PALM OIL: AMAPÁ FEASIBILITY ASSESSMENT

www.panconsult.com.br [email protected]

CURITIBA > Rua Euzébio da Motta, 900 – CEP 80.530-260 - Tel./Fax +55 41 3322 4487 – Curitiba/PR FLORIANÓPOLIS > Av. Pref. Osmar Cunha, 126 – Sala 708 – CEP 80.015-100 – Tel. +55 48 3204 8885 – Florianópolis/SC

APRIL 26TH, 2013

PALM OIL: AMAPÁ FEASIBILITY ASSESSMENT

1. Introduction Yield Palm oil has the highest oil yield per hectare, it requires the lowest fer7lizer investment and has a produc7ve cycle of about 25 years. However, it needs a long lead 7me between plan7ng and produc7ve harvest( 2-‐4 years). Cul7va7on requires sunshine, rainfall evenly distributed during the year and rage of temperature between 24 and 32 degrees, therefore the areas for cul7va7on are located around ten degrees off the equator. The produc7vity will vary by the agronomic prac7ce, specially behind the seed quality, fer7lizing investment and handling (i.e. right harves7ng moment). Currently there are a substan7al gap between the yields of smallholders and large planta7on companies (World Bank Group 2010) and also, between countries, such as Ecuador with 1.99 ton/ hectare vs. Costa Rica with 4.1 ton/ hectare.

Consumption In 2005 palm oil surpassed soybean oil as the most consumed oil in the global vegetable oils market. From 2004 to 2010 global consump7on of vegetable oil grew more than 35%, to around 147 million tonnes. OECD-‐FAO projects an increase to 184 million tons in 2019/2020, with China, India and Brazil leading the consump7on growth. Oil palm will drive the produc7on growth as it has the highest output per hectare, reducing the burden of addi7onal land.

The major palm oil applica7on are: -‐ Food segment: cooking oils and frying fats; margarine and spreads; shortenings; confec7onary and bakery fats; ice cream; coffee creamers and filled milk; emulsifiers and vitamin E supplements. -‐ Non food segment: soap, shampoo and detergents; animal feed; energy genera7on, biodiesel and lubricants; cosme7cs; pharmaceu7cals; organic fer7lizers from biomass; paints; plas7cizers, stabilizers for rubber and pvc.

The primary produc7on regions for palm oil are Indonesia and Malaysia and its produc7on is economically vital for them and their rural communi7es. This industry is labor-‐intensive, requiring an average of five workers per hectare. Compe7ng oil crops o`en require approximately one worker for every 200 hectares. In the next page we can see the trade flows of palm oil between the primary produc7on regions for palm oil and their respec7ve flows into the world’s primary palm oil consumer markets (India, Indonesia, China, EU, and the U.S.).

Figure 1.2: Worldwide oil palm yield per hectare – ISTA Mielke Sep’10

Figure 1.1: Worldwide oil yield per hectare – ISTA Mielke Sep’10

Figure 1.3: Worldwide consumpDon composiDon of vegetable oils and fats in 2004 and 2010 – ISTA Mielke Sep’10

PALM OIL: AMAPÁ FEASIBILITY ASSESSMENT

Looking ahead, according to the Food and Agricultural Policy Research Ins7tute (FAPRI, April 2010), palm oil produc7on in Indonesia (+7.8 million tonnes) and Malaysia (+4.9 million tonnes) will increase to a total of 52.6 million tonnes in the next decade (figure 1.5). Although there is a challenge regarding palm areas expansion, yield improvement will be the key factor for produc7on growth. Woods Hole Research Centre (WHRC) indicates Brazil in par7cular and to a lesser extent the Andes region and Central Africa as areas with the most poten7al to develop oil palm planta7ons outside Indonesia and Malaysia. For the next decade, LMC Interna7onal expects a growth to 11.1 million tonnes of palm oil in these areas (figure 2.5), 46% of which will be produced by Thailand (2.9 million tonnes) and Colombia (2.2 million tonnes). The expansion in Colombia, the largest palm oil producer in the Americas, is partly being funded by the United States Agency for Interna7onal Development to reseile disarmed paramilitary members on arable land

