esta legislação que introduz o ICAAP (Internal Capital Adequacy Assessement Process) no sistema financeiro angolano, vem ponderar os Fundos Próprios Regulamentares ao risco de crédito, de mercados e operacional;

× Instrutivo 18/2016, de 8 de Agosto – Prestação de Informação sobre a composição dos fundos próprios e rácio de solvabilidade;

× Aviso 3/2016, de 6 de Junho – Risco de Crédito;

× Instrutivo 13/2016, de 8 Agosto – Prestação de informação sobre o requisito de fundos próprios regulamentar para risco de crédito e risco de crédito de contraparte;

× Instrutivo 12/2016, de 8 de Agosto – Cálculo e requisito de fundos próprios regulamentar para risco de crédito e risco de crédito de contraparte;

www.banc.co.ao026

× Aviso 4/2016, de 22 de Junho – Risco de Mercados;

× Instrutivo 14/2016, de 8 de Agosto – Cálculo e requisito de fundos próprios regulamentar para risco de mercado e risco de crédito de contraparte na carteira de negociação;

× Instrutivo 15/2016, de 8 de Agosto – Prestação de Informação sobre requisito de fundos próprios para risco de mercado e risco de crédito de contraparte na carteira de negociação;

× Aviso 5/2016, de 22 de Junho – Risco Operacional;

× Instrutivo 16/2016, de 8 de Agosto – Cálculo e requisito de fundos próprios regulamentar para risco operacional;

× Aviso 7/2016, de 22 de Junho – Risco Operacional;

× Aviso 8/2016, de 22 de Junho – Taxa de Juro;

× Aviso 9/2016, de 22 de Junho – Grandes Riscos;

× Instrutivo 19/2016, de 30 de Agosto – Risco de Liquidez;

× Aviso 6/2016, de 22 de Junho – IFRS;

× Instrutivo 5/2016, de 8 de Agosto – Perdas por imparidade da carteira de crédito;

× Instrutivo 11/2016, de 8 de Agosto – Tratamento das perdas na carteira de crédito;

× Instrutivo 6/2016, de 8 de Agosto – Divulgação de instrumentos financeiros;

× Instrutivo 7/2016, de 8 de Agosto – Método da taxa de juro efectiva no reconhecimento de rendimentos e gastos de instrumentos financeiros;

× Instrutivo 8/2016, de 8 de Agosto – Locações;

× Instrutivo 9/2016, de 8 de Agosto – Títulos e Valores Mobiliário;

× Instrutivo 10/2016, de 8 de Agosto – Benefícios de Empregados;

× Instrutivo 20/2016, de 6 de Setembro – Adopção pela primeira vez das normas internacionais de relato financeiro;

É dada uma especial atenção ao tema do Capital e Liquidez, aguardando medidas que venham reforçar os capitais próprios do Banco.

BANC — Relatório e Contas, 2016 027

O Anexo III do Relatório de Controlo Interno e Governação Corporativa tem uma perspectiva dos riscos evidenciados. De assinalar que a análise integral do mencionado relatório foi feita em sede de Comité de Auditoria. Nesse sentido foram observados os principais riscos elencados no anexo III (deficiências de controlo interno).

Plano de Acção sobre os riscos materiais (Risco de Crédito e Risco de Liquidez e Capital).

O Gabinete de Gestão do Risco apresentou a adopção de medidas de mitigação do risco de crédito, essencialmente através da intensificação das acções de recuperação dos créditos com sinais de imparidades. As acções devem ser conduzidas pela Direcção de Crédito em estreita cooperação com as áreas comerciais. O enfoque deve ser dado no reforço de garantias, recolha de informação quantitativa relevante para a análise do risco de crédito, e desenvolvimento de avaliações de garantias reais.

A Direcção de Crédito deverá adoptar o módulo de créditos reestruturados e integrar essa informação na análise de risco.

Deve a mesma Direcção e o Gabinete de Gestão de Risco participar na adopção do aplicativo KIWI, sobre o cálculo de imparidades.

Na sequência da explanação feita sobre as mais recentes “peças legislativas”, com impacto na actividade bancária, o GGR apresentou os relatórios sobre o Rácio de Solvabilidade Regulamentar, ponderado por riscos (Aviso 2/2016) e sobre o Risco de Taxa de Juro (Aviso 8/2016).

Ao Gabinete de Gestão de Risco caberá a tarefa de propôr medidas de mitigação e coordenar a sua implementação, sempre que os resultados dos relatórios apresentem risco de impacto nos capitais próprios.

www.banc.co.ao028

5.ÁREAS DE

NEGÓCIO

029BANC — Relatório e Contas, 2016

5.1 CARTEIRA DE CLIENTES

Em termos estratégicos o Banco tem mantido uma política comercial que assenta entre outros pontos no crescimento sustentado do número de clientes e da carteira de depósitos em termos de volume. Outro aspecto que importa realçar é o trabalho de fomento da literacia financeira dos nossos clientes. Esse trabalho desenvolve-se no dia-a-dia no relacionamento pessoal com os nossos gestores comerciais e toda a linha de atendimento. Consideramos que a captação de negócio só faz sentido quando os produtos e serviços realmente servem os clientes e lhes trazem vantagens económicas e sociais, nomeadamente a cultura de poupança. Outra aposta do Banco tem sido a contínua segmentação da sua base de clientes.

O Banco dá especial ênfase a um trabalho comercial integrado e conexo que junta as áreas comerciais, o marketing, organização e processos, procurando encontrar soluções financeiras desenhadas à medida das necessidades dos clientes. Realçamos o depósito Super Oportunidade BANC, bem como um conjunto de taxas promocionais de final de ano agregados a outros produtos de poupança.

Desta acção de busca de sinergias internas direccionadas para a satisfação dos clientes resultou um crescimento de 25,4% do número de clientes, o que representa 6.867 novos clientes, dos quais 6.531 são particulares e 336 Empresas, atingindo um total de 33.929 clientes no final de 2016.

Esta carteira de clientes está distribuída geograficamente por 6 províncias de Angola e 2 escritórios de representação, um em Portugal e outro no Brasil.

5.2 CARTEIRA DE DEPÓSITOS (PARTICULARES E EMPRESAS)A carteira de depósitos cresceu 11% relativamente a 2015 fruto de uma conjuntura pouco favorável à constituição de poupança pelas famílias ou de reservas de tesouraria das empresas. Também uma maior contracção do negócio cambial explica uma menor pujança da captação de novos recursos. Este facto obrigou a uma alteração do paradigma do negócio bancário que imperou até ao início da crise do petróleo, que assentava em grande parte na componente de operações cambiais em detrimento da captação de poupanças e reservas para investimento na economia.

5.3 CRÉDITO A CLIENTES

A carteira de crédito a clientes ressentiu-se sobremaneira do arrefecimento da economia, tendo regredido 11% relativamente a 2015. Também uma regulamentação prudencial mais rigorosa obrigou o Banco à adopção de uma política de gestão mais restritiva. Deste modo, o foco do Banco centrou-se na actividade de restruturação e recuperação. Esta nova realidade trouxe enormes desafios à actividade bancária, tendo em consequência disso um

www.banc.co.ao030

efeito positivo na consolidação dos proveitos de crédito. Por outro lado, e não menos importante, consideramos que uma política mais conservadora relativamente a estes activos propiciará no médio prazo vantagens económicas por via da menor afectação de recursos próprios a provisões para crédito de cobrança duvidosa e reconhecimento de imparidades.

Um dos exemplos que ilustra bem o que atrás se referiu é o caso do programa governamental Angola Investe, que no nosso Banco, em 2016, teve muito pouca expressão, pese embora a garantia do Estado que lhe está associada. Este facto é explicado não só pela conjuntura adversa, mas também pela fraca qualidade dos projectos apresentados.

A carteira total de créditos a clientes em 2016 ascendeu a AKZ 11.708 milhões, o que representou uma contracção de 12% relativamente a 2015.

O Banco continua focado na dinamização da sua área comercial como ponto central da sua estratégia de crescimento, tanto do lado da captação de recursos como na gestão do crédito. Este deve obedecer a pressupostos de análise de risco económicos e sustentáveis. Para este fim a nossa instituição continua a investir nos seus colaboradores comerciais no sentido de os apetrechar com as melhores competências profissionais. Neste âmbito destacamos os programas de formação de gestores bem como o de técnicos de vendas.

BANC — Relatório e Contas, 2016 031

6.IMOBILIZADO

Desde o arranque da actividade do Banco Angolano de Negócios e Comércio em 2007, o maior crescimento da sua rede de balcões continua a ser o registado no ano de 2009 com a abertura de 5 agências. Desde então esse número tem crescido prudentemente em função da estratégia adoptada pela instituição. Em 2016 registamos a inauguração do edifício sede, que inclui uma nova agência nas suas instalações e o encerramento de uma dependência no Porto do Lobito.

Actualmente a acção principal incide na manutenção e melhoria das agências existentes, não descurando novas oportunidades e a implementação do plano de abertura de novos postos comerciais, tão logo seja economicamente viável, numa perspectiva de custo-benefício.

Neste plano, destacamos a inauguração das agências de Lubango II e Morro Bento.

BANC — Relatório e Contas, 2016 033

7.SECTOR DE MEIOS

Devido à crescente concorrência que se verificou em 2016 no sistema financeiro, o BANC trabalhou de modo a reter e fidelizar os seus clientes, oferecendo-lhes produtos e serviços de qualidade. Para este resultado foi determinante a actividade do Marketing, uma vez que a sua principal função foi promover a marca BANC como uma instituição bancária de referência a nível nacional. Desta forma foi possível não só satisfazer os clientes como também enquanto instituição, manter o dinamismo e a proactividade.

Destacamos ainda os serviços oferecidos pela internet banking, como também o atendimento personalizado que continua a ser uma marca distintiva do Banco. Continuamos ainda a dinamizar a marca BANC através de publicações feitas em jornais e revistas nacionais e internacionais. Incluímos no nosso portfólio de meios de comunicação novos canais como a Revista Exame, Sapo (Publicações online), Ledbox (sala de desembarque do aeroporto internacional), Big Midia e Continental (aluguer de espaços – outdoors).

7.1 PRINCIPAIS TAREFAS REALIZADAS EM 2016

Dentro dos objectivos de Marketing propostos para o corrente ano, foram realizadas as seguintes tarefas:

1. Renovação do contrato com a empresa Espaços para publicidade;

2. Renovação da assinatura com a revista Exame;

3. Manutenção das campanhas de comunicação do BANC nas cidades de Luanda e Soyo;

4. Inserção de campanhas no Jornal de Angola e jornal “O País”;

5. Assinatura do contrato com a Empresa Sapo jornal de Angola Online;

6. Desenvolvimento conceptual da campanha inaugural da Sede BANC;

7. Assinatura com as empresas Big Midia e Continental.

7.2 PLANO DE MARKETING PARA 2017

Para o ano de 2017 O MKT propõe a criação de mecanismos que continuem a fomentar relações duradouras com os seus actuais e futuros clientes, oferecendo-lhes produtos e serviços segmentados de qualidade e cada vez mais diferenciadores. Para que esta diferenciação seja possível, devemos apostar cada vez mais num atendimento personalizado baseado na estratégia de vendas cruzadas (cross selling).

No plano da comunicação, dada a actual situação financeira que o país tem atravessado, tencionamos dar seguimento à estratégia BTL- Below the Line

BANC — Relatório e Contas, 2016 035

(divulgação dos nossos produtos e serviços através de feiras, patrocínios, internet, sms, mobile). Embora este tipo de acção também contribua para a notoriedade da marca, o seu objectivo prende-se acima de tudo com a oferta de algum tipo de incentivo, para que se obtenha um acréscimo imediato das vendas (ex.: abertura de conta + aplicação a prazo = possibilidade de transferências internacionais para novos clientes). Neste contexto procederemos ao longo do ano com a divulgação dos nossos produtos de poupanças em jornais e sobretudo canais digitais. Pretendemos igualmente criar e divulgar produtos de depósitos a prazos para captação de recursos ao longo do ano.

www.banc.co.ao036

8.OPERAÇÕES

NACIONAIS E SOBRE O

ESTRANGEIRO

037BANC — Relatório e Contas, 2016

O sector bancário angolano vive um cenário de redução no volume de transacções, pela diminuição na quantidade das importações e pelo decréscimo das divisas colocadas nos leilões do Banco Central. Neste contexto, o BANC realizou em 2016 um total de 6.940 operações nacionais e estrangeiras.

8.1 OPERAÇÕES NACIONAIS

As operações realizadas em moeda nacional destacaram-se quer pela sua frequência, quer pelo valor e volume de operações, não obstante o contexto de menor disponibilidade financeira e de desvalorização da moeda nacional. Todavia, o Banco BANC, movimentou um total de 2.150 cheques no montante de AKZ 4.575 milhões. De igual modo os serviços de transferência a crédito (STC) realizaram 335 operações no valor total de AKZ 1.765 milhões, subdivididas em transferências recebidas no montante de AKZ 2.006 milhões, por contrapartida de AKZ 3.771 milhões de transferências efectuadas.

O Sistema de Pagamentos em Tempo Real, observou entradas de valores no montante total de AKZ 9.998 milhões, contra saídas no valor total de AKZ 7.979 milhões, que resultaram num saldo credor de AKZ 2.018 milhões.

