avisos legais - fibria – relações com investidores itour _final_port_271016.pdf · avisos...

TRANSCRIPT

Avisos Legais

As informações contidas nesta apresentação podemincluir afirmações que constituem estimativas,conforme o significado disposto na Seção 27A do U.S.Securities Act de 1933 e emendas ao mesmo e naSeção 21E do U.S. Securities Exchange Act de 1934 eemendas ao mesmo.

Tais estimativas envolvem um certo grau de risco eincerteza em relação às previsões empresariais,financeiras, de tendências, estratégicas e outras,podendo estar baseadas em premissas, dados oumétodos que, apesar de considerados razoáveis pelaempresa naquele dado momento, podem se revelarincorretos, imprecisos ou mesmo infactíveis.

A empresa não dá qualquer garantia deque as expectativas expostas nesta apresentação seconfirmarão.

Os investidores em potencial ficam desde já avisadosque as referidas estimativas não são garantias dedesempenho futuro e envolvem riscos e incertezas.

Ficam também avisados que os resultados reaispoderão ser bastante diferentes daqueles dados nasestimativas, devido a vários fatores que incluem, masnão se limitam aos riscos inerentes dos negóciosinternacionais e outros riscos previstos nosdocumentos arquivados pela empresa junto à CVM e àSEC.

Fica desde já declarado que a empresa não assumiráqualquer obrigação de atualizar as estimativas, asquais representam apenas a data na qual foram feitas.

THE FUTURE OF MARKET PULP

5TH INVESTOR TOURARACRUZ, 21-22 SEPTEMBER 2016

A PRESENTATION BY MR. JOÃO CORDEIRO

COPYRIGHT©PÖYRY

FIBRIA INVESTOR TOUR 2016

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

COPYRIGHT©PÖYRYSEPTEMBER 2016

FIBRIA INVESTOR TOUR 2016

THE FUTURE OF MARKET PULP

“What drives demand for market pulp ?”1

“How substitution of fibres will evolve ?”2

“Where will the new supply come from ?”3

“What is happening in the next five years ?”4

“How to create long-lasting shareholder value ?”5

COPYRIGHT©PÖYRYSEPTEMBER 2016

FIBRIA INVESTOR TOUR 2016

“What drives the demand for

market pulp?”1

COPYRIGHT©PÖYRY

DEMAND DRIVERS FOR BEKP:

FIRST…

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

Organic Growth• A multitude of applications

• The geography of megatrends

COPYRIGHT©PÖYRY

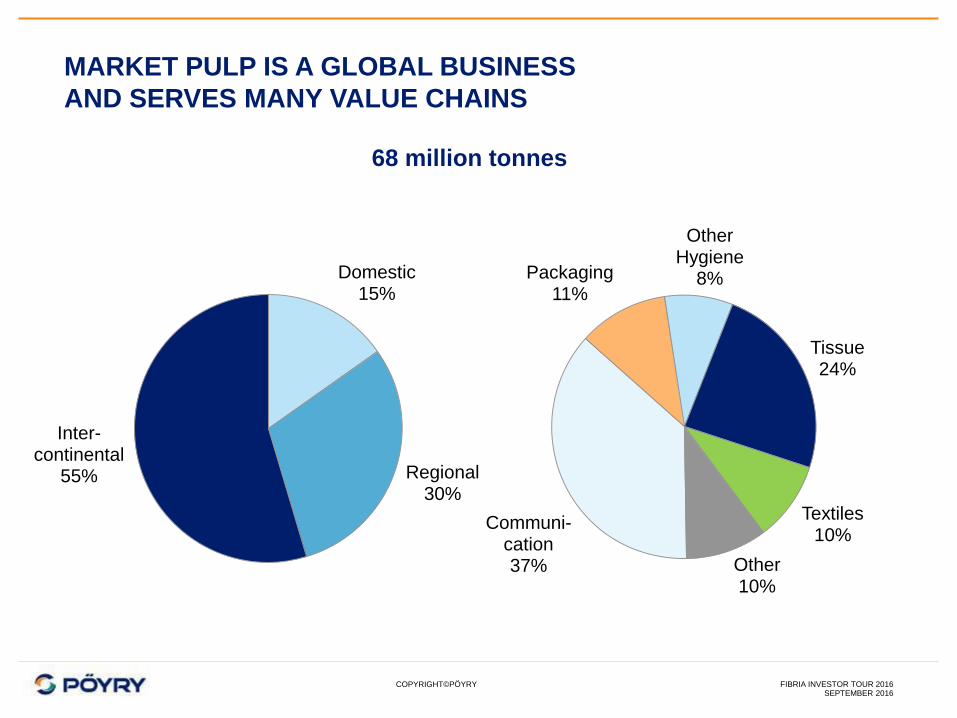

MARKET PULP IS A GLOBAL BUSINESS

AND SERVES MANY VALUE CHAINS

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

Domestic15%

Regional30%

Inter-continental

55%

Communi-cation37%

Packaging11%

Other Hygiene

8%

Tissue24%

Textiles10%

Other10%

68 million tonnes

COPYRIGHT©PÖYRYSEPTEMBER 2016

FIBRIA INVESTOR TOUR 2016

CONSUMPTION PATTERNS ARE RAPIDLY CHANGING

Total Paper & Board Demand

in the “West”

0

100

200

300

2000 2010 2020 2030

Mil

ha

res

Million tonnes

0

100

200

300

2000 2010 2020 2030

Mil

ha

res

Million tonnes

Graphic Papers

Packaging Papers

Tissue

Graphic Papers

Packaging Papers

Tissue

West = North America, Western Europe, Japan, Oceania

East = All other world regions

Total Paper & Board Demand

in the “East”

COPYRIGHT©PÖYRY

0

10

20

30

40

50

0

2

4

6

8

10

1980 1995 2010

Ctd. Mech., W. Europe (left)

Mech. pulp, Global (right)

Mechanical

pulp

Ctd Mech

Papers

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

Growth

FROM A LIFE CYCLE PERSPECTIVE

BEKP AND TISSUE ARE GROWTH SEGMENTS

0

10

20

30

40

50

0

5

10

15

20

25

1980 1995 2010

Tissue, China (left)

Market BEKP, Global (right)

Tissue

China

Market BEKP

0

5

10

15

20

25

0

4

8

12

16

20

1980 1995 2010

Newsprint, North Am. (left)

Sulfite pulp (right)