Figure 1.4: Major Trade Flows of Palm Oil – ISTA Mielke Sep’10

Figure 1.5: Global development of palm oil producDon in the period 2010-‐2020 –a FAPRI, b LMC, c ISTA Mielke Sep’10

PALM OIL: AMAPÁ FEASIBILITY ASSESSMENT Palm oil value chain The palm oil value chain can be divided into upstream produc7on and downstream processing. During the upstream produc7on to preserve the quality of palm oil, the fresh fruit bunches (FBB) and loose fruits must be milled within 24 hours of harves7ng. The FBB are sterilized by steaming under high pressure and the fruitlets are separated from the palm bunches. The fruitlets are mechanically pressed to obtain crude palm oil (and palm kernel oil). No solvents are used to extract the oil. By means of centrifuga7on, the crude palm oil (CPO) is separated from waste and water. Tradi7onally, CPO is a popular cooking oil in the tropical belt of West Africa. The empty fruit bunches and liquid waste resul7ng from these processes are used as fer7lizers in planta7ons. In the downstream processing the conversion of CPO into refined oil involves the removal of impuri7es, colors and flavors by refining, bleaching and deodoriza7on (RBD). RBD palm oil may be separated (frac7onated) into liquid and solid frac7ons by thermo-‐mechanical means (controlled cooling, crystalliza7on, and filtering). The liquid frac7on (olein) is used extensively as a liquid cooking oil in tropical climates, compe7ng successfully with the more expensive groundnut, corn and sunflower oils. It is possible to process palm olein and stearin further (e.g. double frac7ona7on, interesterifica7on and hydrogena7on) to produce specialty fats or split them into oleo chemical products such as glycerol and faiy acids.

Figure 1.5: Palm Oil Value Chain – MVO Fact Sheet 11-‐2010

2. Major worldwide consumers details Key international markets Among the three biggest interna7onal markets, China is the one with less CPO importance.

Figure 2.1: ComposiDon palm oil imports EU 27, India and China – EUROSTAT, Prod. Board MVO, G. Trade Atlas, Solvent Extractors’ Assoc. of India

PALM OIL: AMAPÁ FEASIBILITY ASSESSMENT Netherlands is the biggest European country importer but as shown in the figure 2.3 they export most of it. This export volume mainly consisted in RBD palm oil and palm olein, most of it sold to Belgium and Germany.

Figure 2.2: Major importers of palm oil* 2009 – Eurostat, 1Product Board MVO 2010

EU import duties on palm oil EU applies a differen7al duty structure to the import of palm oil. The applicable duty rate depends on the stage of processing, origin and applica7on of the product. Based on the EU’s Generalized System of Preferences (GSP) palm oil imports origina7ng in developing countries such as Thailand, Brazil and Nigeria, are eligible for considerable duty reduc7ons while imports from GSP+ countries (e.g. Andes and Central American countries) are eligible for duty free access to the EU.

Figure 2.3: Dutch imports, consumpDon and re-‐export of palm oil – Product Board MVO, September 2010

Figure 2.4: EU import duDes on palm oil – EUROSTAT, Prod. Board MVO, G. Trade Atlas, Solvent Extractors’ Assoc. of India

PALM OIL: AMAPÁ FEASIBILITY ASSESSMENT

Figure 3.1: Worldwide Palm Oil ProducDon (‘000T), ProducDvity (T/ha) and ProducDon Area – Oil World 2012

3. Brazilian Market In the last years Brazil increased its produc7on mainly behind the increase of the produc7vity improvement, jumping from 2.31 to 2.82 T/ha in the last four years.