8.2 OPERAÇÕES SOBRE O ESTRANGEIRO

Em relação às operações sobre estrangeiro, o Banco BANC recebeu operações em moeda externa que totalizaram USD 104 mil, espelhando um decréscimo de 26%. As operações emitidas em dólares espelharam uma diminuição de 60%, atingindo 1.720 ordens.

Relativamente às operações emitidas em euros perfizeram 2.100 operações, verificando-se um incremento de 70%, relativamente a igual período do ano anterior.

8.3 OPERAÇÕES CAMBIAIS

O Banco BANC registou um total de 3.820 vendas de divisas num total equivalente a USD 45.1 milhões.

8.4 OPERAÇÕES MONEYGRAM, ATM E TPA

Em 2016 as operações enviadas de Moneygram totalizaram AKZ 91,7 milhões num total de 1.977 operações.

Durante o mesmo período foram instalados 3 ATM´s, totalizando 53 montados.

O total de TPA’s no final de 2016 foi de 926, sendo que durante o ano, foram colocados 156 novos dispositivos de pagamento.

www.banc.co.ao038

9.RECURSOS HUMANOS

039BANC — Relatório e Contas, 2016

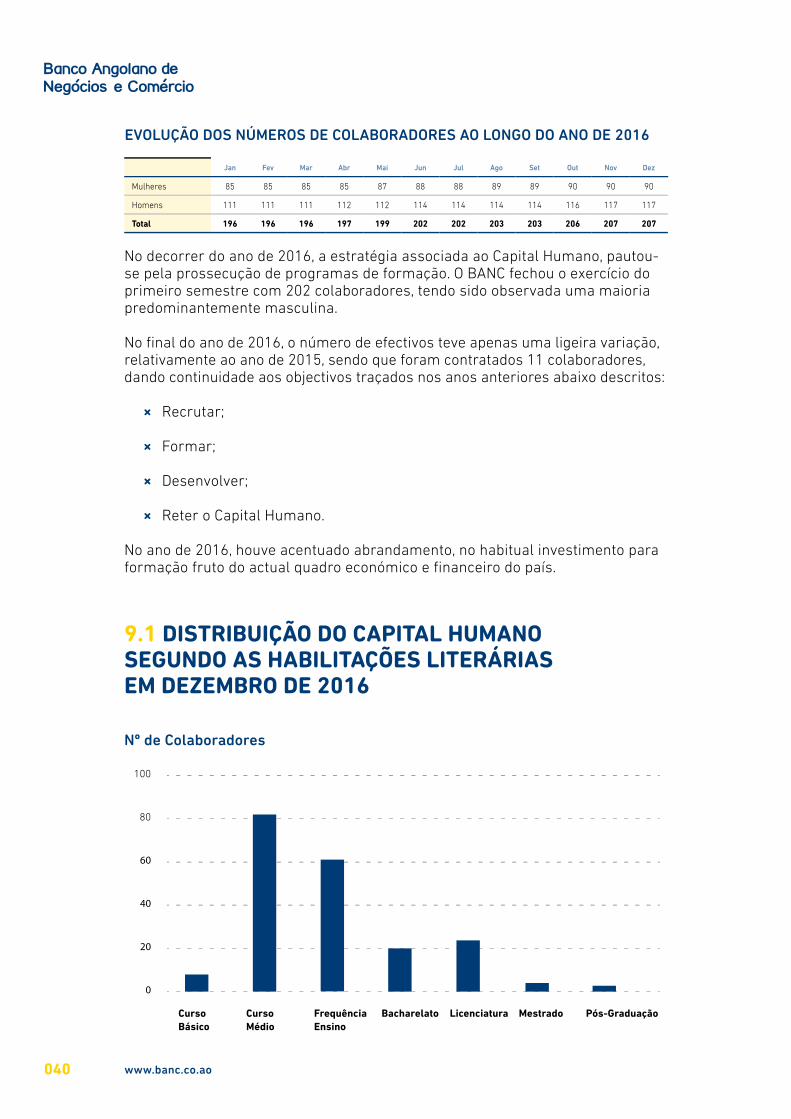

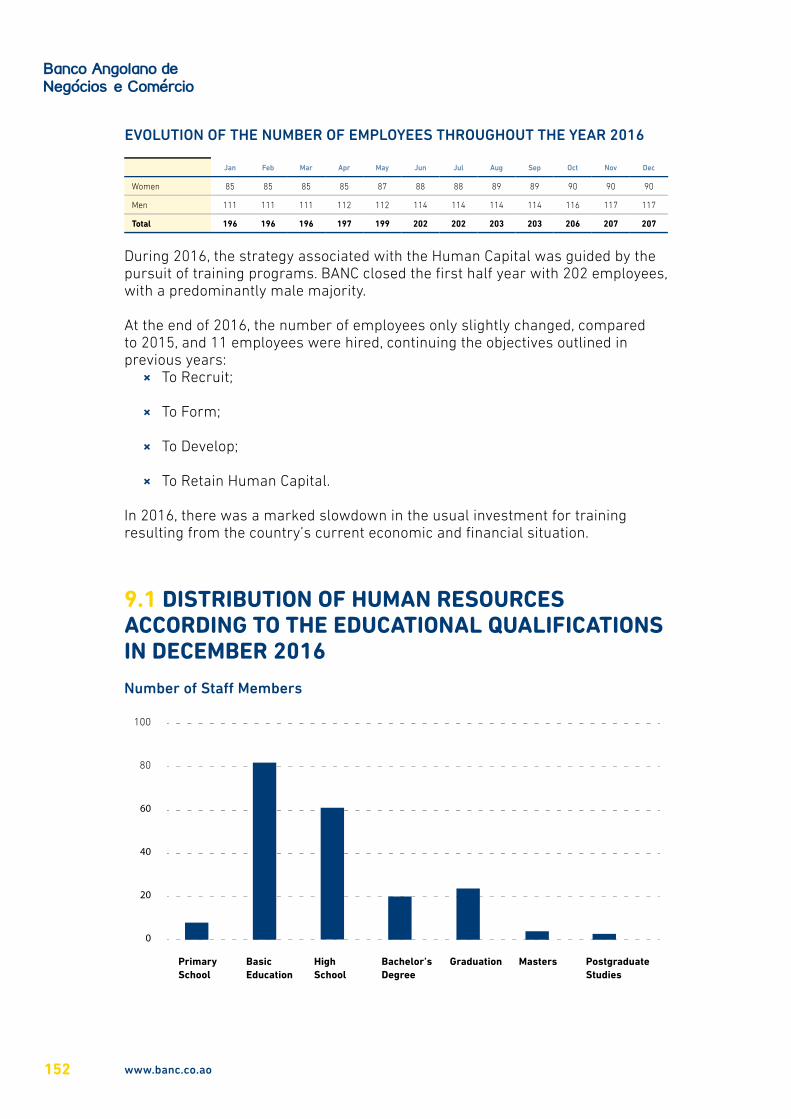

EVOLUÇÃO DOS NÚMEROS DE COLABORADORES AO LONGO DO ANO DE 2016

Jan Fev Mar Abr Mai Jun Jul Ago Set Out Nov Dez

Mulheres 85 85 85 85 87 88 88 89 89 90 90 90

Homens 111 111 111 112 112 114 114 114 114 116 117 117

Total 196 196 196 197 199 202 202 203 203 206 207 207

No decorrer do ano de 2016, a estratégia associada ao Capital Humano, pautou-se pela prossecução de programas de formação. O BANC fechou o exercício do primeiro semestre com 202 colaboradores, tendo sido observada uma maioria predominantemente masculina.

No final do ano de 2016, o número de efectivos teve apenas uma ligeira variação, relativamente ao ano de 2015, sendo que foram contratados 11 colaboradores, dando continuidade aos objectivos traçados nos anos anteriores abaixo descritos:

× Recrutar;

× Formar;

× Desenvolver;

× Reter o Capital Humano.

No ano de 2016, houve acentuado abrandamento, no habitual investimento para formação fruto do actual quadro económico e financeiro do país.

9.1 DISTRIBUIÇÃO DO CAPITAL HUMANO SEGUNDO AS HABILITAÇÕES LITERÁRIAS EM DEZEMBRO DE 2016

Nº de Colaboradores

100

80

60

40

20

0

Curso Básico

Curso Médio

Frequência Ensino

Bacharelato Licenciatura Mestrado Pós-Graduação

www.banc.co.ao040

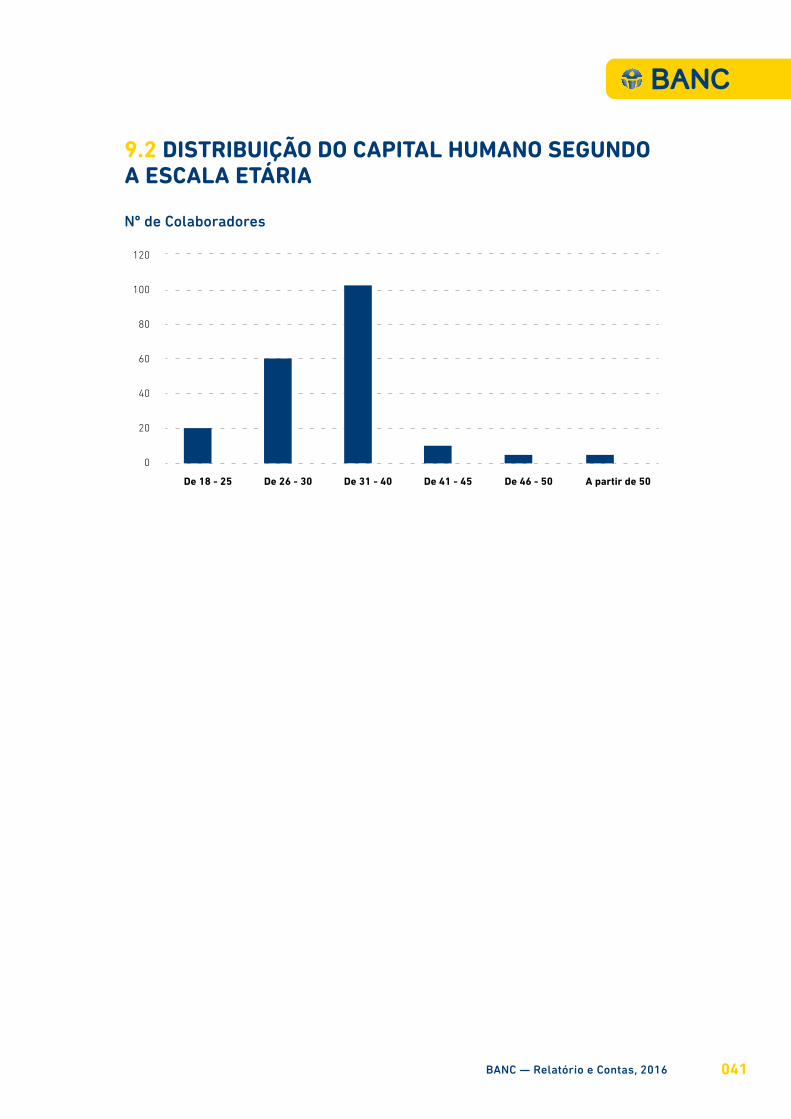

9.2 DISTRIBUIÇÃO DO CAPITAL HUMANO SEGUNDO A ESCALA ETÁRIA

Nº de Colaboradores

120

100

80

60

40

20

0

De 18 - 25 De 26 - 30 De 31 - 40 De 41 - 45 De 46 - 50 A partir de 50

BANC — Relatório e Contas, 2016 041

10. INFORMÁTICA - DESENVOLVIMENTO E SEGURANÇA

10.1 DIRECÇÃO DE DESENVOLVIMENTO E SEGURANÇADurante o ano de 2016 a Direcção de Desenvolvimento e Segurança (DDP) coordenou a implementação dos seguintes projectos e iniciativas:

1. Reestruturação de crédito e Análise de garantias;

2. Projecto Pelicano – MasterCard [Integração BANKA/PEX];

3. Projecto Integração BANKA/SWIFT;

4. Programa de projectos Disaster Recovery × Quick-EDD; × Configuração e arranque da Infraestrutura Blade;

5. Programa de projectos Ondjango – Sede Talatona × SP1 – Datacenter | Plano B - Polo técnico; × SP2 – Neworking; × SP4 – Aprovisionamento.