Newsprint

North America

Sulphite pulp

Demand M t/a

Maturity Decline

COPYRIGHT©PÖYRY

GROWING PRODUCTION OF TISSUE AND PACKAGING PAPERS

COMPENSATES FOR THE DECLINE IN GRAPHIC SEGMENT

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

0

50

100

150

200

Graphic

PapersTissue

White

Packaging

Papers

Specialties

Million tonnes

196

-15.6

+13.3 +6.4 +2.1 202

Paper and Paperboard Production Development

grades using Bleached Kraft Pulp only

2014 2025

COPYRIGHT©PÖYRYSEPTEMBER 2016

IMPROVED HYGIENE STANDARDS

AND MORE WHITE PACKAGING

23,528,7

+3.6 -2.4 +2.8+1.2

0

20

40

60

2014 Fluff Graphic Tissue Pack. &Spec.

2030

Million tonnes

Demand

Decline 2014-2030

Increment 2014-2030

28,9

44,6

+0.4

+12.5+2.8

0

20

40

60

2014 Graphic Tissue Pack. &Spec.

2030

Million tonnes

Global demand growth for

BSKP Market Pulp

Global demand growth for

BHKP Market Pulp

FIBRIA INVESTOR TOUR 2016

COPYRIGHT©PÖYRYSEPTEMBER 2016

CHINA IS RESPONSIBLE FOR MORE THAN 60%

OF THE WORLD’S INCREMENTAL DEMAND

Demand for papermaking market pulps

61

82

1

13

62 1

0

15

30

45

60

75

90

2014 NorthAmerica

WesternEurope

Japan EasternEurope

China Rest ofAsia

LatinAmerica

Others 2030

Million tonnes

FIBRIA INVESTOR TOUR 2016

Demand

Decline 2014-2030

Increment 2014-2030

COPYRIGHT©PÖYRYSEPTEMBER 2016

FIBRIA INVESTOR TOUR 2016

Global Middle Class

GROWTH IN ASIA IS EMPOWERED BY URBANIZATION

AND INCREASING DISPOSABLE INCOME

Urban Population in China and India

0,0

0,2

0,4

0,6

0,8

1,0

1,2

2000 2015 2030 2045

Billion people living in cities

+165 Mi

+220 Mi

0

1

2

3

4

5

2000 2010 2020 2030

Middle class population – billion

China

India

China

India

OECD

Rest of the World

COPYRIGHT©PÖYRY

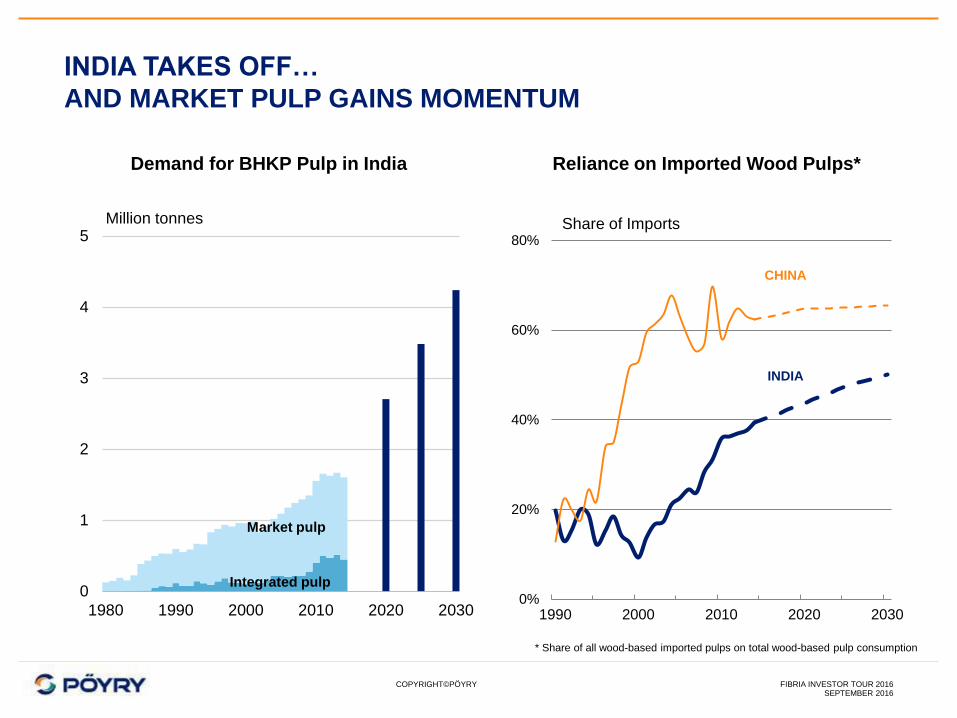

INDIA TAKES OFF…

AND MARKET PULP GAINS MOMENTUM

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

Demand for BHKP Pulp in India

0

1

2

3

4

5

1980 1990 2000 2010 2020 2030

Milh

are

s

Million tonnes

Integrated pulp

Market pulp

0%

20%

40%

60%

80%

1990 2000 2010 2020 2030

INDIA

CHINA

Reliance on Imported Wood Pulps*

Share of Imports

* Share of all wood-based imported pulps on total wood-based pulp consumption

COPYRIGHT©PÖYRY

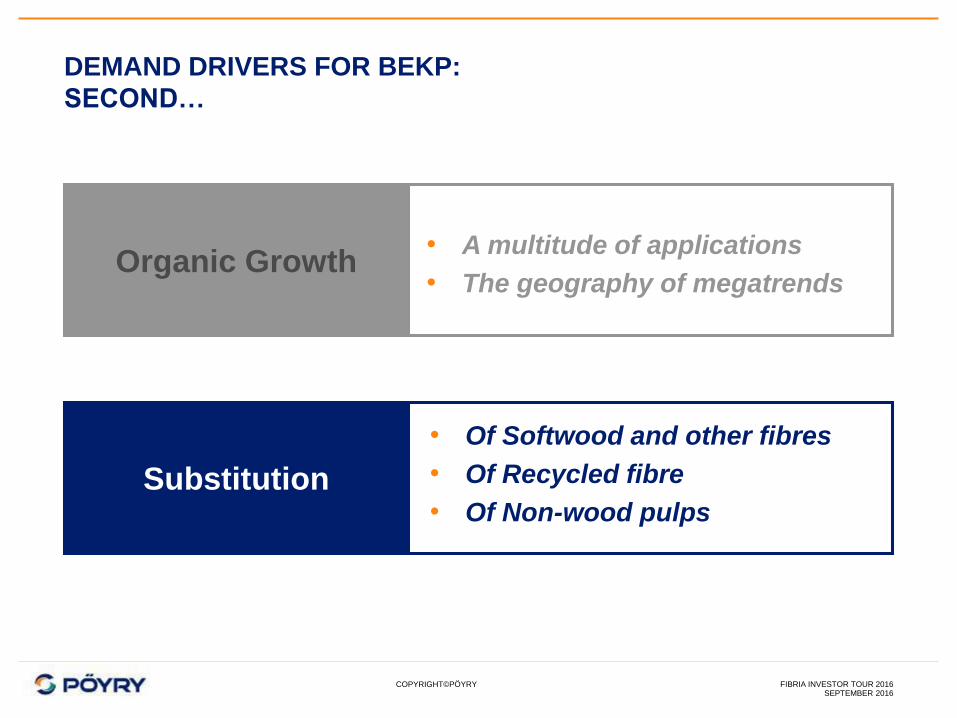

“How substitution of fibres

will evolve ?”2

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

COPYRIGHT©PÖYRY

DEMAND DRIVERS FOR BEKP:

SECOND…

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

Organic Growth

Substitution

• A multitude of applications

• The geography of megatrends

• Of Softwood and other fibres

• Of Recycled fibre

• Of Non-wood pulps

COPYRIGHT©PÖYRY

BHKP MARKET PULP

A HUGE POTENTIAL TO SUBSTITUTE OTHER FIBRES

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

0

50

100

150

200

Brownrecycled

fibres

Othervirginfibres

Whiterecycled

fibres

BHKPintegrated

BSKPNon-woodfibres

Other P&B

Packaging Papers

Tissue

Graphic Papers

Million tonnes

Other virgin fibres include mechanical, semi-chemical and unbleached kraft pulps

Current Global Consumption of Papermaking Fibres

BHKP

Market pulp

13

3032

6470

165

29

COPYRIGHT©PÖYRY

0%

50%

100%

150%

2015e Future

SUPPLY OF WHITE RECYCLED FIBRE IS UNDER STRESS

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

Virgin

Fibre

Recycled

Fibre

Example European Tissue Furnish

Fibre Migration

• Shift from recycled towards virgin fibre

Substitution between grades

• Limited attractiveness to invest in new

deinking capacity

Organic growth

• Tissue demand at 2%/a

• Sofwood looses share to hardwood

1

2

3

COPYRIGHT©PÖYRY

THE SHARE OF NON-WOOD PULP WILL DECLINE

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

Share of Non-Wood Pulp in ChinaConsumption of Non-Wood Pulp by Region

0

5

10

15

20

2000 2005 2010 2015 2020 2025 2030

Million tonnes

China

Rest of Asia-Pacific

Rest of the World

0%

2%

4%

6%

8%

10%

2013 2020 2025 2030

Bamboo

Straw

Bagasse

Other

In total papermaking fibre

8.3 M t

5 M t

COPYRIGHT©PÖYRYSEPTEMBER 2016

FIBRIA INVESTOR TOUR 2016

“Where will the new supply

come from?”3

COPYRIGHT©PÖYRY

THERE ARE LIMITED SPOTS IN THE WORLD

FOR LARGE-SCALE COMPETITIVE MARKET PULP PRODUCTION

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

Predominantly

softwood

Predominantly

hardwood

Availability of

softwood

plantations,

good for fluff

Some capacity

increase in

BSKP

Large land

availability, but

only a few spots

for large-scale

competitive

platforms

Major demand

increase in

construction: wood

panels, sawnwood,

Plantation development

potential –

regional challenges

Mountain pine

beetle

infestation

Supply shifting

from natural forest

to fast-growing

plantations –

limited industrial

sites

Wood export

platform to Asia,

eucalyptus

availability will

diminish

Good long-fibre wood availability

but logistics challenges

Bio-energy

usage

increasing

COPYRIGHT©PÖYRYSEPTEMBER 2016

FIBRIA INVESTOR TOUR 2016

Chinese Wood Demand by Sector

CHINESE WOOD DEFICIT MAY INCREASE FURTHER

0

50

100

150

SupplyDemand SupplyDemand

For pulp industry For other uses

Imports Domestic Supply

Index, 2014= 100

2014 2025

Chinese Pulpwood Costs

• The pulp making sector accounts for only

some 10% of the total demand, has little

bargaining power

• Wood imports will double in ten years

• Expansion of domestic market pulp supply

is rather limited

• Pulpwood costs are bound to increase

further

COPYRIGHT©PÖYRY

ASIAN PULP INDUSTRY HAS GROWN, BUT BASED ON

INCREASING DEPENDENCE ON IMPORTED WOOD CHIPS

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

0

5

10

15

20

25

1995 2000 2005 2010 2015

Japan

China

Taiwan

South Korea

India

Million BDMT

Hardwood Wood Chip Imports

Africa

Australia

Indonesia

Chile

& BrazilVietnam

Thailand

COPYRIGHT©PÖYRYSEPTEMBER 2016

FIBRIA INVESTOR TOUR 2016

Development of Wood Chip

Imports in Asia-Pacific

THERE ARE NEW PRESSURES ON ASIAN WOOD CHIP MARKETS

69

M m3

141

M m3

40

58

0

5

10

15

20

25

30

35

2015 2025 f

Japan

China

Other

250

300

350

400

450

500

2009 2010 2011 2012 2013 2014 2015 2016*

From Australia

From Vietnam

USD/ADT of pulp

Imported Fibre Costs

to Chinese Pulp Mills

Emerging Asia-Pacific wood chip demand drivers:

• Japanese nuclear power policy and guaranteed electricity price incentives to support bio-energy

• New pulp capacity in Indonesia reshuffles the wood chip markets

• Expansion of pulp production within China, Vietnam and Thailand

Million BDMT

COPYRIGHT©PÖYRY

TIGHTENING PLANTATION WOOD AND CHIP SUPPLY

COULD ADD TO THE CASH COST OF ASIAN PULP MILLS

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

Source: PöyryNote: Cash delivered costs include: wood costs (stumpage, harvesting, transport), chemicals, energy, labour, other manufacturing costs, pulp logisitic costs (mill to port, sea freight, insurance), mill overheads.

Excludes other SG&A, corporate costs, depreciation and capital charges.

0

250

500

750

0 5 10 15 20 25 30 35

Selected Mills in South

America

Selected Mills in

South East Asia

USD/ADt

BHKP Market Pulp Cash Costs to Shanghai – 2Q 2016

COPYRIGHT©PÖYRYSEPTEMBER 2016

FIBRIA INVESTOR TOUR 2016

“What is happening in

the next five years ?”4

COPYRIGHT©PÖYRY

0

5

10

15

20

25

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Capacity year end

Decided expansion

FOUR INVESTMENT WAVES: TRIGGERED BY ACCESS TO

LOW COST CAPITAL AND AVAILABLE FOREST LAND

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

1977-1979

• Cenibra

• Aracruz A

• Jari

Earlier

• Suzano

• Ripasa 1972

1991-1998

• Aracruz B

• Suzano Mucuri

• Cenibra

• Simao Jacareí

• Arauco

• CMPC

2002-2009

• Aracruz C

• Jacareí expansion

• Ripasa expansion

• Lwarcel expansion

• Veracel

• Mucuri B

• Fibria Três Lagoas I

• UPM Fray Bentos

1st wave 2nd wave 3rd wave

2012-2018

• Eldorado I

• Suzano Imperatriz

• CMPC Guaíba II

• Klabin Puma

• MdP

• Fibria Tres Lagoas II

Million tonnes of BHKP capacity

8% 18% 47% 57%

4th wave

Share of South America in global BHKP supply

COPYRIGHT©PÖYRY

1 MILLION TONNES OF MARKET CAPACITY

ARE REMOVED ANNUALLY

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

-2

-1

0

1

2

3

4

5

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Expansion New line

New mill Shut down

Decrease Net cap change

Capacity Exits 2005-15:

Total 1.0 M t/a

• Shut-downs 0.45 M t/a

• Other exits: 0.55 M t/a

New capacity exits will come from:

• Conversions to other grades

• Decreases in production

• Integration into papermaking

• Further shut-downs

Historical Market BHKP Capacity Changes

million tonnes

COPYRIGHT©PÖYRY

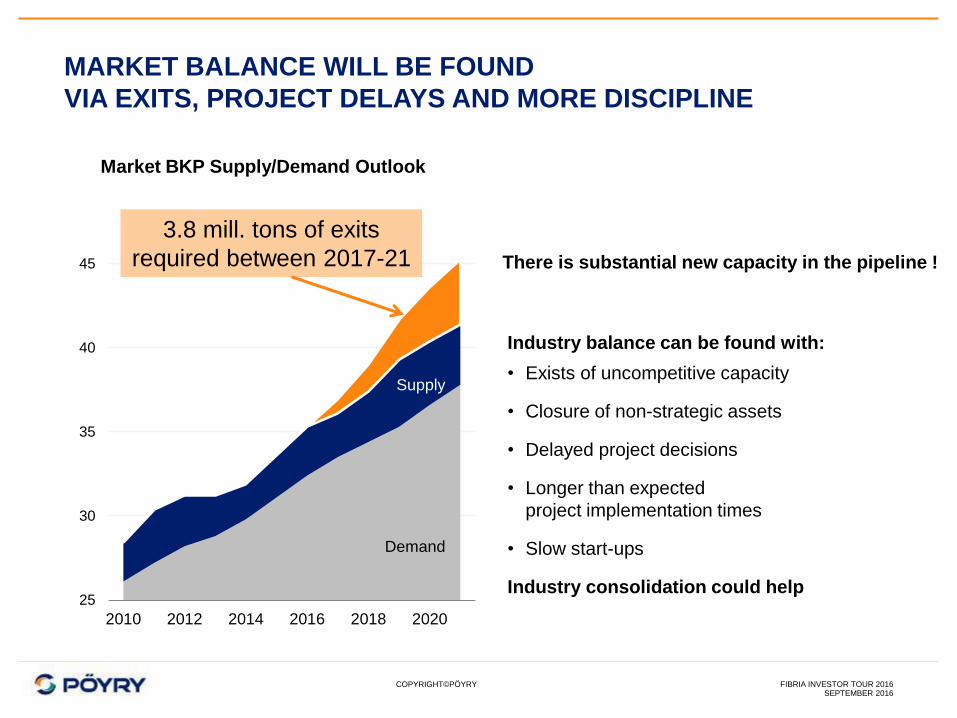

MARKET BALANCE WILL BE FOUND

VIA EXITS, PROJECT DELAYS AND MORE DISCIPLINE

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

Market BKP Supply/Demand Outlook

Industry balance can be found with:

• Exists of uncompetitive capacity

• Closure of non-strategic assets

• Delayed project decisions

• Longer than expected

project implementation times

• Slow start-ups

Industry consolidation could help25

30

35

40

45

2010 2012 2014 2016 2018 2020

3.8 mill. tons of exits

required between 2017-21 There is substantial new capacity in the pipeline !