Key Player – Agropalma Group The leading Brazilian company is Agropalma Group -‐ a 100% Brazilian private capital company -‐ started its ac7vi7es in 1982. Agropalma represents more than 70% of total Brazilian palm oil produc7on and it’s also leading the palm oil produc7on in La7n America, plus controlling the en7re produc7on chain, from seedling to refined oil, vegetable fats and margarine. The Agropalma Group directly employs more than 4,200 people who live in agro communi7es provided by the Group, with complete water, electricity and sewage infrastructure. The communi7es are also provided with schools, clubs, and health center as well as informa7on technology infrastructure connec7ng the units located in Tailândia, Acará, Belém and São Paulo. Crude oil leaves the mills in Tailândia and Acará ci7es and is taken in ferries to its tanking facili7es in Belém, Capital of the State of Pará, where the refinery and the margarine and fats unit are located since 1997. The refinery has a produc7on capacity of 320/tonnes/day. See below the group structure:

• 107,000 hectares of land; • 39,000 hectares of planta7on; • 1.600 km of private roads; • 05 crude oil extrac7on mills; • 01 export terminal; • 01 palm oil and kernel oil refinery plant; • 01 Vegetable fats, spreads, and margarine packing unit; • 04 laboratories of quality control; • Electrical power genera7on for the industrial process; • 04 water treatment sta7ons.

PALM OIL: AMAPÁ FEASIBILITY ASSESSMENT

Figure 3.2: RSPO Members in Brazil – RSPO 2012

Agropalma Group – Conference Call Talking with Mr. Marcello Brito, Agropalma’s commercial director, we were able to get his general overview and feedback from the Brazilian palm oil status and mid term perspec7ve, according to his point of view:

“Brazil is nowadays producing around 300M ton and impor7ng 400M tons, out of this 200M tons is kernel. There are two main challenges regarding oil palm produc7on in Brazil: i) Produc7on cost: around 50% of the produc7on cost is manpower and according to a study Agropalma purchased in UK last year, Brazilian manpower is the most expensive country when compared with the 43 producing countries in the world and it’s over 300% more expensive than benchmarks in Asia while the closest cost is Colombia, about 10% less expensive. Part of this cost is due to the people you need to recruit in the yield, most of them (90%) are not na7ve from Pará, what makes the opera7on complex and expensive. In the next 2 years 9,250 direct workers, this means a flow of approximately 37 thousand people. ii) Loca7on: the consump7on of biodiesel and food/ cosme7c oil are not concentrated in the north but in the south of the country. The fleet from Belém to São Paulo is more expensive than the fleet from Malaysia or Indonesia to Santos. Regarding the demand perspec7ve, globally we have and oversupply of 3.5 millions tons above the demand, for this reason the prices are not airac7ve. In the Brazilian market, there is a poten7al increase in the consump7on behind biodiesel, but it depends on poli7cal decisions to increase or not the mix in the common diesel and that is out of our control. In the end of 2011 Vale purchased Biopalma with the inten7on to produce B20 (20% biodiesel + 80% diesel) for their consump7on in their fleet of locomo7ves, machinery and equipment in the region. The issue is that the refinery will be ready only in 2015 and Vale is flooding the market of palm oil at cost price (80M tons). This context made Agropalma boiom line results reduce 58% in 2012 vs. 2011 and due to that, Agropalma frozen all the expansion plans un7l 2016, when will review this decision. Currently Agropalma produces the margarine Vitapalma, focused exclusively to food-‐service (bakeries, ice cream factories, bars and restaurants).”

RSPO Agropalma received the interna7onal cer7ficate issued by the RSPO (Roundtable on Sustainable Palm Oil) in August 2011, enabling them to export to countries and customers (most abroad) where RSPO is a pre-‐requirement. There is a public commitment to use exclusively RSPO palm oil as of late 2015 made by that some consump7on giants such as Unilever, Cargill, Nestlé, Carrefour, Tesco, Wal-‐Mart, Henkel, among dozens of others, and even countries like Holland and Belgium. "It is expected that this market then reaches a plateau between 12 and 15 million tons per year, equivalent to more than three 7mes the current market," says Brito. See below the companies that par7cipated in the RSPO event in Belém late 2012.