10.2 DESENVOLVIMENTO

No âmbito de iniciativas regulamentares, foram implementadas por parceiros (EXICTOS), bem como internamente as seguintes:

1. A Framework CEOB, para dar tratamento à cobrança da Contribuição Especial Obrigatória, uma iniciativa do estado angolano, onde os Bancos Comerciais são os principais parceiros;

2. Reformulação da estrutura dos mapas de Necessidades e Operações Executadas em Moeda Estrangeira, iniciativa do BNA para com os Bancos Comerciais;

Iniciativas de necessidade organizacional:

1. Comissão de Manutenção DO, para cobrança de taxa de manutenção/serviço na conta do cliente;

2. Diferenças SAP, iniciativa decorrente do Projecto de Integração BANKA e o SAP com objectivo de terminar com as diferenças existentes no SAP oriundas da integração das interfaces;

3. Suporte Migração, iniciativa para acompanhamento e configurações necessárias à mudança para o novo sítio.

BANC — Relatório e Contas, 2016 043

11.ANÁLISE FINANCEIRA

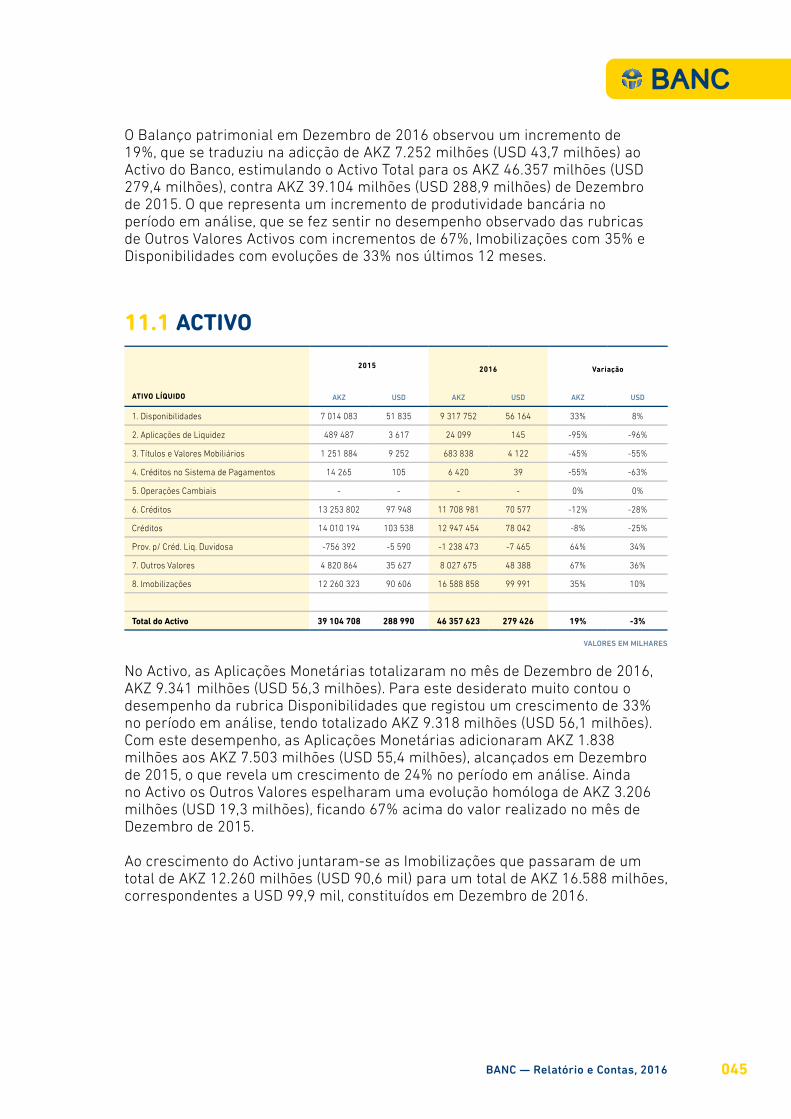

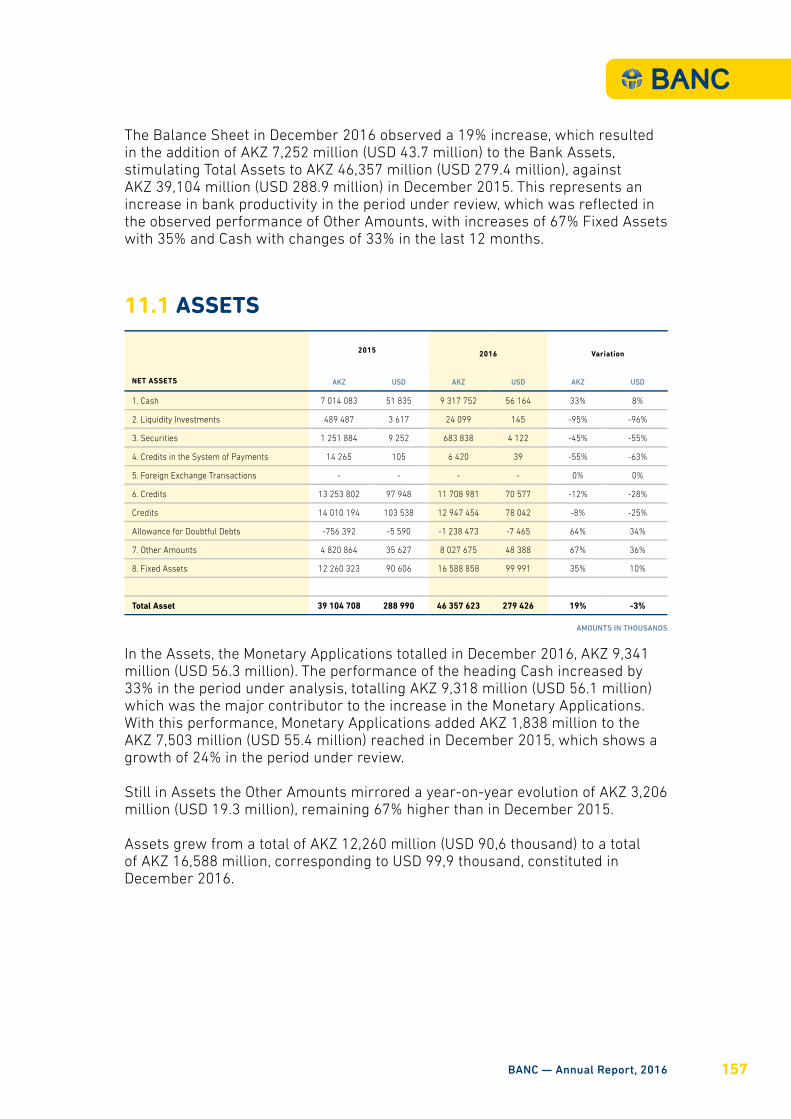

O Balanço patrimonial em Dezembro de 2016 observou um incremento de 19%, que se traduziu na adicção de AKZ 7.252 milhões (USD 43,7 milhões) ao Activo do Banco, estimulando o Activo Total para os AKZ 46.357 milhões (USD 279,4 milhões), contra AKZ 39.104 milhões (USD 288,9 milhões) de Dezembro de 2015. O que representa um incremento de produtividade bancária no período em análise, que se fez sentir no desempenho observado das rubricas de Outros Valores Activos com incrementos de 67%, Imobilizações com 35% e Disponibilidades com evoluções de 33% nos últimos 12 meses.

11.1 ACTIVO

ATIVO LÍQUIDO

2015 2016 Variação

AKZ USD AKZ USD AKZ USD

1. Disponibilidades 7 014 083 51 835 9 317 752 56 164 33% 8%

2. Aplicações de Liquidez 489 487 3 617 24 099 145 -95% -96%

3. Títulos e Valores Mobiliários 1 251 884 9 252 683 838 4 122 -45% -55%

4. Créditos no Sistema de Pagamentos 14 265 105 6 420 39 -55% -63%

5. Operações Cambiais - - - - 0% 0%

6. Créditos 13 253 802 97 948 11 708 981 70 577 -12% -28%

Créditos 14 010 194 103 538 12 947 454 78 042 -8% -25%

Prov. p/ Créd. Liq. Duvidosa -756 392 -5 590 -1 238 473 -7 465 64% 34%

7. Outros Valores 4 820 864 35 627 8 027 675 48 388 67% 36%

8. Imobilizações 12 260 323 90 606 16 588 858 99 991 35% 10%

Total do Activo 39 104 708 288 990 46 357 623 279 426 19% -3%

No Activo, as Aplicações Monetárias totalizaram no mês de Dezembro de 2016, AKZ 9.341 milhões (USD 56,3 milhões). Para este desiderato muito contou o desempenho da rubrica Disponibilidades que registou um crescimento de 33% no período em análise, tendo totalizado AKZ 9.318 milhões (USD 56,1 milhões). Com este desempenho, as Aplicações Monetárias adicionaram AKZ 1.838 milhões aos AKZ 7.503 milhões (USD 55,4 milhões), alcançados em Dezembro de 2015, o que revela um crescimento de 24% no período em análise. Ainda no Activo os Outros Valores espelharam uma evolução homóloga de AKZ 3.206 milhões (USD 19,3 milhões), ficando 67% acima do valor realizado no mês de Dezembro de 2015.

Ao crescimento do Activo juntaram-se as Imobilizações que passaram de um total de AKZ 12.260 milhões (USD 90,6 mil) para um total de AKZ 16.588 milhões, correspondentes a USD 99,9 mil, constituídos em Dezembro de 2016.

VALORES EM MILHARES

BANC — Relatório e Contas, 2016 045

11.1.1 CARTEIRA DE TÍTULOSO total das Aplicações Financeiras, incluindo os activos de títulos emitidos no mercado secundário, sofreu uma redução de 45% em 2016, perfazendo AKZ 683,9 milhões (USD 4,1 milhões), contra AKZ 1.252 milhões (USD 9,3 milhões), do ano anterior.

A Carteira de Títulos do Banco compõe-se de 86% de Bilhetes do Tesouro Nacional, ascendendo a mais de AKZ 585 milhões (USD 3,5 milhões), e de 14% de Obrigações do Tesouro nacional indexadas ao dólar, com maturidade de dois anos. As taxas de remuneração dos Bilhetes do Tesouro cifraram-se entre os 16,7% e os 20,3%. A taxa de remuneração das Obrigações do Tesouro Indexadas ao dólar, cifram-se em 7%. As taxas de Juro dos Títulos do Tesouro nacional revelaram-se mais atractivas em 2016. Todavia estão muito abaixo da taxa de inflação anual, que até ao final de 2016 se fixou em 41,95%, contra 24% da taxa de juro mais elevada, negociada ao longo do ano de 2016.

18 000 000,00

16 000 000,00

14 000 000,00

12 000 000,00

10 000 000,00

8 000 000,00

6 000 000,00

4 000 000,00

2 000 000,00

0,00

Disponibilidades

2015 2016

AplicaçõesMonetárias

Titulos e Valores Monetários

Créditos Outros Valores Imobilizações

30,00%

25,00%

20,00%

15,00%

10,00%

5,00%

0,0091 Dias

2015 2016

182 Dias

BT OT OTNR

365 Dias 2 Anos 3 Anos 4 Anos 5 Anos 2 Anos

Evolução das Taxas de Juro dos Títulos do Tesouro Nacional

www.banc.co.ao046

11.1.2 CRÉDITO A CLIENTESO volume de crédito concedido aos Clientes sofreu uma redução de 12% em 2016, sendo este facto consistente com a quebra de liquidez financeira que afectou os bancos comerciais e as empresas ao longo do ano, resultando na contração do crédito concedido aos Clientes Particulares, que por sua vez registaram uma redução do volume de AKZ 2.758 milhões (USD 16,7 milhões) em 2016, contra AKZ 3.304 milhões (USD 24,2 milhões) em 2015, o que implica uma contração aos particulares de 17%.

No que respeita ao crédito concedido aos Clientes Empresas, observou-se a tendência também para contração, visto não haver da parte das empresas garantias seguras de retorno do crédito recebido, havendo igualmente muito poucos projectos de investimento com a qualidade e contragarantias necessárias. Assim sendo, o crédito concedido às Empresas no mês de Dezembro de 2016 totalizou AKZ 8.950 milhões (USD 53,9 milhões), face a AKZ 9.949 milhões, equivalentes a USD 73,5 milhões. Podemos, portanto, concluir que o crédito aos Clientes Empresa registou no período homólogo de 2015, uma quebra de 10%.

O Crédito em moeda nacional totalizou AKZ 8.650 milhões (USD 52,1 milhões), em Dezembro de 2016, contra AKZ 10.567 milhões (USD 78 milhões), realizados em igual período de 2015, o que revela uma contração de 18%. O Crédito Concedido em moeda estrangeira totalizou, no mês de Dezembro de 2016, AKZ 822,7 milhões (USD 4,9 milhões), contra 719,2 milhões, (USD 5,3 milhões), concedidos em Dezembro de 2015.

O Crédito Vencido em moeda nacional totalizou AKZ 3.294 milhões (USD 19,8 milhões), que representam um agravamento de 36%. O Crédito Vencido em moeda estrangeira perfez AKZ 1,1 milhão (USD 7 mil). A conjugação do crédito vencido em moeda nacional e em moeda estrangeira resultou no Crédito Vencido Total de AKZ 3.294 milhões (USD 19,9 milhões), contra AKZ 2.414 milhões (USD 17,8 milhões), alcançados no período homólogo de 2015 (+36%).

Em função do agravamento do crédito vencido total, as Provisões Totais de Crédito cresceram 64%. O incremento do valor das provisões foi repartido entre Provisões para Crédito de Liquidação Duvidosa e Provisões de Crédito Normal, tendo as primeiras somado AKZ 845,8 milhões, equivalentes a USD 5 milhões e as Provisões para Crédito Normal ascendido a AKZ 392,6 milhões (USD 2,3 milhões).

Carteira de Crédito

2015 2016

47%

53%

BANC — Relatório e Contas, 2016 047

O crédito concedido aos clientes totalizou AKZ 9.473 milhões, equivalentes a USD 57,1 milhões no mês de Dezembro de 2016, o que relativamente ao saldo obtido em igual período de 2015 representou uma quebra de AKZ 1.812 milhões, equivalentes a USD 10,9 milhões, indicando uma contração do crédito concedido aos clientes na ordem de 16%. O total dos proveitos de crédito, quer sejam em moeda nacional, quer sejam em moeda estrangeira, fixaram-se em AKZ 179,2 milhões, equivalentes a USD 1 milhão, espelhando um decréscimo de 42% em relação ao ano anterior.