Demand

Supply

COPYRIGHT©PÖYRYSEPTEMBER 2016

FIBRIA INVESTOR TOUR 2016

“How to create long-lasting

shareholder value?”5

COPYRIGHT©PÖYRY

0 5.000 10.000 0 5.000 10.000 15.000

THE BEST PROTECTION TO PRICE EROSION

IS COMPETITIVENESS AND INVESTMENT DISCIPLINE

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

Financial health, competitiveness and the pacing of investments determine the

ability of the industry to create shareholder value

Illustrative only

Cumulative capacity, 1000 t/a

USD / t

Cash Costs

Capital Costs

Value Creation

Value destruction !Price Level

475

COPYRIGHT©PÖYRYSEPTEMBER 2016

FIBRIA INVESTOR TOUR 2016

Pulp

Seller

Pulp

Buyer

Is it only about price ?

COPYRIGHT©PÖYRY

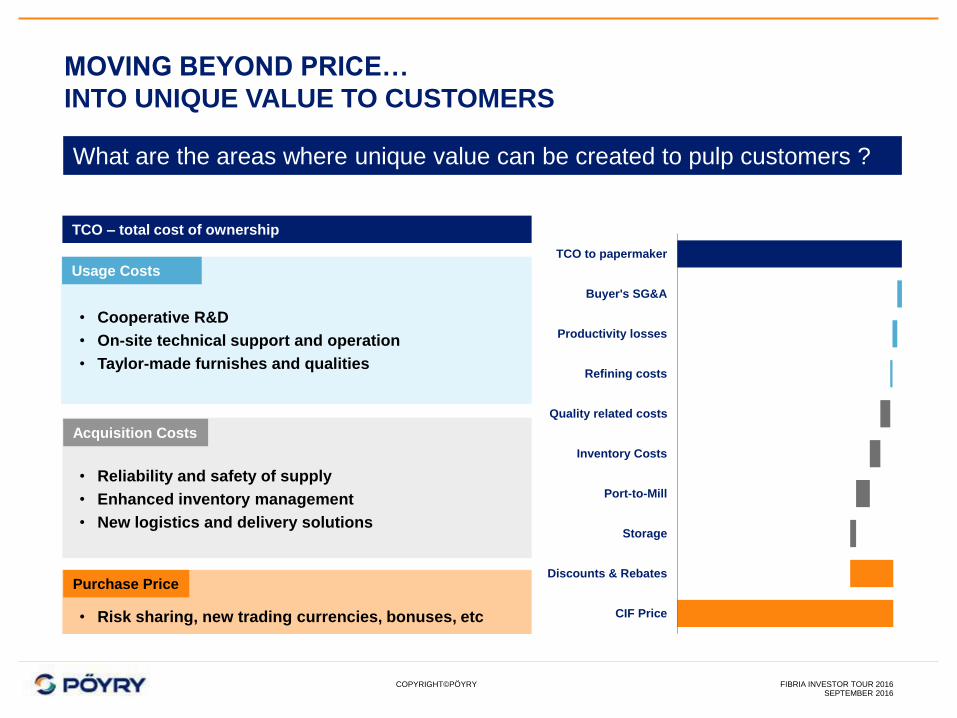

MOVING BEYOND PRICE…

INTO UNIQUE VALUE TO CUSTOMERS

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

0 200 400 600

CIF Price

Discounts & Rebates

Storage

Port-to-Mill

Inventory Costs

Quality related costs

Refining costs

Productivity losses

Buyer's SG&A

TCO to papermaker

Purchase Price

• Cooperative R&D

• On-site technical support and operation

• Taylor-made furnishes and qualities

What are the areas where unique value can be created to pulp customers ?

• Reliability and safety of supply

• Enhanced inventory management

• New logistics and delivery solutions

Usage Costs

Acquisition Costs

TCO – total cost of ownership

• Risk sharing, new trading currencies, bonuses, etc

COPYRIGHT©PÖYRYSEPTEMBER 2016

FIBRIA INVESTOR TOUR 2016

TO BEAT THE MARKETS

Differentiate1

2 Consolidate

Innovate3

COPYRIGHT©PÖYRY

DISCLAIMER AND RIGHTS

This presentation material has been prepared by Pöyry Management Consulting Oy (“Pöyry”) for Fibria S.A. All other use is strictly prohibited and

no other person or entity is permitted to use this presentation, unless otherwise agreed in writing by Pöyry. By accepting delivery of this

presentation material, the Recipient acknowledges and agrees to the terms of this disclaimer.

NOTHING IN THIS REPORT IS OR SHALL BE RELIED UPON AS A PROMISE OR REPRESENTATION OF FUTURE EVENTS OR RESULTS.

PÖYRY HAS PREPARED THIS REPORT BASED ON INFORMATION AVAILABLE TO IT AT THE TIME OF ITS PREPARATION AND HAS NO

DUTY TO UPDATE THIS REPORT.

Pöyry makes no representation or warranty, expressed or implied, as to the accuracy or completeness of the information provided in this report or

any other representation or warranty whatsoever concerning this report. This report is partly based on information that is not within Pöyry’s

control. Statements in this report involving estimates are subject to change and actual amounts may differ materially from those described in this

report depending on a variety of factors. Pöyry hereby expressly disclaims any and all liability based, in whole or in part, on any inaccurate or

incomplete information given to Pöyry or arising out of the negligence, errors or omissions of Pöyry or any of its officers, directors, employees or

agents. Recipients' use of this report and any of the estimates contained herein shall be at Recipients' sole risk.

Pöyry expressly disclaims any and all liability arising out of or relating to the use of this report except to the extent that a court of competent

jurisdiction shall have determined by final judgment (not subject to further appeal) that any such liability is the result of the willful misconduct or

gross negligence of Pöyry. Pöyry also hereby disclaims any and all liability for special, economic, incidental, punitive, indirect, or consequential

damages. Under no circumstances shall Pöyry have any liability relating to the use of this report in excess of the fees actually received

by Pöyry for the preparation of this report.

All information contained in this report is confidential and intended for the exclusive use of the Recipient. The Recipient may transmit the

information contained in this report to its directors, officers, employees or professional advisors provided that such individuals are informed by the

Recipient of the confidential nature of this report. All other use is strictly prohibited.

All rights (including copyrights) are reserved to Pöyry. No part of this report may be reproduced in any form or by any means without prior

permission in writing from Pöyry. Any such permitted use or reproduction is expressly conditioned on the continued applicability of each of the

terms and limitations contained in this disclaimer.