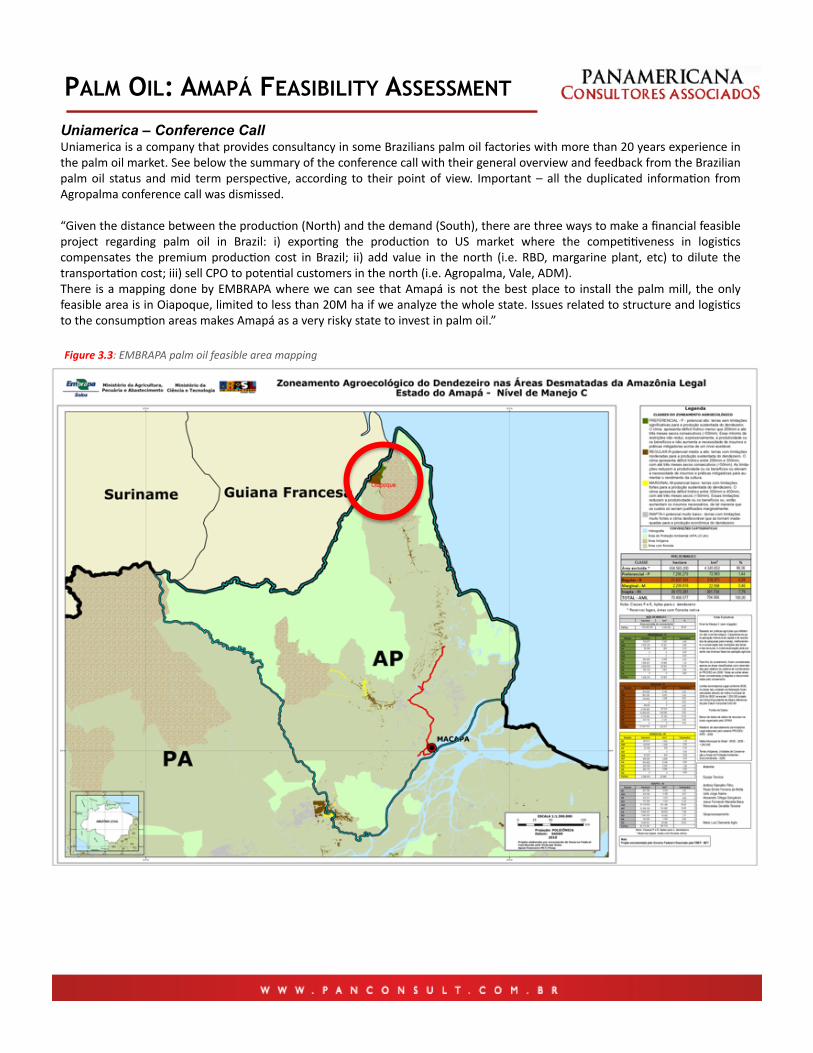

PALM OIL: AMAPÁ FEASIBILITY ASSESSMENT Uniamerica – Conference Call Uniamerica is a company that provides consultancy in some Brazilians palm oil factories with more than 20 years experience in the palm oil market. See below the summary of the conference call with their general overview and feedback from the Brazilian palm oil status and mid term perspec7ve, according to their point of view. Important – all the duplicated informa7on from Agropalma conference call was dismissed.

“Given the distance between the produc7on (North) and the demand (South), there are three ways to make a financial feasible project regarding palm oil in Brazil: i) expor7ng the produc7on to US market where the compe77veness in logis7cs compensates the premium produc7on cost in Brazil; ii) add value in the north (i.e. RBD, margarine plant, etc) to dilute the transporta7on cost; iii) sell CPO to poten7al customers in the north (i.e. Agropalma, Vale, ADM). There is a mapping done by EMBRAPA where we can see that Amapá is not the best place to install the palm mill, the only feasible area is in Oiapoque, limited to less than 20M ha if we analyze the whole state. Issues related to structure and logis7cs to the consump7on areas makes Amapá as a very risky state to invest in palm oil.”