2015 2016 Variação

AKZ USD AKZ USD Absoluta (%)

1. Crédito Total 13 253 802 97 948 11 708 981 70 577 -1 544 822 -12%

1.1 Crédito sobre Clientes 11 286 345 83 408 9 473 360 57 102 -1 812 985 -16%

Moeda Nacional 10 567 062 78 092 8 650 631 52 143 -1 916 432 -18%

Moeda Estrangeira 719 283 5 316 822 729 4 959 103 447 14%

1.2 Crédito e Juros Vencidos 2 414 505 17 844 3 294 813 19 860 880 308 36%

Moeda Nacional 2 414 470 17 843 3 293 677 19 853 879 207 36%

Moeda Estrangeira 36 - 1 136 7 1 100 3085%

Juros Vencidos a Regularizar -1 - - - 1 -100%

2. Proveitos de Crédito 309 344 2 286 179 281 1 080 -130 063 -42%

Moeda Nacional 306 952 2 268 178 868 1 078 -128 084 -42%

Moeda Estrangeira 2 392 18 413 2 -1 979 -83%

3. Provisões Totais de Crédito -756 392 -5 590 -1 238 473 -7 465 -482 081 64%

3.1 Provisões Liquidação Duvidosa -580 395 -4 289 -845 871 -5 099 -265 477 46%

3.2 Provisões Crédito Normal -175 998 -1 301 -392 602 -2 366 -216 604 123%

4. Rácios

4.1 Crédito/ Depósitos 69% 55% -21%

4.2 Crédito Vencido/ Crédito Total 18% 28% 54%

4.3 Próvisões Crédito/ Crédito Total -6% -11% 85%

VALORES EM MILHARES

Evolução do Crédito por segmento10 000,00

8 000,00

6 000,00

4 000,00

2 000,00

0,00

2015

Empresas

Particulares

2016

Evolução do Crédito a Clientes

www.banc.co.ao048

O rácio Crédito/Depósito, o qual espelha uma redução do peso do crédito total sobre a Carteira de depósitos, passou de 69% em 2015, para de 55% em igual período de 2016.

O rácio Crédito Vencido/Crédito Total fixou-se no mês de Dezembro de 2016, em 28%, contra os 18%, obtidos no período homólogo de 2015, o que espelha um aumento de 54% do crédito em situação irregular no total do crédito concedido.

As Provisões de Crédito sobre o crédito total passaram de 6% em Dezembro de 2015, para 11% sobre o total do crédito no mês de Dezembro de 2016.

11.2 PASSIVO

PASSIVO

2015 2016 Variação

AKZ USD AKZ USD AKZ USD

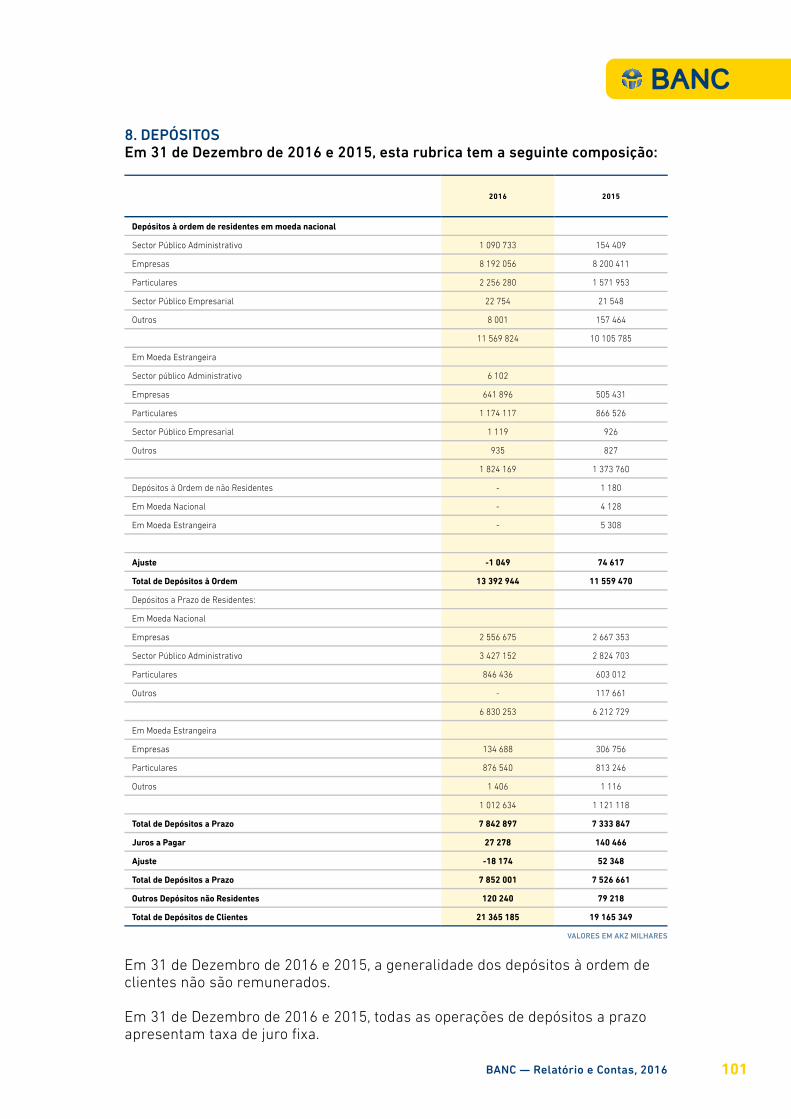

1. Depósitos 19 165 349 141 635 21 365 185 128 781 11% -9%

À Ordem 11 559 470 85 426 13 392 944 80 728 16% -6%

A Prazo 7 526 661 55 623 7 852 001 47 329 4% -15%

Outros Depósitos 79 218 585 120 240 725 52% 24%

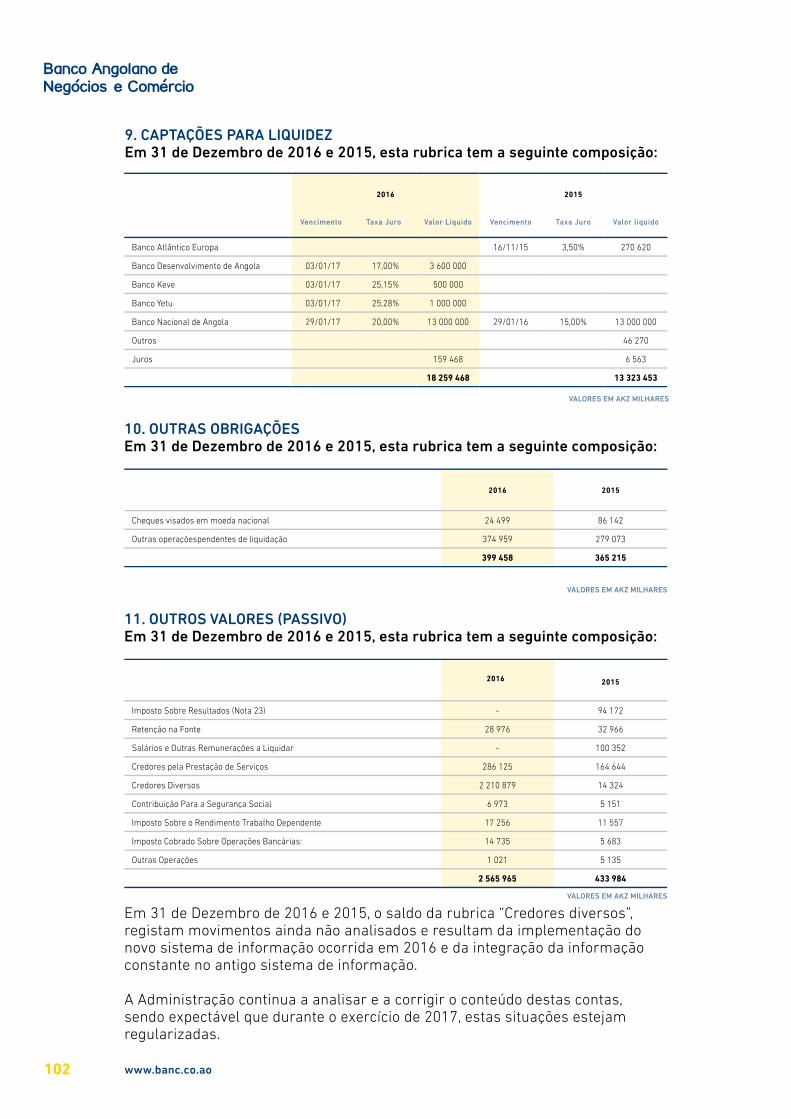

2. Captações para Liquidez 13 323 453 98 463 18 259 468 110 061 37% 12%

3. Obrigações no Sistema de Pagamentos 365 215 2 699 399 458 2 408 9% -11%

4. Operações Cambiais - - - - 0% 0%

5. Outras Obrigações 433 984 3 207 2 565 965 15 467 491% 382%

6. Provisões para Responsabilidades Prováveis

31 250 231 15 867 96 -49% -59%

7. Capital Social 4 345 752 32 116 4 345 752 26 195 0% -18%

8. Reservas e Fundos 1 219 970 9 016 1 219 970 7 354 0% -18%

9. Resultados Potenciais - - - - 0% 0%

10. Resultados Transitados - - -90 373 -545 0% 0%

11. Resultado Operacional 381 345 2 818 -1 751 532 -10 558 -559% -475%

12. Resultado Não Operacional -67 438 -498 27 863 168 -141% -134%

13. Encargos s/Resultado Corrente -94 172 -696 - - -100% -100%

Total do Passivo 39 104 708 288 990 46 357 623 279 426 19% -3%

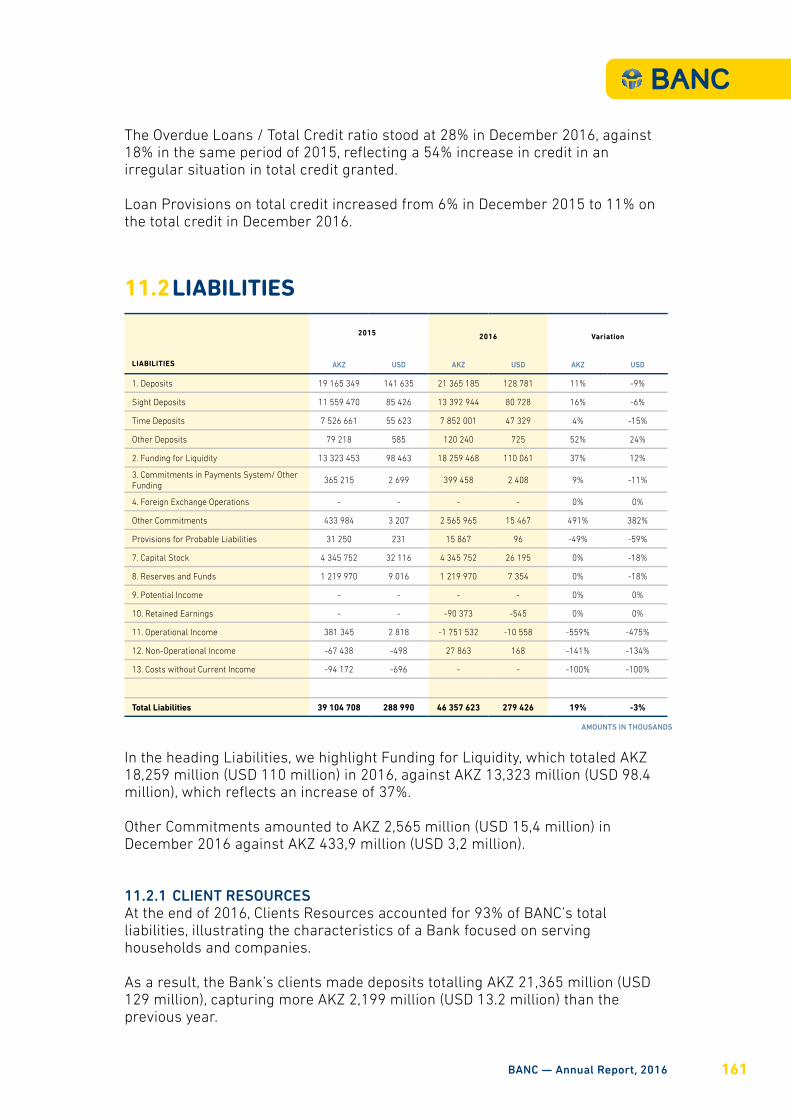

No Passivo destacaram-se as Captações de Liquidez que em 2016 perfizeram AKZ 18.259 milhões (USD 110 milhões), contra AKZ 13.323 milhões (USD 98,4 milhões), realizando uma evolução de 37%.

As Outras Obrigações, totalizaram AKZ 2.565 milhões, (USD 15,4 milhões), obtidos no mês de Dezembro de 2016, contra AKZ 433,9 milhões, (USD 3,2 milhões).

11.2.1 RECURSOS DE CLIENTESOs Recursos de Clientes representavam no final de 2016, 93% do total do passivo do BANC, ilustrando as características de um Banco centrado ao serviço das famílias e das empresas.