SEPTEMBER 2016FIBRIA INVESTOR TOUR 2016

Sustainability – Risks and Opportunities for the Pulp and Paper Sector

Rod Taylor

WWF International

Fibria Investors Forum

September, 2016

© A

dri

ana

Gam

bar

ini/

WW

F-B

razi

l

Forests for Life

Overview

1. A global perspective

2. Deep dive on Asia

3. Market signals and opportunities for leadership

Sustainability – Risks and Opportunities for the Pulp and Paper Sector

Forests for Life

Overview

1. A global perspective

2. Deep dive on Asia Market signals

3. Market signals and opportunities for leadership

Unsustainable

forestry

Market Transformation in the pulp and paper sector

Well-managed

forests or

plantations

Recycled Fibre

High GHG

emissions

High Water

Pollution

Waste to

landfill

Zero Water

Pollution

Zero

Waste

Low GHG

emissions

Powered by

renewables

Unsustainable Best Practice

WWF Projections

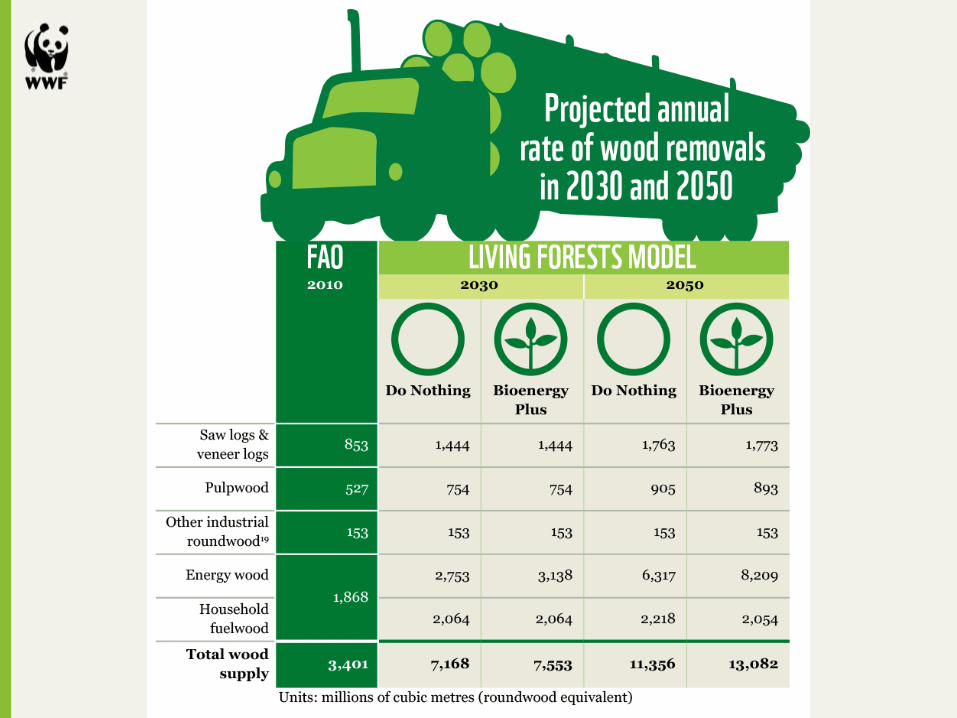

www.panda.org/livingforests

Between 2010 and 2050 –

Increased population and wealth will

demand volume of annual wood removals to

increase 3x, while producing 70% more

food

240 to 300 million additional hectares of

natural forest managed for commercial

harvesting

Around 250 million hectares of new

plantations

Produce more with LESS land, LESS water,

and LESS pollution, while maximizing

efficiency, and minimizing raw-material

inputs

Projected expansion in forestry plantations 2010 to 2050

Living Forests Report

Projected expansion

in forestry plantations

between 2010 and 2050

(millions of hectares)

The big squeeze

Farmland

Plantation Other ecosystems

Unlogged forest

Logged forest

Land use between now and

2050.

Each segment

represents a current

land use or a

natural state

(not to scale)

The big squeeze

Land use between now and

2050. High greenhouse

gas emissions

Huge decline

in biodiversity

Commodities impacting WWF priority places

Risks related to sustainability span

the whole supply chain

Deforestation pressures

Using more wood could be good for the planet…

Using low footprint materials

Wood is renewable, biodegradable and nature

does the engineering and synthesis, often resulting

in a lower footprint than materials made through

heavy industrial processes.

Tennis Racket: made with carbon fibre

produced from wood-based precursor

Sponge: separates oil from water, made by

“silyated” nanocellulose

Furniture: built with MDF and MDP using

wood based resins.

Body armour: High-strength yet lightweight using nanocellulose

Textiles: wood pulp and recycled material

Medicine: prepared with nanocellulose for controlled release of drugs in the body drugs controlled released

New wood-based materials and the bio-economy

Efficiency in the forest

Improved management practices in natural forests and plantations enable more wood

extraction with less social and environmental impact.

© W

WF-C

ano

n / D

ado

Gald

ieri

Bio-technology (including GMOs)

For

Against

More efficient processing and recycling can help reduce

pressure to extract more wood from forests

Good for the planet:

seven possible lives

Wasted opportunity:

life and death

virgin

fibre

More equitable consumption patterns

© K

jell-Arn

e Larsson

/ WW

F

The affluent reduce wasteful paper use so the poor can consume more for education,

hygiene and food safety.

Forests for Life

Overview

1. A global perspective

2. Deep dive on Asia

3. Market signals and opportunities for leadership

Indonesia - Draining rainforests on deep peatlands

Southeast Asia - Fire and Haze

Fires in Sumatra

Source: WWF-Singapore

Fires in Indonesia & Haze Much Beyond

Haze across the Straits in Singapore

APP products being pulled off Singapore retailers’

shelves in protest over links to haze from Sumatra

NTUC FairPrice staff removing Asia Pulp & Paper Group-related products from shelves at a Nex shopping mall outlet on Oct 7, 2015.

Photo: Lim Yaohui For The Straits Times

Impacts: Burnt peat, natural forests and plantations; health

and livelihoods; reduced farm yields; GHG emissions.

Deforestation in Sumatra

1985

Forest Deforestation

1990 2000 2008/2009

Historical forest loss and location of

pulp mills in Sumatra

Source: WWF Indonesia

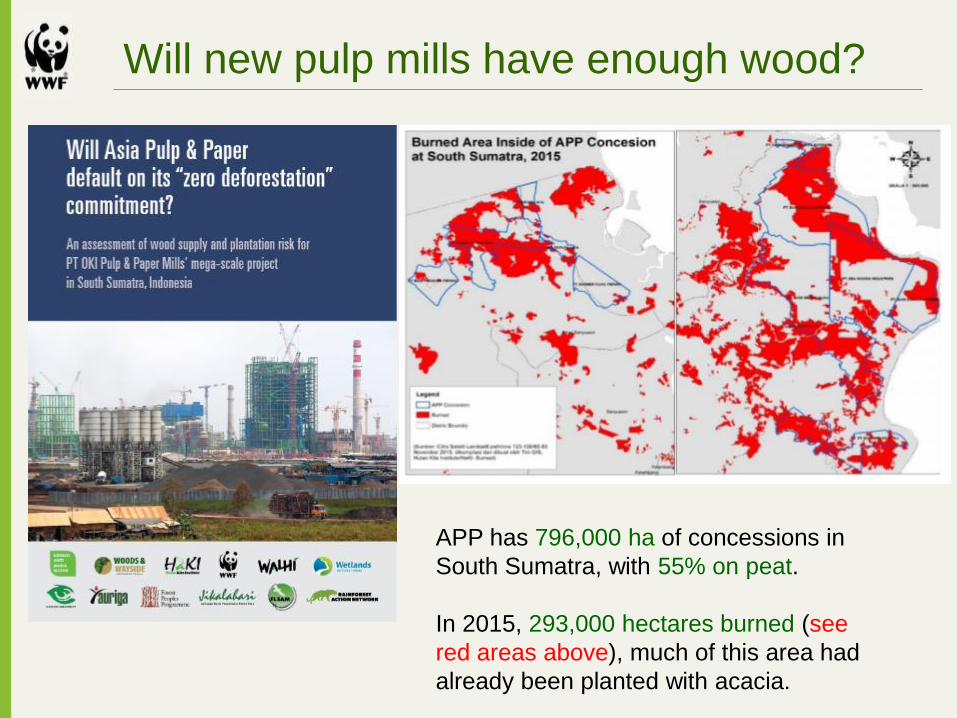

Will new pulp mills have enough wood?