Figure 3.3: EMBRAPA palm oil feasible area mapping

PALM OIL: AMAPÁ FEASIBILITY ASSESSMENT Vale Vale kicked off in its program to inaugurate a biodiesel produc7on plant palm oil, in the city of Moju, Pará . The project includes the construc7on of a second unit in Acará and a plan to transform the palm oil biodiesel as of2015. The total es7mated investment in the is about $ 500 million. The goal is to supply Vale’s demand for renewable fuel for the use of so-‐called B20, composi7on of 20% biodiesel with 80% diesel in its fleet of locomo7ves, machinery and equipment in the country. The first plant will be able to extract 120 tons / hour of fresh fruit bunches. When installed the second unit, which according to the Vale, will be the world's largest in the segment, the number will rise to 680 tons / hour. The use of biofuels is a way found to achieve the target of 5% reduc7on in emissions of carbon dioxide (CO2), which today are around 12 million tons per year by 2020. "We aim to achieve 5% savings on the level of emissions," said the chairman, Murilo Ferreira, adding that the goal includes provision for expansion of Vale’s ac7vi7es.

ADM ADM entered the palm oil business in Pará and will allocate the harvest in its 12M ha for oil produc7on driven to food and cosme7cs industry. With the first harvest planned for 2015 in the ci7es of Irituia, São Domingos do Capim, Mãe do Rio and São Miguel do Guamá, ADM now has the poten7al to crush 60 tons of bunches per hour. By 2021, when the trees planted now are ripe and at the peak of their produc7vity, oil produc7on is expected to reach the mark of 60 000 tonnes of crude oil per year.

Petrobras Petrobras sees much in biofuel produc7on. To Biodiesel Project, where Petrobras is inves7ng in a program that should involve 1,250 family farmers and generate a total of 5,000 direct jobs. The project includes the installa7on of two complex for the extrac7on of palm oil and the implementa7on of a biodiesel plant in Pará, in the city of Mocajuba.

Importing companies The Brazilian Ministry of External Rela7ons launched a Catalogue of Brazilian Importers (CIB) that provides full details of 7,672 companies, rela7onships with company and product list with product descrip7on. Listed companies represent 78.32% of the volume imported by the country annually. This is the most complete catalog of importers already provided by the Brazilian government. See below the list of companies that imported olive oil palm.

Other companies There are exporters list available Brazil Global Net tool that the Brazilian Ministry of External Rela7ons launched, such as Scomex Comercio Exterior (PE), Agorey Trading Ltda (SP), Ecolub Assistance Ltda (SP), Exporta Bahia Ltda (BA), Frozfo Comércio Importação & Exportação Ltda (SP) and Ortos Engenharia Ltda (RJ). Other poten7al Brazilian customers that appeared in the research done in this study were Aboissa Óleos Vegetais Ltda (SP) and Indústria Yossam Ltda (PA).

Figure 3.4: Catalogue of Brazilian Importers – Brazilian Ministry of External RelaDons – updated on April’13

PALM OIL: AMAPÁ FEASIBILITY ASSESSMENT

4. Key Conclusions Location There are three key variable that may influence the decision regarding the loca7on of the palm oil mill: logis7cs, local structure/ government support, land & weather profile.

Recommenda/on: meet to different stake holders prior to the loca7on defini7on such as EMBRAPA Amazonia Oriental, government, poten7al customers, fleet companies, Abrapalma, etc. Other topics to be discussed and addressed in these mee7ngs are the people availability & recruitment and structure needed to accommodate these families.

Potential Customers Worldwide in the long term there is an increasing consump7on trend on palm oil. As this is a commodity, compe77ve produc7on cost, logis7cs and cer7fica7on are the key to make financial sense to the project. Currently there are customers purchasing local and imported palm oil in Brazil, however the logis7cs doesn’t help. The biggest poten7al growth in Brazil in the mid term will be behind biodiesel.

Recommenda/on: meet to big poten7al customers to close a partnership prior to invest in a palm oil mill or refinery. Among the biggest customers we may highlight Agropalma, Vale, Petrobras, ADM, Cargill, Bunge and Unilever. Other alterna7ve is to contact poten7al customers in US market given the logis7cs and/ or Europe given the tax compe77veness & cer7fica7ons requirement.

Figure 4.1 : EMBRAPA palm oil feasible area mapping