VALORES EM MILHARES

BANC — Relatório e Contas, 2016 049

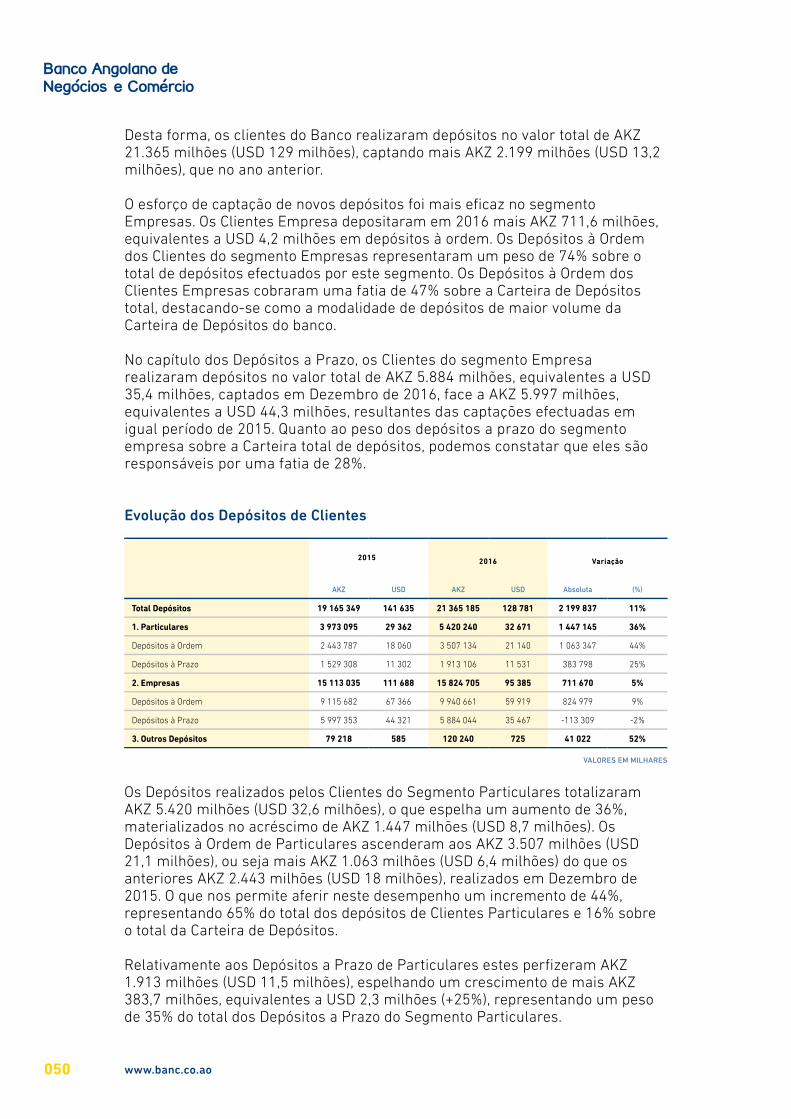

Desta forma, os clientes do Banco realizaram depósitos no valor total de AKZ 21.365 milhões (USD 129 milhões), captando mais AKZ 2.199 milhões (USD 13,2 milhões), que no ano anterior.

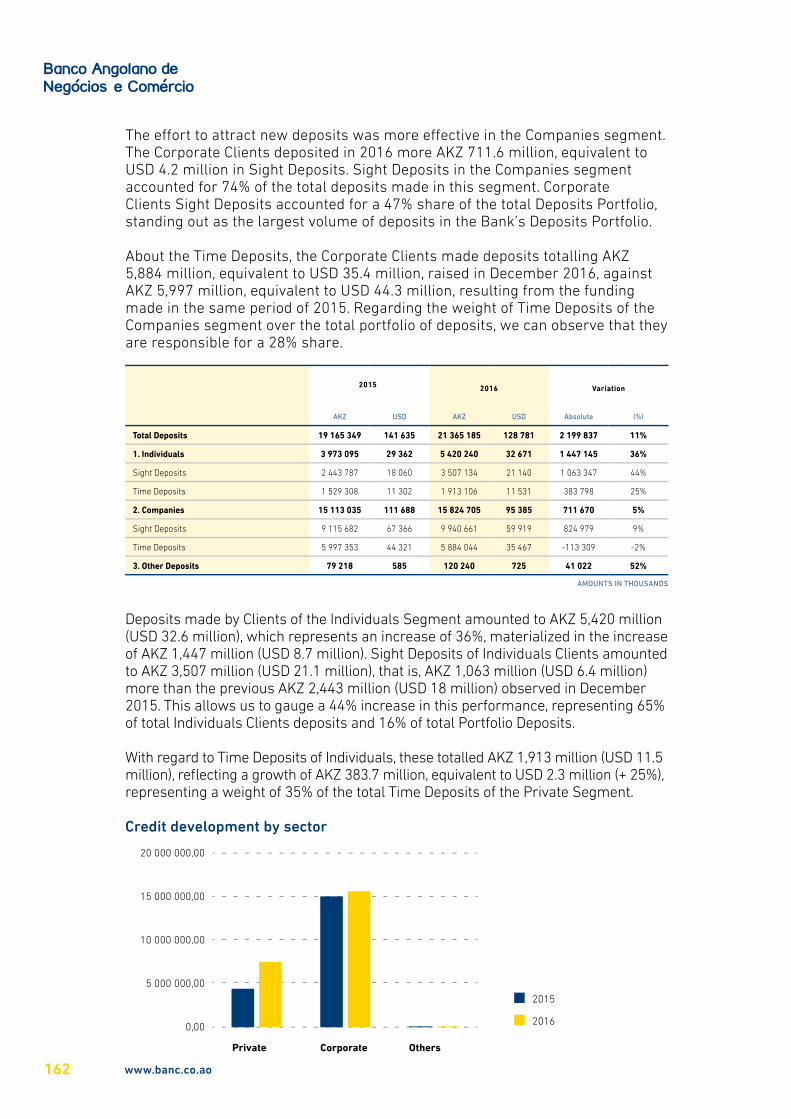

O esforço de captação de novos depósitos foi mais eficaz no segmento Empresas. Os Clientes Empresa depositaram em 2016 mais AKZ 711,6 milhões, equivalentes a USD 4,2 milhões em depósitos à ordem. Os Depósitos à Ordem dos Clientes do segmento Empresas representaram um peso de 74% sobre o total de depósitos efectuados por este segmento. Os Depósitos à Ordem dos Clientes Empresas cobraram uma fatia de 47% sobre a Carteira de Depósitos total, destacando-se como a modalidade de depósitos de maior volume da Carteira de Depósitos do banco.

No capítulo dos Depósitos a Prazo, os Clientes do segmento Empresa realizaram depósitos no valor total de AKZ 5.884 milhões, equivalentes a USD 35,4 milhões, captados em Dezembro de 2016, face a AKZ 5.997 milhões, equivalentes a USD 44,3 milhões, resultantes das captações efectuadas em igual período de 2015. Quanto ao peso dos depósitos a prazo do segmento empresa sobre a Carteira total de depósitos, podemos constatar que eles são responsáveis por uma fatia de 28%.

Evolução dos Depósitos de Clientes

2015 2016 Variação

AKZ USD AKZ USD Absoluta (%)

Total Depósitos 19 165 349 141 635 21 365 185 128 781 2 199 837 11%

1. Particulares 3 973 095 29 362 5 420 240 32 671 1 447 145 36%

Depósitos à Ordem 2 443 787 18 060 3 507 134 21 140 1 063 347 44%

Depósitos à Prazo 1 529 308 11 302 1 913 106 11 531 383 798 25%

2. Empresas 15 113 035 111 688 15 824 705 95 385 711 670 5%

Depósitos à Ordem 9 115 682 67 366 9 940 661 59 919 824 979 9%

Depósitos à Prazo 5 997 353 44 321 5 884 044 35 467 -113 309 -2%

3. Outros Depósitos 79 218 585 120 240 725 41 022 52%

VALORES EM MILHARES

Os Depósitos realizados pelos Clientes do Segmento Particulares totalizaram AKZ 5.420 milhões (USD 32,6 milhões), o que espelha um aumento de 36%, materializados no acréscimo de AKZ 1.447 milhões (USD 8,7 milhões). Os Depósitos à Ordem de Particulares ascenderam aos AKZ 3.507 milhões (USD 21,1 milhões), ou seja mais AKZ 1.063 milhões (USD 6,4 milhões) do que os anteriores AKZ 2.443 milhões (USD 18 milhões), realizados em Dezembro de 2015. O que nos permite aferir neste desempenho um incremento de 44%, representando 65% do total dos depósitos de Clientes Particulares e 16% sobre o total da Carteira de Depósitos.

Relativamente aos Depósitos a Prazo de Particulares estes perfizeram AKZ 1.913 milhões (USD 11,5 milhões), espelhando um crescimento de mais AKZ 383,7 milhões, equivalentes a USD 2,3 milhões (+25%), representando um peso de 35% do total dos Depósitos a Prazo do Segmento Particulares.

www.banc.co.ao050

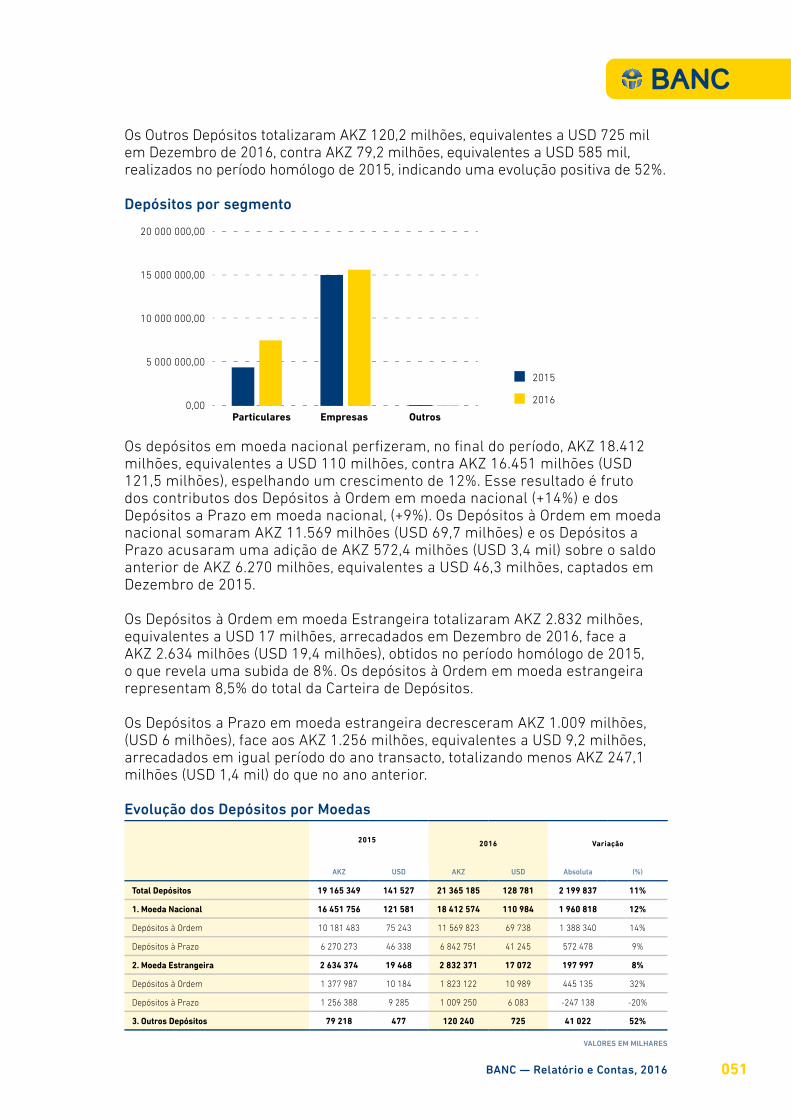

Os Outros Depósitos totalizaram AKZ 120,2 milhões, equivalentes a USD 725 mil em Dezembro de 2016, contra AKZ 79,2 milhões, equivalentes a USD 585 mil, realizados no período homólogo de 2015, indicando uma evolução positiva de 52%.