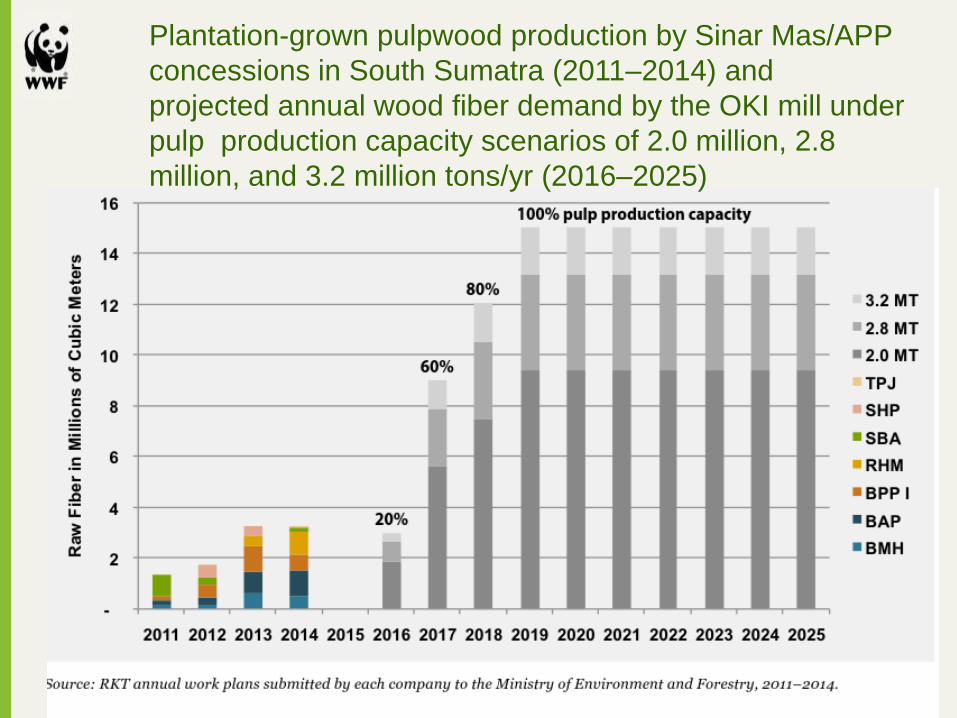

APP has 796,000 ha of concessions in

South Sumatra, with 55% on peat.

In 2015, 293,000 hectares burned (see

red areas above), much of this area had

already been planted with acacia.

Sinar Mas/APP supplier concessions in South Sumatra

Plantation-grown pulpwood production by Sinar Mas/APP

concessions in South Sumatra (2011–2014) and

projected annual wood fiber demand by the OKI mill under

pulp production capacity scenarios of 2.0 million, 2.8

million, and 3.2 million tons/yr (2016–2025)

Sinar Mas/APP concessions overlaid onto fire risk map

of South Sumatra Forestry Department

Provincial Forestry DepartmentMas/APP supplier

concessions in South Sumatra

Forests for Life

Overview

1. A global perspective

2. Deep dive on Asia

3. Market signals and opportunities for leadership

The Sustainable Development Goals

Issue

LEGAL

PRODUCTION

OCC. HEALTH &

SAFETY

LABOUR RIGHTS

WATER

MANAGEMENT

Commercial implications

• Operating licenses revoked or concessions repossessed;

• Risk of customer and consumer boycotts

• Incidents can affect profitability in ways including stoppages;

• A poor reputation makes it harder to attract workers

• A poor reputation makes it harder to attract workers;

• Unrest can lead to production stoppages;

• Well treated workforce is more productive and turnover is lower

• Bad water management can affect ability to transport products;

• It also can reduce water availability on long-term

• Mills: Bad water management can reduce water availability;

Pollution can cause communities’ protests: reputational risk,

risk of operational stoppage and license being revoked

Organizations sourcing forestry products: Lack of sustainability

can mean higher costs, and higher price volatility on the long-term

Impact on

cashflow/Bal S

Commercial case for action on sustainability issues in forestry

Revenue Yield Value of collateralOperating costs Closure of

business

More and more brands and retailers are

committing to deforestation-free sourcing

Commitment by 11 companies to

increase demand and supply of certified

and recycled paper products, particularly

FSC certified products

Objectives are to:

• Increase demand and supply of certified

and recycled paper products,

particularly FSC certified products

• Eliminate illegal and controversial

sources in the supply chain

• Increase supply chain transparency

Pre-competitive platform for paper buyers:

• Established in 2013• 5 companies and WWF-Japan

Objectives:

• Eliminating illegal and controversial sources in the supply chain• Increase demand and supply of certified and recycled paper products,

particularly FSC certified products• Encourage suppliers to understand and support responsible procurement

Consortium for Sustainable Paper Use - Japan

• Impacts on forest ecosystems from fibre sourcing

• Emissions from manufacturing processes such as water pollution and

greenhouse gas emissions

• Reporting and Environmental Management System

See results of EPCI 2015 at http://epci.panda.org/

WWF Environmental Paper Company Index

For more information,

please visit:

panda.org/livingforests

Obrigado

Estratégia e Novos Negócios

MANUTENÇÃO DA

RENTABILIDADECRESCIMENTO

COM DISCIPLINADIVERSIFICAÇÃO

COM FOCO

Principais tendências no Setor de Papel e Celulose

Demanda não é uma preocupação. Papéis sanitários, embalagens e a China lideram o crescimento sólido que vislumbramos para o futuro.

A fragmentação do setor leva à indisciplina nos investimentos.

O acesso a recursos de madeira é fundamental para a competitividade. A América do Sul continuará sendo o principal provedor de novos volumes de celulose no futuro próximo.

O aumento nos custos e a valorização monetária oferecem riscos à rentabilidade.

Impacto crescente da sustentabilidade. Oportunidades e ameaças devido à crescente pressão por soluções.

RENTABILIDADE

CRESCIMENTO

DIVERSIFICAÇÃO

Excelência Operacional

Disciplina Financeira

Governança Sólida

Sustentabilidade

Transparência

Cultura de Alto Desempenho

Ambiente Organizacional

Opções

IMEDIATO CURTO PRAZO MÉDIO PRAZO LONGO PRAZO

A estratégia da Fibria

Excelência Operacional

Modernização

Biotecnologia

Formação da Base Florestal

Crescimento Orgânico

Consolidação

Bio Estratégia

Logística

Imobiliário

Ativamente e preferencialmente buscar a consolidação com o objetivo de criar um setor mais saudável.

Continuar com a promoção de crescimento por meio de expansões e parcerias de forma disciplinada.

Manter a formação ativade florestas para estarmos prontos para oportunidades de crescimento.

Consolidar nossa posição entre os 10% dos participantes do mercado com menor custo

caixa no setor ao:

• Alcançar IMACEL de15.0 toneladas/ha/ano de celulose até 2025 para novas florestas plantadas.

• Tentar obter um mínimo de 10% de volume de

celulose diferenciadaprecificado com prêmio.

Diversificar seu fluxo de caixa por meio de investimentos focados em outros negócios que não a celulose, alavancando os ativos chave e as competências da Fibria.

Alcançar um fluxo de caixa livre mensurável de novos negócios em comparação ao negócio de celulose.

Principais Aspirações

RENTABILIDADE CRESCIMENTO DIVERSIFICAÇÃO

Complementar ànossa

cadeia de valor

Alavancagem emnossas

competências

Estabelecimento de parcerias

comprovedores de

tecnologiasvencedores

Inovação aplicada como objetivo final

Processo “Stage &

Gate”

Criação deFlexibilidadeEstratégica

DIVERSIFICAÇÃO FOCADA

Diversificação: Princípios da Bioestratégia

Rentabilidade: Desenvolvimento de Produto

Parte da Estratégia Comercial da Fibria

Para oferecer serviços e produtos (celulose) diferenciados e/ou customizados em engenharia de aplicação que gerem valor na cadeia “global”

Idade

Densidade

Material Genético

FLORESTAFÁBRICA

CLIENTE Cozimento

Branqueamento

Aditivos Refinamento

Co-refinamento

Mistura personalizada de insumos (furnish)

ALAVANCAS DE GERAÇÃO DE VALOR:

Custo Reduzido

Desempenho de Produto

Sustentabilidade Geral do Produto

CONSUMIDOR FINAL

Celulose totalmente livre de cloro desenvolvida para atender à

necessidade do mercado

Exemplo de Produtos Desenvolvidos - TCF

Idealização com o uso de várias tecnologias em uso na Fibria:

‣ 3 diferentes regiões no Brasil

‣ 6 tecnologias de cozimento

‣ 8 linhas de branqueamento combinando diferentes estágios.