2015 2016 Variação

AKZ USD AKZ USD Absoluta (%)

Total Depósitos 19 165 349 141 527 21 365 185 128 781 2 199 837 11%

1. Moeda Nacional 16 451 756 121 581 18 412 574 110 984 1 960 818 12%

Depósitos à Ordem 10 181 483 75 243 11 569 823 69 738 1 388 340 14%

Depósitos à Prazo 6 270 273 46 338 6 842 751 41 245 572 478 9%

2. Moeda Estrangeira 2 634 374 19 468 2 832 371 17 072 197 997 8%

Depósitos à Ordem 1 377 987 10 184 1 823 122 10 989 445 135 32%

Depósitos à Prazo 1 256 388 9 285 1 009 250 6 083 -247 138 -20%

3. Outros Depósitos 79 218 477 120 240 725 41 022 52%

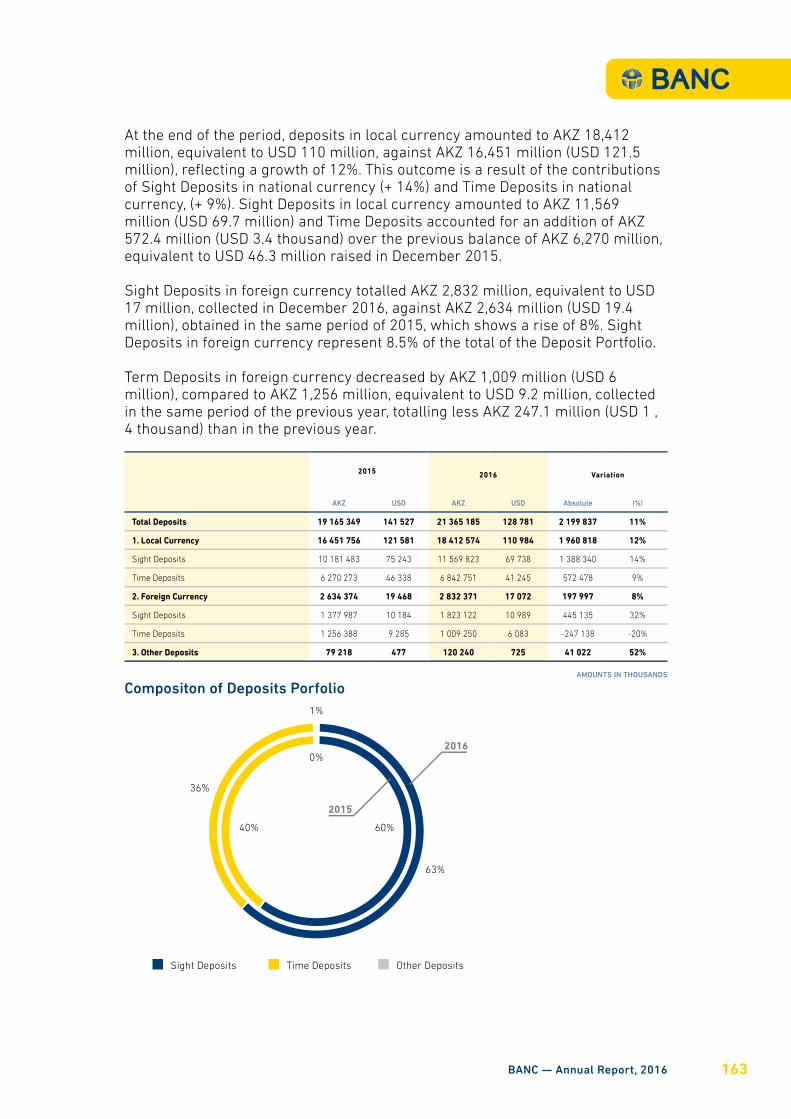

Os depósitos em moeda nacional perfizeram, no final do período, AKZ 18.412 milhões, equivalentes a USD 110 milhões, contra AKZ 16.451 milhões (USD 121,5 milhões), espelhando um crescimento de 12%. Esse resultado é fruto dos contributos dos Depósitos à Ordem em moeda nacional (+14%) e dos Depósitos a Prazo em moeda nacional, (+9%). Os Depósitos à Ordem em moeda nacional somaram AKZ 11.569 milhões (USD 69,7 milhões) e os Depósitos a Prazo acusaram uma adição de AKZ 572,4 milhões (USD 3,4 mil) sobre o saldo anterior de AKZ 6.270 milhões, equivalentes a USD 46,3 milhões, captados em Dezembro de 2015.

Os Depósitos à Ordem em moeda Estrangeira totalizaram AKZ 2.832 milhões, equivalentes a USD 17 milhões, arrecadados em Dezembro de 2016, face a AKZ 2.634 milhões (USD 19,4 milhões), obtidos no período homólogo de 2015, o que revela uma subida de 8%. Os depósitos à Ordem em moeda estrangeira representam 8,5% do total da Carteira de Depósitos.

Os Depósitos a Prazo em moeda estrangeira decresceram AKZ 1.009 milhões, (USD 6 milhões), face aos AKZ 1.256 milhões, equivalentes a USD 9,2 milhões, arrecadados em igual período do ano transacto, totalizando menos AKZ 247,1 milhões (USD 1,4 mil) do que no ano anterior.

Evolução dos Depósitos por Moedas

VALORES EM MILHARES

Depósitos por segmento25 000 000,00

20 000 000,00

15 000 000,00

10 000 000,00

5 000 000,00

0,00Particulares Empresas Outros

2015

2016

BANC — Relatório e Contas, 2016 051

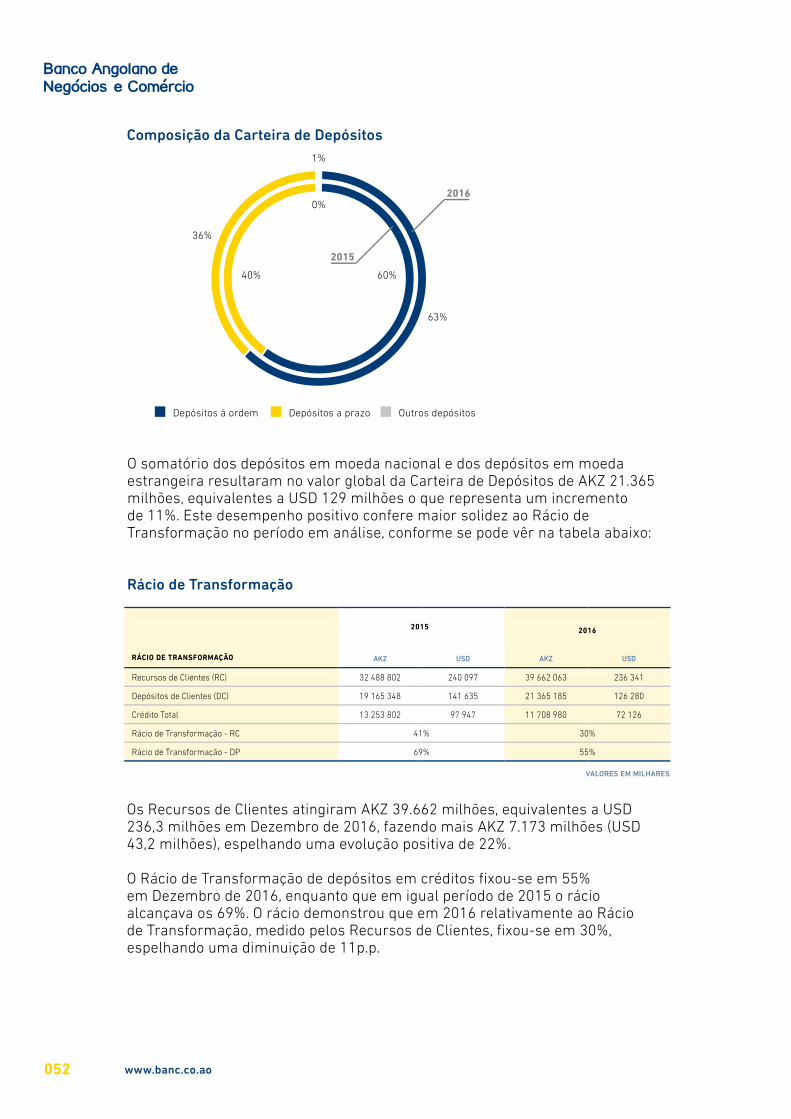

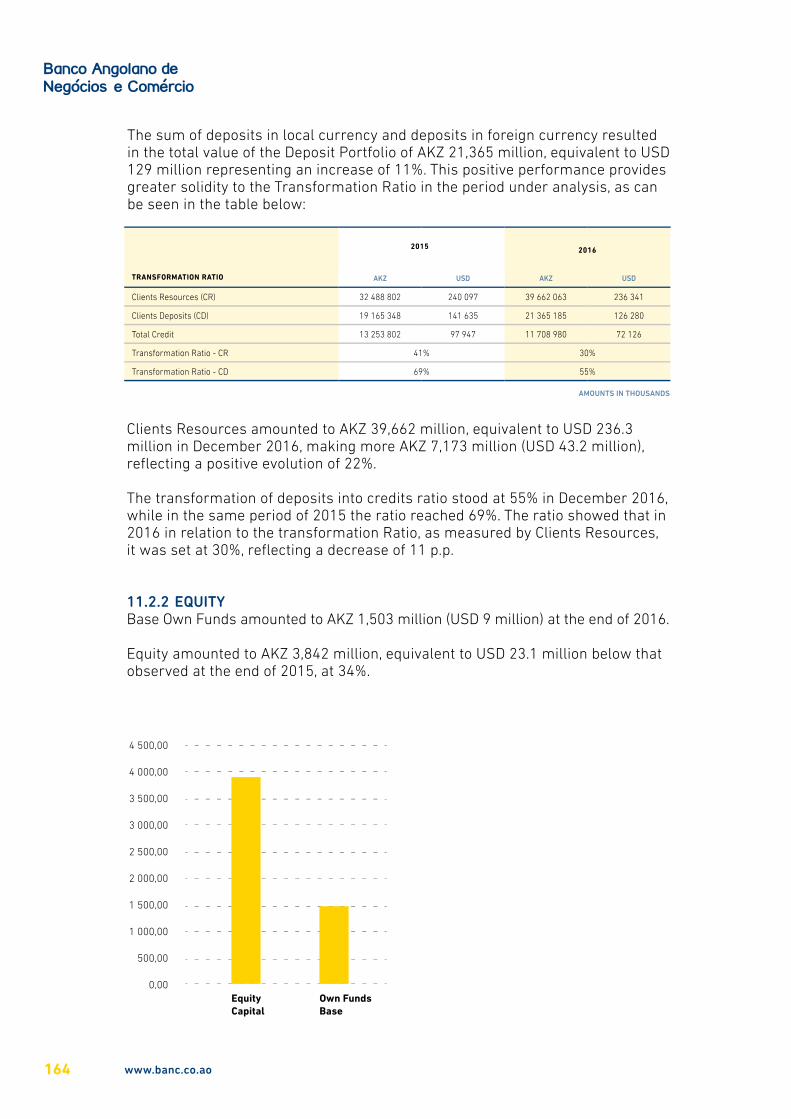

O somatório dos depósitos em moeda nacional e dos depósitos em moeda estrangeira resultaram no valor global da Carteira de Depósitos de AKZ 21.365 milhões, equivalentes a USD 129 milhões o que representa um incremento de 11%. Este desempenho positivo confere maior solidez ao Rácio de Transformação no período em análise, conforme se pode vêr na tabela abaixo:

Rácio de Transformação

RÁCIO DE TRANSFORMAÇÃO

2015 2016

AKZ USD AKZ USD

Recursos de Clientes (RC) 32 488 802 240 097 39 662 063 236 341

Depósitos de Clientes (DC) 19 165 348 141 635 21 365 185 126 280

Crédito Total 13 253 802 97 947 11 708 980 72 126

Rácio de Transformação - RC 41% 30%

Rácio de Transformação - DP 69% 55%

Os Recursos de Clientes atingiram AKZ 39.662 milhões, equivalentes a USD 236,3 milhões em Dezembro de 2016, fazendo mais AKZ 7.173 milhões (USD 43,2 milhões), espelhando uma evolução positiva de 22%.

O Rácio de Transformação de depósitos em créditos fixou-se em 55% em Dezembro de 2016, enquanto que em igual período de 2015 o rácio alcançava os 69%. O rácio demonstrou que em 2016 relativamente ao Rácio de Transformação, medido pelos Recursos de Clientes, fixou-se em 30%, espelhando uma diminuição de 11p.p.

VALORES EM MILHARES

Composição da Carteira de Depósitos

Depósitos à ordem Depósitos a prazo Outros depósitos

0%

1%

36%

63%

40% 60%

www.banc.co.ao052

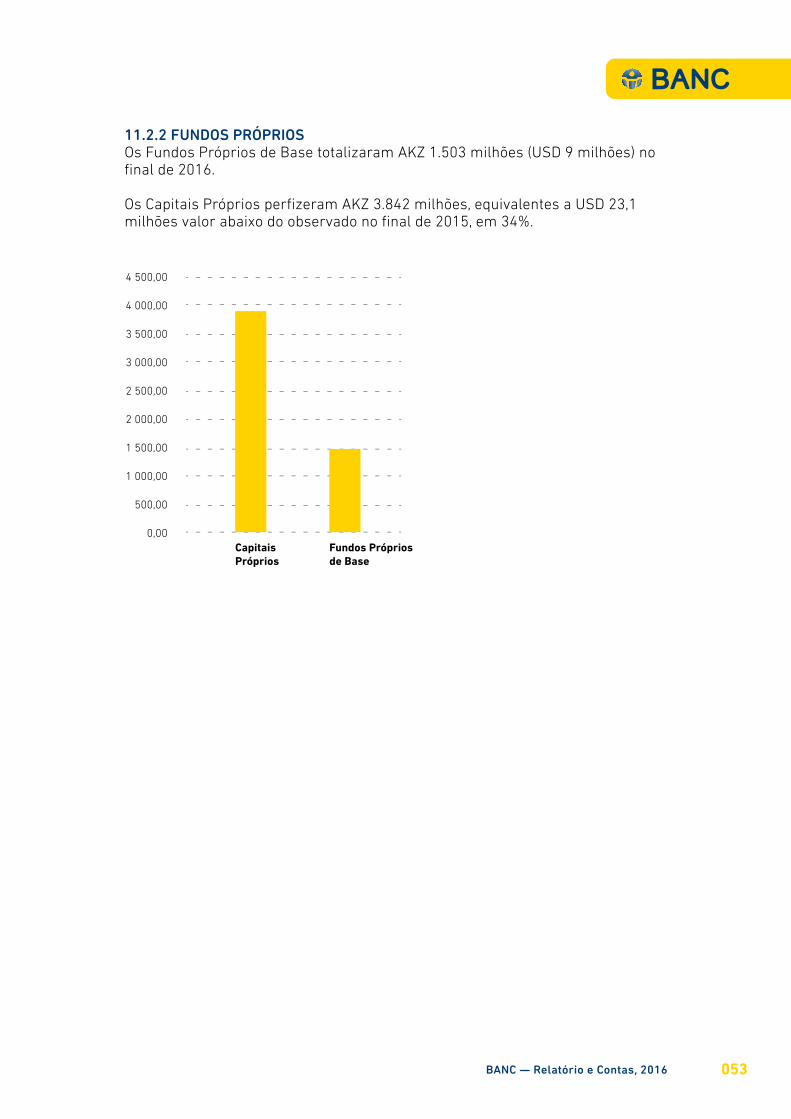

11.2.2 FUNDOS PRÓPRIOSOs Fundos Próprios de Base totalizaram AKZ 1.503 milhões (USD 9 milhões) no final de 2016.

Os Capitais Próprios perfizeram AKZ 3.842 milhões, equivalentes a USD 23,1 milhões valor abaixo do observado no final de 2015, em 34%.