Tempo entre a introdução do desafio e a entrega do produto: <1 ano

TRÊS LAGOAS - Mato Grosso do Sul 1,3 milhões t/ano

ARACRUZ - Espírito Santo2,3 milhões t/ano

JACAREÍ - São Paulo 1,1 milhões t/ano

VERACEL - Bahia

1,1 milhões t/ano (50% da produção)

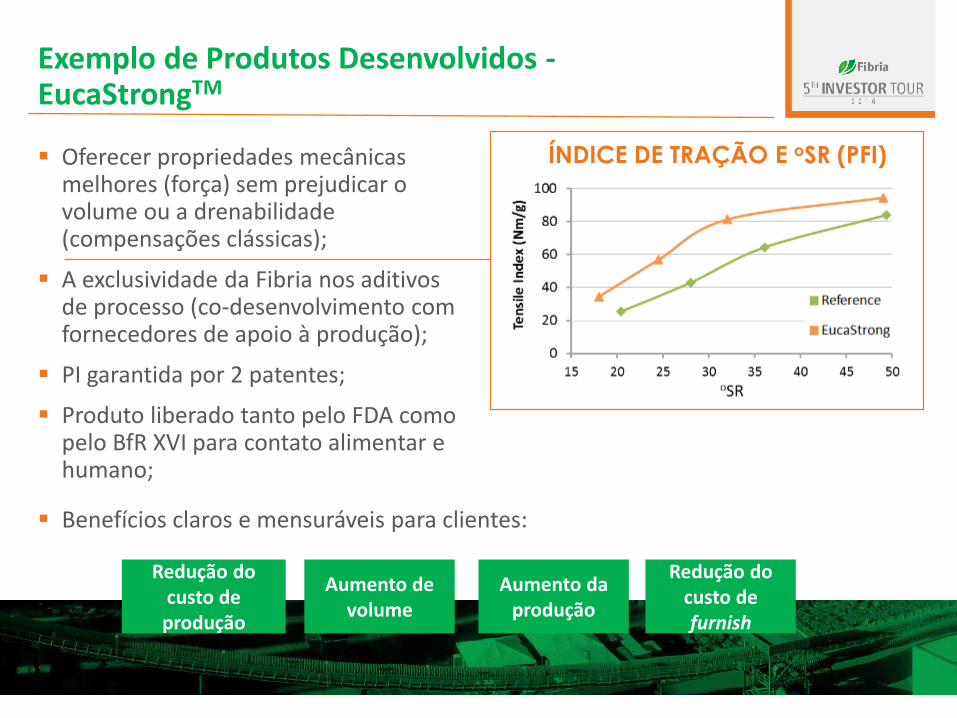

Exemplo de Produtos Desenvolvidos -EucaStrongTM

Oferecer propriedades mecânicas melhores (força) sem prejudicar o volume ou a drenabilidade (compensações clássicas);

A exclusividade da Fibria nos aditivos de processo (co-desenvolvimento com fornecedores de apoio à produção);

PI garantida por 2 patentes;

Produto liberado tanto pelo FDA como pelo BfR XVI para contato alimentar e humano;

Aumento da produção

Redução do custo de furnish

Aumento de volume

Redução do custo de produção

ÍNDICE DE TRAÇÃO E oSR (PFI)

Benefícios claros e mensuráveis para clientes:

Caminhos da tecnologia priorizados por maturidade e atratividade econômica

PIRÓLISE

LIGNINA

NANO-CELULOSE

BIOCOMPÓSITOS

Caminhos Priorizados

Fonte: Projeto de Bio-Estratégia da Fibria

Mat

uri

dad

e Te

cno

lógi

ca

Atratividade Econômica

Prioridade 1

Prioridade 2

TamanhoRelativo do Mercado

Tecnologia A

Tecnologia B

Tecnologia E

Tecnologia F

Tecnologia C

Tecnologia D

Status de desenvolvimento de diferentes caminhos tecnológicos de bioestratégia

Roadmap definido em 2012

Atualizado e executado de maneira disciplinada

Identificação de possíveis parceiros de tecnologia

Relações estratégicas no

local

Investimentos piloto

Identificação de

tecnologias promissoras

Negociação com parceiros de tecnologia selecionados

Investimentos comerciais

PIRÓLISE

LIGNINA

NANO-CELULOSE

BIOCOMPÓSITOS

ESTÁ

GIO

DE

DES

ENV

OLV

IMEN

TO

Vários parceiros já colaboram

Váriosparceiros já colaboram

Investigação em andamento

Negociaçõesem andamento

Flexibilidade no usode matérias primas

Tecnologia comercialmente

comprovadaProduto

Renovável

Negócio de Pirólise com base na plataforma de tecnologia RTP da Ensyn

Biomassa entregue

na planta

Biomassa convertida em bio-

óleo na planta de RTP

Bio-óleo entregue

aos clientes

MATÉRIA PRIMA PROCESSO DE RTP ÓLEO COMBUSTÍVEL

SUBSTITUTO

Flexibilidade do mercado consumidor

MERCADOS CONSUMIDORES

Aquecimento e

Resfriamento

Co-processamento na

Refinaria

Ingredientes Alimentares e

Produtos Químicos Renováveis

Já

comercial

O co-processamento é uma das poucas opções de compliance para que refinadores atendam a requisitos regulatórios

O co-processamento é a solução de compliance com o menor custo para refinadores, permitindo que economizem milhões de dólares em compliance por ano

• Venda de bio-óleo para refinarias - com base em seu desempenho em comparação ao petróleo

• Monetização de créditos no âmbito do Programa RFS2

• O preço dos créditos varia de maneira inversa em relação ao preço do petróleo

• Monetização de créditos gerada por refinarias californianas no âmbito do Programa LCFS

• Monetização de créditos gerada por refinarias californianas no âmbito do Programa de Comércio de Emissões de Carbono

RECEITA DE BIO-ÓLEO RECEITA DE RIN RECEITA DE LCFS RECEITA DE COMÉRCIO

DE EMISSÕES

ProduçãoUnidade de

petróleo

CraqueamentoCatalítico Fluido

(FCC)DistribuiçãoDistribuição Vendas no varejo

Diesel / Gasoline

Diesel / Gasoline

Biocombustível misturadoBio-Óleo

Bio-Óleo

Petróleo

97% 3%

VGO Biocrude

O mercado de Refinarias de Craqueamento Catalítico Fluido (FCC) dos EUA é de 5,6 milhões bpd e pouco explorado

O mercado de refinarias dos EUA oferece uma significativa oportunidade de demanda de mercado

A atual capacidade diária de FCC do mercado dos EUA é de 5,6 milhões de barris

Uma taxa de mistura conservadora de 3% exigiria 170.000 bpd ou 2,6 bilhões gpy de bio-óleo

Não existem concorrentes comercialmente fornecendo bio-óleo para o mercado de FCC em refinarias

Capacidade de Óleo Combustível Renovável (RFO) para Fornecimento de 3%

do Mercado de FCC dos EUA

Refinaria dos EUA Capacidade de FCC

5,6M bpd

85,8B gpy

170.000 bpd

2,6B gpyFontes: Oil and Gas Journal, RFA

130 unidades de RTP da

Aracruz

A Fibria e a Ensyn criaram uma JV no Brasil com a tecnologia RTP

Fonte: Análise da Equipe Estratégica da Fibria

VANTAGEM DO CUSTO DA CARGA

Potencial para utilizar a área de um milhão de ha da Fibria para o fornecimento de resíduos florestais

Possíveis parceiros nos setores de florestas, agricultura e serraria

Alavancagem do conhecimento da Fibria em operações de logística florestal

Acesso à tecnologia de pirólise da Ensyn, protegida por uma robusta PI

Acesso atual a mercados consumidores na América do Norte e no Brasil

Conhecimento sobre o ambiente regulatório nos EUA

EXCELÊNCIA EM LOGÍSTICA DE BIOMASSA

ACESSO À TECNOLOGIA

ACESSO AO MERCADO

Destaques do Projeto de RTP

FLEXIBILIDADE COMERCIAL

Cenário Base: exportação para os EUA para co-processamento

Cenário Alternativo: exportação para os EUA para aquecimento

Cenário Desfavorável: uso interno – substituto do GN

POTENCIAL LOCALIZAÇÃO

FAVORÁVEL

Sinergias com a localização da Fibria‣ Integração operacional‣ Utilização dos resíduos florestais

disponíveis‣ Alternativas logísticas identificadas

SITUAÇÃO FINANCEIRA

SÓLIDA

TEMPO DE COLOCAÇÃO

NO MERCADO

Implementação em 24 meses a partir da data de aprovação

Sólida situação financeira mesmo em cenários de variação cambial desfavoráveis

Baixa volatilidade com correlação negativa: preços do petróleo e benefícios regulatórios