Capitais Próprios

Fundos Próprios de Base

BANC — Relatório e Contas, 2016 053

12.ANÁLISE ECONÓMICA

12.1 RENTABILIDADE

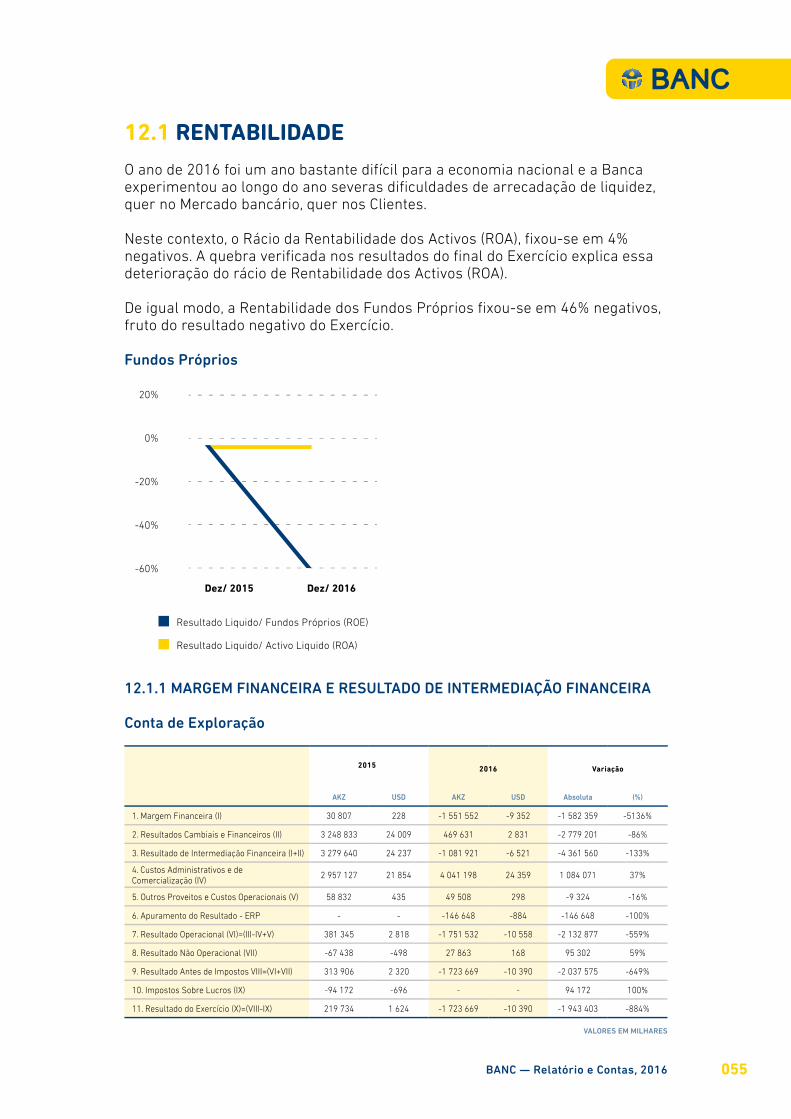

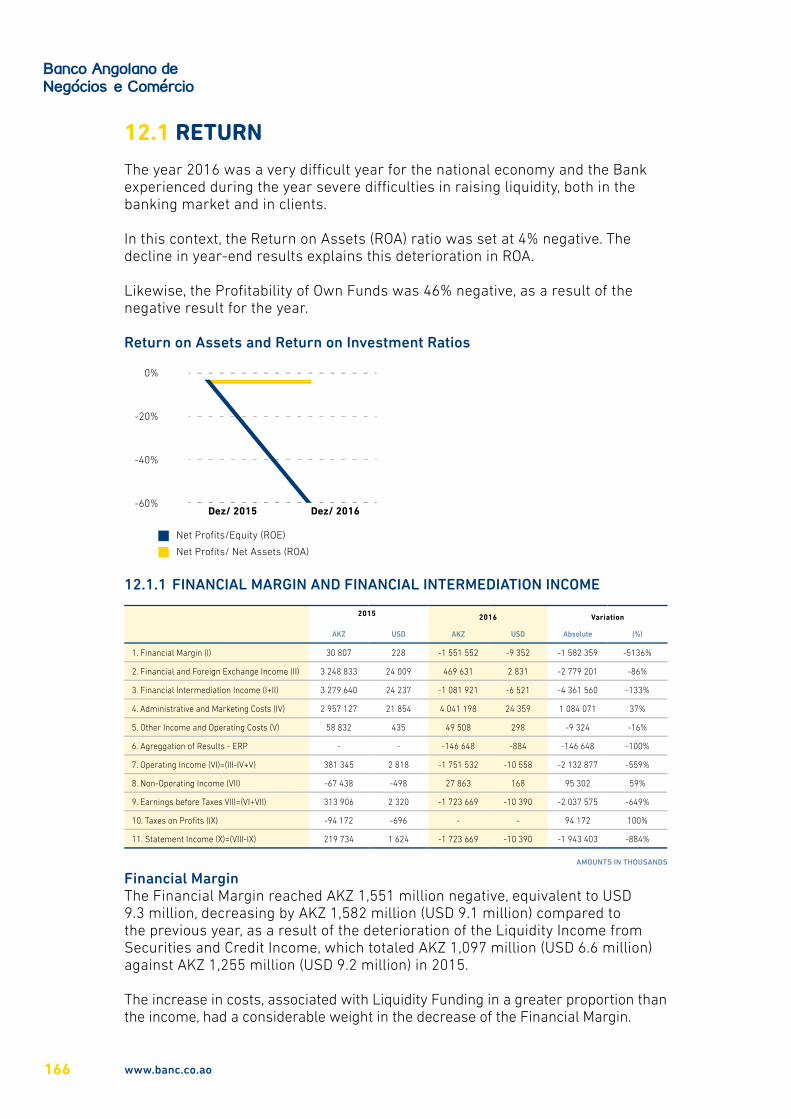

O ano de 2016 foi um ano bastante difícil para a economia nacional e a Banca experimentou ao longo do ano severas dificuldades de arrecadação de liquidez, quer no Mercado bancário, quer nos Clientes.

Neste contexto, o Rácio da Rentabilidade dos Activos (ROA), fixou-se em 4% negativos. A quebra verificada nos resultados do final do Exercício explica essa deterioração do rácio de Rentabilidade dos Activos (ROA).

De igual modo, a Rentabilidade dos Fundos Próprios fixou-se em 46% negativos, fruto do resultado negativo do Exercício.

12.1.1 MARGEM FINANCEIRA E RESULTADO DE INTERMEDIAÇÃO FINANCEIRA

Conta de Exploração

2015 2016 Variação

AKZ USD AKZ USD Absoluta (%)

1. Margem Financeira (I) 30 807 228 -1 551 552 -9 352 -1 582 359 -5136%

2. Resultados Cambiais e Financeiros (II) 3 248 833 24 009 469 631 2 831 -2 779 201 -86%

3. Resultado de Intermediação Financeira (I+II) 3 279 640 24 237 -1 081 921 -6 521 -4 361 560 -133%

4. Custos Administrativos e de Comercialização (IV)

2 957 127 21 854 4 041 198 24 359 1 084 071 37%

5. Outros Proveitos e Custos Operacionais (V) 58 832 435 49 508 298 -9 324 -16%

6. Apuramento do Resultado - ERP - - -146 648 -884 -146 648 -100%

7. Resultado Operacional (VI)=(III-IV+V) 381 345 2 818 -1 751 532 -10 558 -2 132 877 -559%

8. Resultado Não Operacional (VII) -67 438 -498 27 863 168 95 302 59%

9. Resultado Antes de Impostos VIII=(VI+VII) 313 906 2 320 -1 723 669 -10 390 -2 037 575 -649%

10. Impostos Sobre Lucros (IX) -94 172 -696 - - 94 172 100%

11. Resultado do Exercício (X)=(VIII-IX) 219 734 1 624 -1 723 669 -10 390 -1 943 403 -884%

VALORES EM MILHARES

Fundos Próprios

20%

0%

-20%

-40%

-60%

Dez/ 2015

Resultado Liquido/ Fundos Próprios (ROE)

Resultado Liquido/ Activo Liquido (ROA)

Dez/ 2016

BANC — Relatório e Contas, 2016 055

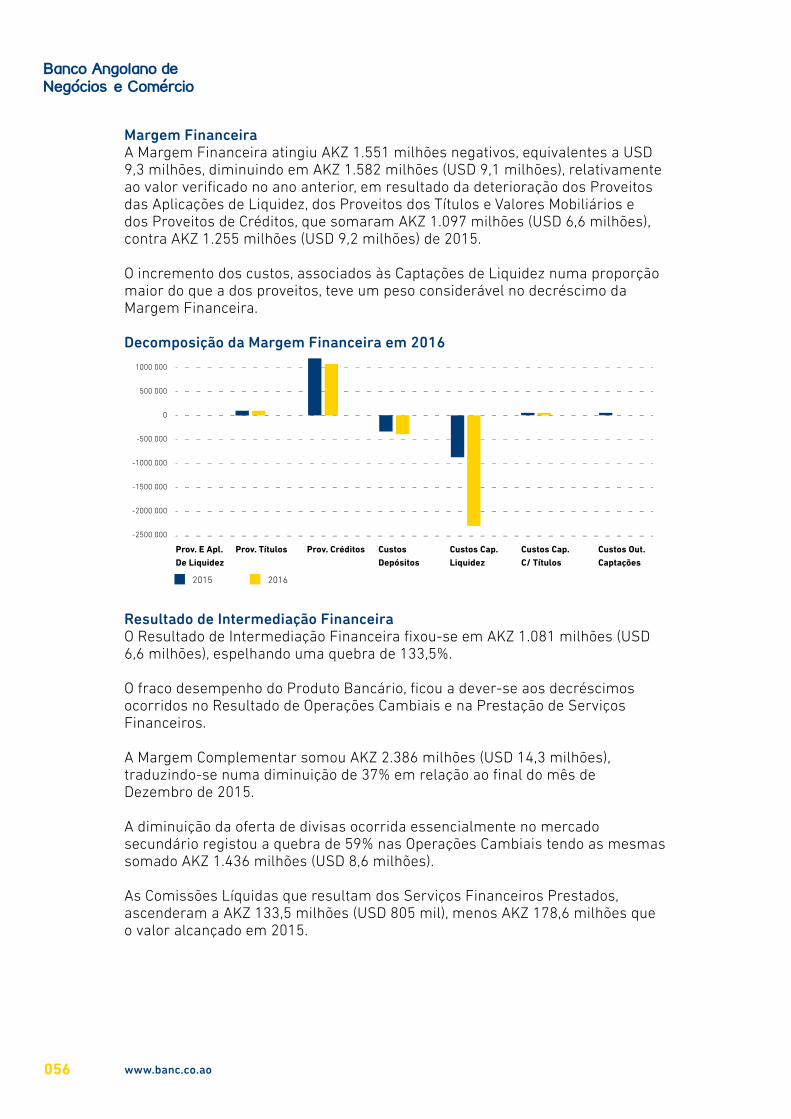

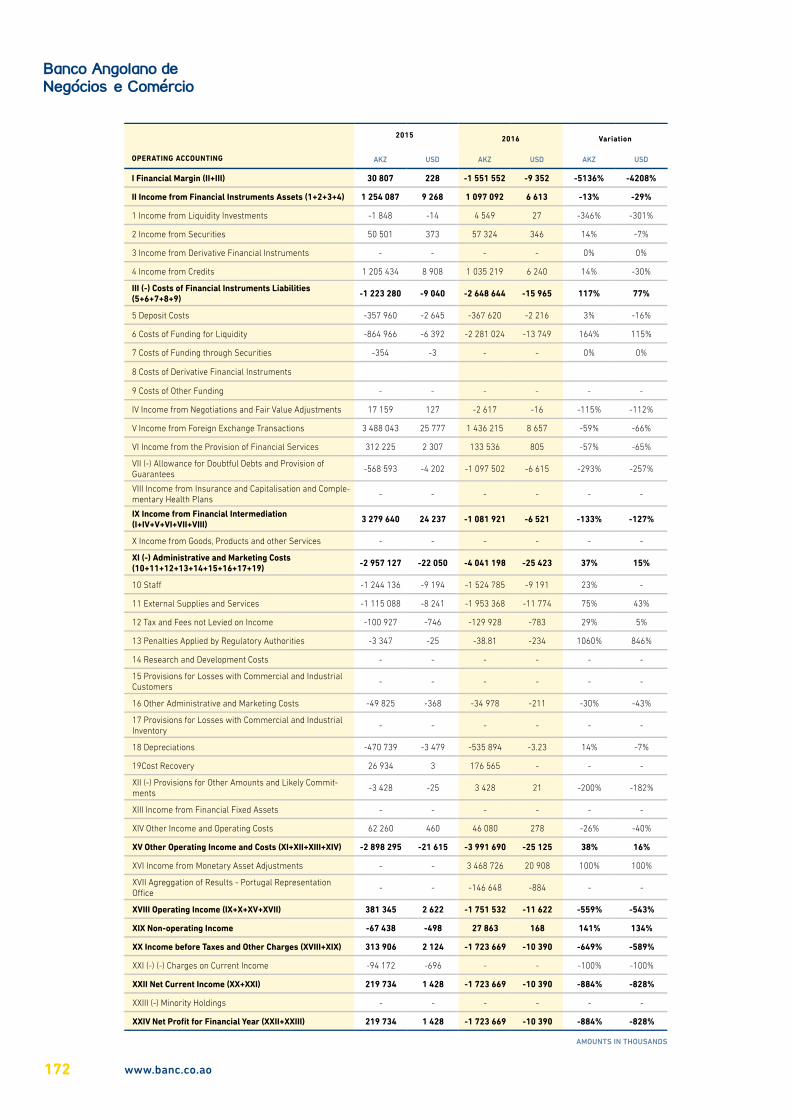

Margem FinanceiraA Margem Financeira atingiu AKZ 1.551 milhões negativos, equivalentes a USD 9,3 milhões, diminuindo em AKZ 1.582 milhões (USD 9,1 milhões), relativamente ao valor verificado no ano anterior, em resultado da deterioração dos Proveitos das Aplicações de Liquidez, dos Proveitos dos Títulos e Valores Mobiliários e dos Proveitos de Créditos, que somaram AKZ 1.097 milhões (USD 6,6 milhões), contra AKZ 1.255 milhões (USD 9,2 milhões) de 2015.

O incremento dos custos, associados às Captações de Liquidez numa proporção maior do que a dos proveitos, teve um peso considerável no decréscimo da Margem Financeira.

Decomposição da Margem Financeira em 2016

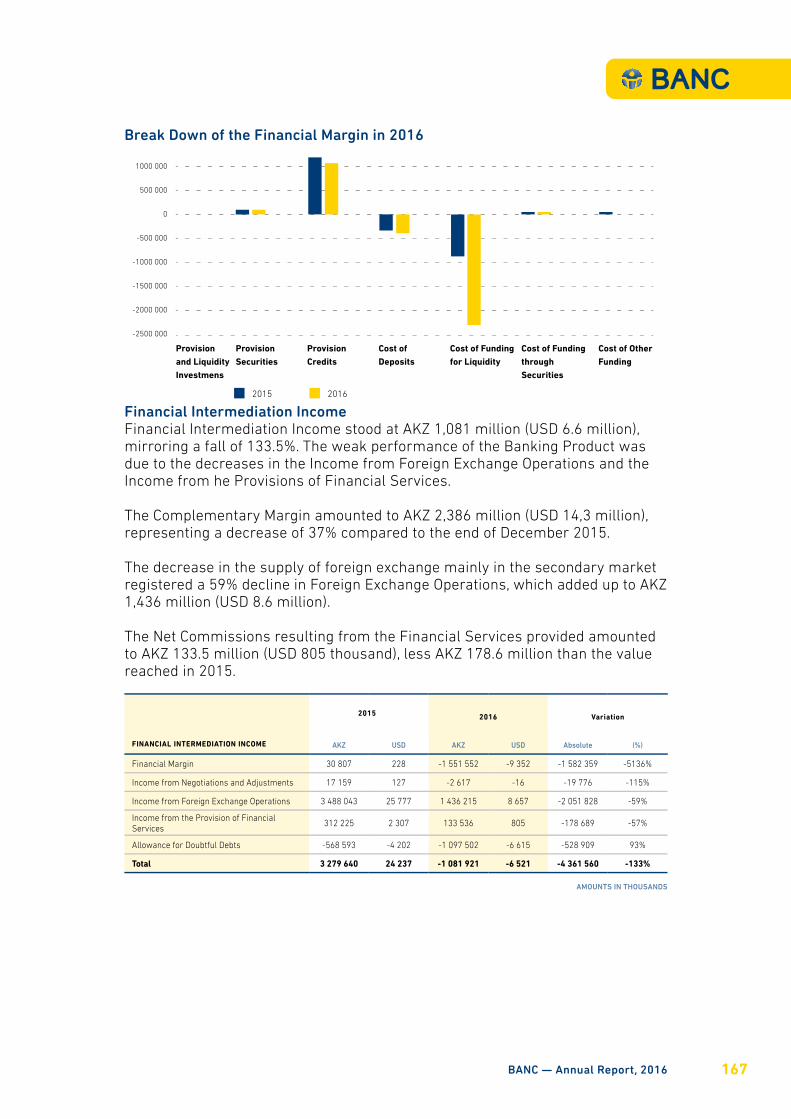

Resultado de Intermediação FinanceiraO Resultado de Intermediação Financeira fixou-se em AKZ 1.081 milhões (USD 6,6 milhões), espelhando uma quebra de 133,5%.

O fraco desempenho do Produto Bancário, ficou a dever-se aos decréscimos ocorridos no Resultado de Operações Cambiais e na Prestação de Serviços Financeiros.

A Margem Complementar somou AKZ 2.386 milhões (USD 14,3 milhões), traduzindo-se numa diminuição de 37% em relação ao final do mês de Dezembro de 2015.

A diminuição da oferta de divisas ocorrida essencialmente no mercado secundário registou a quebra de 59% nas Operações Cambiais tendo as mesmas somado AKZ 1.436 milhões (USD 8,6 milhões).

As Comissões Líquidas que resultam dos Serviços Financeiros Prestados, ascenderam a AKZ 133,5 milhões (USD 805 mil), menos AKZ 178,6 milhões que o valor alcançado em 2015.

1500 000

1000 000

500 000

0

-500 000

-1000 000

-1500 000

-2000 000

-2500 000

2015 2016

Prov. E Apl.De Liquidez

Prov. Títulos Prov. Créditos Custos Depósitos

Custos Cap. Liquidez

Custos Cap. C/ Títulos

Custos Out. Captações

www.banc.co.ao056

Produto Bancário

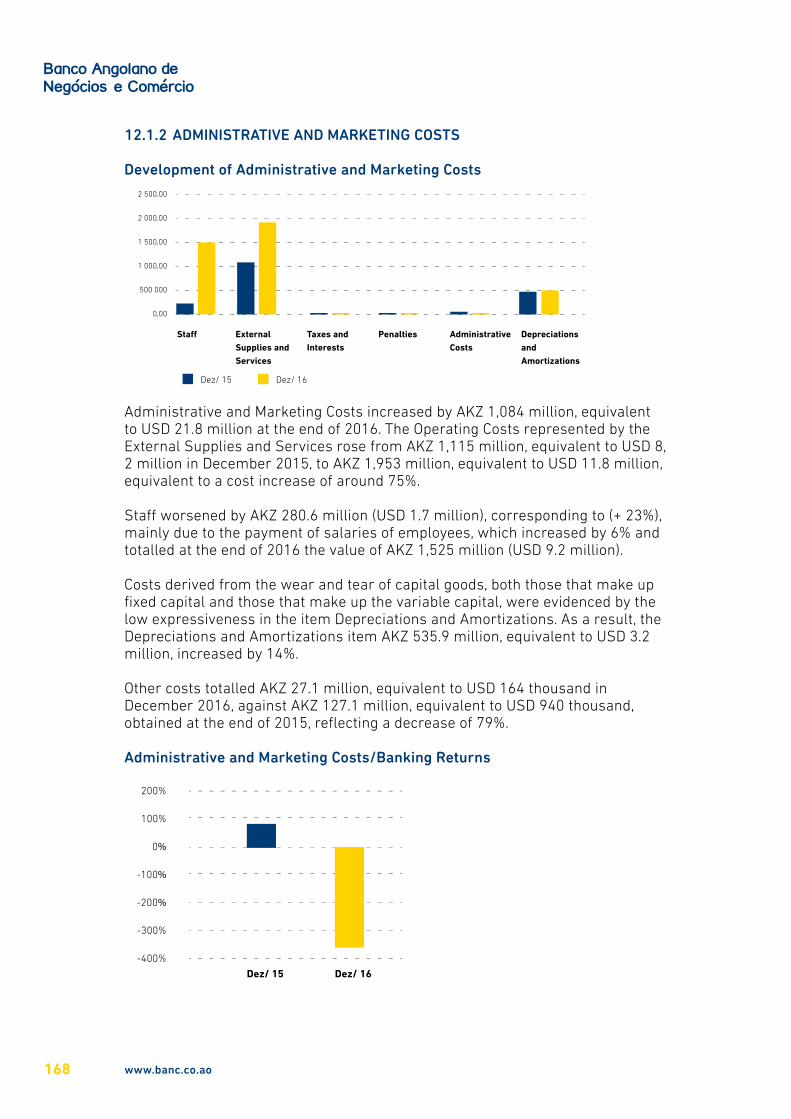

12.1.2 CUSTOS ADMINISTRATIVOS E DE COMERCIALIZAÇÃO

Evolução dos Custos Administrativos e de Comercialização

RESULTADO DE INTERMEDIAÇÃO FINANCEIRA

2015 2016 Variação

AKZ USD AKZ USD Absoluta (%)

Margem Financeira 30 807 228 -1 551 552 -9 352 -1 582 359 -5136%

Resultados de Negóciações e Ajustes 17 159 127 -2 617 -16 -19 776 -115%

Resultados de Operações Cambiais 3 488 043 25 777 1 436 215 8 657 -2 051 828 -59%

Resultados de Prestação de Serviços Finan-ceiros

312 225 2 307 133 536 805 -178 689 -57%

Provisões para Crédito de Liquidação Duvi-dosa

-568 593 -4 202 -1 097 502 -6 615 -528 909 93%

Total 3 279 640 24 237 -1 081 921 -6 521 -4 361 560 -133%

VALORES EM MILHARES

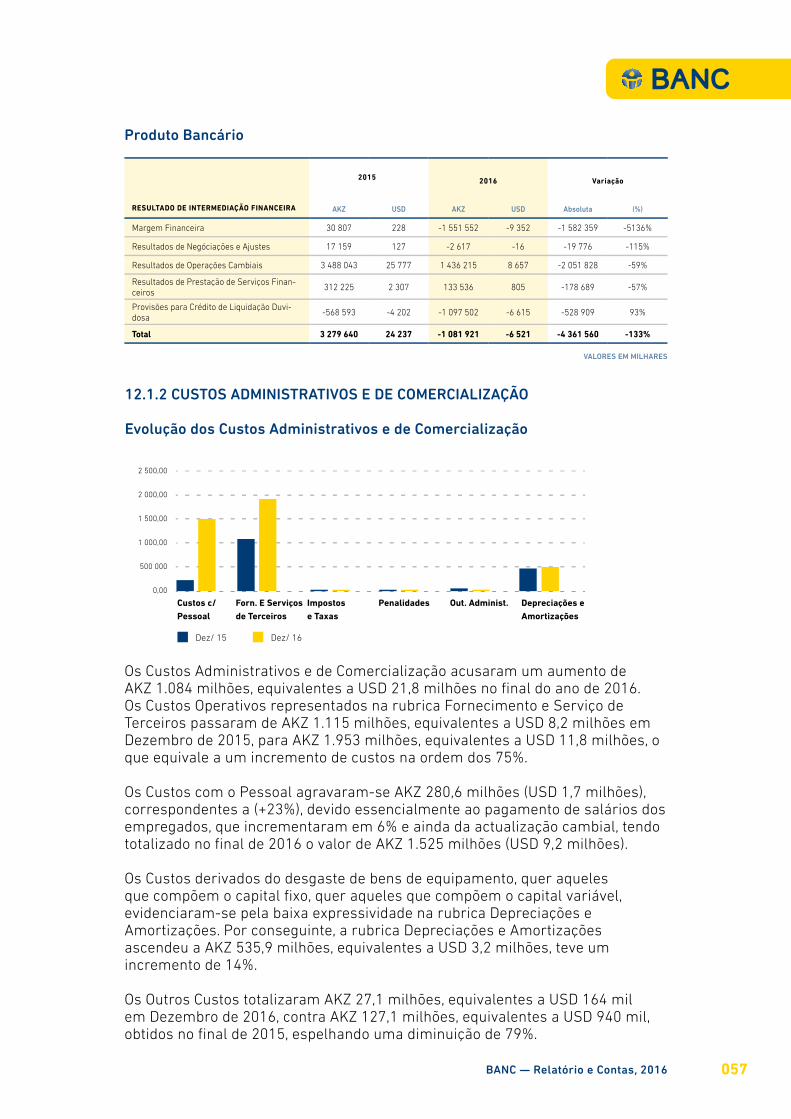

Os Custos Administrativos e de Comercialização acusaram um aumento de AKZ 1.084 milhões, equivalentes a USD 21,8 milhões no final do ano de 2016. Os Custos Operativos representados na rubrica Fornecimento e Serviço de Terceiros passaram de AKZ 1.115 milhões, equivalentes a USD 8,2 milhões em Dezembro de 2015, para AKZ 1.953 milhões, equivalentes a USD 11,8 milhões, o que equivale a um incremento de custos na ordem dos 75%.