Disponibilidade de financiamento de baixo custo

STATUS

Engenharia básica terminada

Contratos de compra e venda em negociação

com as refinarias americanas

Necessidade de aprovação pelos conselhos da

Fibria e da Ensyn

Vídeo - RTPRecebimento e fragmentação

da madeira

Silo de biomassa

E-houseSala de

Controle -Armazém

Filtragem

Moagem e Triagem

SecadoraMáquinas de

Gás

Silo de Biomassa Seca

RTP Torre de Resfriame

nto

Armazenamento de

RFO

Atualmente a lignina é queimada como combustível

Potencial para a aplicação da lignina a outros usos de

valor agregado

25%-30% DA

COMPOSIÇÃO TÍPICA EM ÁRVORES DE EUCALIPTO

QUEIMADA PARA PRODUZIR ENERGIA

PRODUTOS DE VALOR AGREGADO

Agregando valor com o desenvolvimento do negócio de lignina

LIGNINA

Laboratórios totalmente equipados

Planta piloto no processo Organosolv

20 famílias de patentes existentes

85 patentes

Mais de 10 anos de dados de pesquisa

10 funcionários em tempo integral

Integração total com o Centro de Tecnologia no Brasil(kraft + Organosolv)

Recursos Humanos Portfólio de Pesquisa e Patente Equipamento

Fibria InnovationsBritish Columbia, Canadá

A aquisição da Lignol em 2014acelera o tempo de colocação no mercado

CommodityPetroquímica

Fricção

Reforçando oPreenchimento para Borracha

Isolamento

FundiçãoMoldagem deCompostos

Produtos deMadeira

Adesivos

MateriaisCompostos

Filmes

RevestimentosFibra de Carbono

O portfólio de lignina da Fibria permite o desenvolvimento de diferentes aplicações

Desenvolvimento de Possíveis AplicaçõesFibria Innovations + Parceiros

Lignina Kraft Lignina Organosolv

Mercado de Nicho

Valor da Lignina

Fibra de Carbono

Vanilina

Resina FF

Carbono Negro

Epóxi

Aditivos de Cimento

Biocombustível

Resina de PU

FenolLigno-sulfonatos

Lignina de Baixa Pureza

BTX

Polímeros

Os processos Kraft e Organosolv possuem características diferentes que os tornam mais adequados a diferentes aplicações

Mercado de Commodities

Energia

Volume

Esta diversidade permite que a Fibria atue em diferentes mercados

Organosolv

Kraft

VISÃO GERAL

Fonte: RISI Relatório “NANOCELLULOSE: Technology, Applications and Markets” 2014; Poyry

Desenvolvimento de Negócio de Nano-celulose

NANO FILAMENTOSFIBRILASFIBRA

PROPRIEDADES

RESISTENTE

LEVE

ALTAMENTE ABSORVENTE

MUDANÇAS REOLÓGICAS

BIODEGRADÁVEL

RENOVÁVEL

Possível criação de valor com clientes em setores novos e já existentes

Licenciamento de Tecnologia

Produtores Externos

FIBRIA Jacarei Aracruz 3L

Cadeias de valor atuais ou

contíguas

Novas cadeias de valor

Petróleo e Gás

Tintas

Papel Especial

Embalagem

Higiene

Compósitos

Cimento

SETOR

As características da Fibria permitem que a companhia

tenha um papel de ligação na cadeia de valor

Em definiçãoLicenciamento

Aquisição e construção de uma planta piloto de 2 t/dia

Início das operações no 1T17

Desenvolvimento em curso das aplicações R$ em papéis sanitários, papel de escrever e para impressão (P&W) e outros

CNCCNF

PARCEIROS

STATUS

RELACIONAMENTO

O posicionamento da Fibria em nano-celulose

Negociações em Andamento

VISÃO DE LONGO PRAZOAMBICIOSA

PLANO DE AÇÃO PRUDENTE, FOCADO E DISCIPLINADO EM

EXECUÇÃO

Principais conclusões sobre a bio-estratégia da Fibria

Complementar ànossa

cadeia de valor

Alavancagem em

nossascompetências

Estabelecimento

de parcerias

com provedores

de tecnologiasvencedores

Inovação aplicada como objetivo final

Processo “Stage &

Gate”

Criação de

FlexibilidadeEstratégica

DIVERSIFICAÇÃO FOCADA

Projeto Horizonte 2

Visão Geral do Local

R$ 2,5 bilhõesde execução financeira

(32%)

53,7%do total terminado

140trabalhadores diretos contratados para as

operações (800 esperados

até Dez/16)

6.000trabalhadores no local

(pico de 8.000 a 10.000 em Dez/16)

7.000.000 de horas

trabalhadas

Atualização de Capex do Horizonte 2

1,80 1,71

0,650,48

0,05

0,11

2,52,3

Original Revisado

R$ EUR US$ e outros

72%

26%

2%

77%

19%

4%

CAPEX (US$ bilhões)(1)

3%

55%

39%

4%

2015 2016 2017 2018

Capex Total em reais: R$ 7,7 bilhões

Cronograma atual

DESAFIOSBENEFÍCIOS

A consolidação traz desafios, mas os benefícios são indiscutíveis

Motivação estratégica

Momento da outra parte

Avaliação relativa

Governança Corporativa

Possibilidade de grande sinergia

Consolidação de mercado e do portfólio de clientes

Racionalização do pipeline de novos projetos

O CRESCIMENTO A PARTIR DA CONSOLIDAÇÃO É UM FATOR CHAVE DE INCENTIVO À CRIAÇÃO DE VALOR

868

535

236301

542

853711

556

61

291

633

32

Liquidez 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

PPE BNDES

NCE ACC/ACE

Voto IV Bonds

Finnvera CRA and Outros

Caixa(1)

Revolver

1,403

Outras atualizações importantes– Liquidez

0,4

2,3

0,2

0,7

0,3

0,2

0,2

0,2

Pré-Pgto Exportação CRA BNDES FDCO ECA Working capitalrelease (2)

Total

0,2 - 2S16

3T153T15

.

0,1 - 2S160,2 - 20170,2 - 2S16

0,5 - 2017

0,2 - 2017

0,1

Capex H2 (2):

(2) Liberação decorrente do contrato de Klabin e fornecedores

Financiamento do Projeto Horizonte 2 (US$ bilhões)

(1) Não inclui US$30 milhões relativos ao MtM de operações de hedge. | (2) Execução financeira do Capex de US$747 milhões até 31 de agosto de 2016 | (3) Considerando R$/US$ em 15/set/16 = 3.3326.

Recursos sacados até 15/set/2016. Recursos contratados a sacar

82901

Liquidez(1) e Cronograma de Amortização da Dívida(3) em 15 de setembro de 2016 (US$ milhões)

524

CHALLENGESBENEFITS

Outras atualizações importantes – Suprimento de Madeira(1)

788

Mad

eira

de

Terc

eiro

s(%

)

0

50

100

150

200

250

300

350

400

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Distância média da floresta para a fábrica Madeira de Terceiros

Aumento na previsão de madeira de terceiros devido ao baixo nível de chuvas na região da Unidade Aracruze otimização da base florestal de Três Lagoas

A distância média vai cair drasticamente gerando uma redução de Opex

(1) Não inclui Veracel, mas considera a base florestal de H2 | (2) Taxa de câmbio R$/USD: 3,33.

Distân

ciam

edia d

a floresta

para a Fáb

rica(km

)

68%34% 63% 73% 67% 75% 67%% Plantado

VPL de pico a nível normalizado(2):CAPEX: R$1,3 bilhões (US$ 0,4 milhão) | OPEX: R$0,9 bilhão (USD 0,3 milhão)

VPL Total : R$2,2 Bi ou US$ 0,7 Bi