lupatech registra lucro lÍquido de r$15,4 milhÕes …lupatech.infoinvest.com.br/ptb/1394/lupa3 er...

TRANSCRIPT

1

LUPATECH REGISTRA LUCRO LÍQUIDO DE

R$15,4 MILHÕES EM 2009

Caxias do Sul, 29 de março de 2010 - A Lupatech S.A. (BM&FBovespa: LUPA3) (OTCQX:

LUPAY) (“Lupatech” ou “Companhia”), líder no Mercosul na fabricação de válvulas industriais e

fabricante de equipamentos para o setor de petróleo e gás e de conjuntos para a cadeia

automotiva, anuncia o resultado do quarto trimestre de 2009 (4T09) e do exercício de 2009. As

informações trimestrais e demonstrações financeiras consolidadas anuais da Companhia são

elaboradas de acordo com as normas internacionais de relatório financeiro – IFRS

(International Financial Reporting Standard). As comparações apresentadas, exceto quando

indicado o contrário, referem-se aos números verificados no terceiro trimestre de 2009 (3T09) e

exercício fiscal de 2008.

TELECONFERÊNCIAS PARA APRESENTAÇÃO DOS RESULTADOS DO 4T09

INGLÊS – INVESTIDORES ASIÁTICOS

Data: 30 de março de 2010Horário: 22:30h (Brasília) /09:30h (HKT) do dia 31/03Telefone: +1 412 858 4600Código: Lupatech

PORTUGUÊS

Data: 31 de março de 2010Horário: 10:00h (Brasília) /09:00h (US-ET)Telefone: +55 11 2188-0188Código: Lupatech

INGLÊS

Data: 31 de março de 2010Horário: 12:00h (Brasília) /11:00h (US-ET)Telefone: +1 412 858 4600Código: Lupatech

RELAÇÕES COM INVESTIDORES - CONTATOS

Thiago Alonso de Oliveira - CFO & IROCynthia Burin - Gerente de RI

Telefone: + 55 (11) 2134-7000 ou + 55 (11) 2134-7088Email: [email protected] : www.twitter.com/LUPA3Blog : www.lupatech.com.br/blog

Assessoria de Imprensa: MZ Consult +55 11 3529-3800

2

PRINCIPAIS INDICADORES:

Lupatech S.A. - Dados Consolidados em R$ mil

Indicadores Financeiros 3T09 4T09 Var % 2008 2009 Var %

Receita Líquida 128.230 107.818 -15,9% 704.673 555.162 -21,2%

Energy Products 85.634 66.670 -22,1% 450.934 386.404 -14,3%

Flow Control 29.623 28.034 -5,4% 164.203 117.080 -28,7%

Metalurgia 12.972 13.114 1,1% 89.535 51.678 -42,3%

Lucro Bruto 28.547 22.619 -20,8% 286.637 152.166 -46,9%Margem 22,3% 21,0% 40,7% 27,4%

Energy Products 15.600 11.555 -25,9% 192.956 104.291 -46,0%Margem 18,2% 17,3% 42,8% 27,0%

Flow Control 13.371 11.188 -16,3% 78.055 48.935 -37,3%Margem 45,1% 39,9% 47,5% 41,8%

Metalurgia (425) (124) -70,8% 15.626 (1.059) -106,8%Margem -3,3% -0,9% 17,5% -2,0%

EBITDA 11.606 6.925 -40,3% 209.708 81.572 -61,1%

Margem 9,1% 6,4% 29,8% 14,7%

Energy Products 4.267 1.313 -69,2% 144.667 54.621 -62,2%Margem 5,0% 2,0% 32,1% 14,1%

Flow Control 7.465 7.828 4,9% 55.809 30.332 -45,6%Margem 25,2% 27,9% 34,0% 25,9%

Metalurgia (126) (2.216) 1663,3% 9.232 (3.381) -136,6%Margem -1,0% -16,9% 10,3% -6,5%

Resultado Líquido 33.365 (47.072) -241,1% (29.530) 15.408 -152,2%Margem 26,0% -43,7% -4,2% 2,8%

Indicadores Operacionais 2008 2009 Var %

Capex Orgânico 124.928 54.014 -56,8%

Aquisições de investimentos 76.869 71.282 -7,3%

[O restante dessa página foi deixado intencionalmente em branco]

3

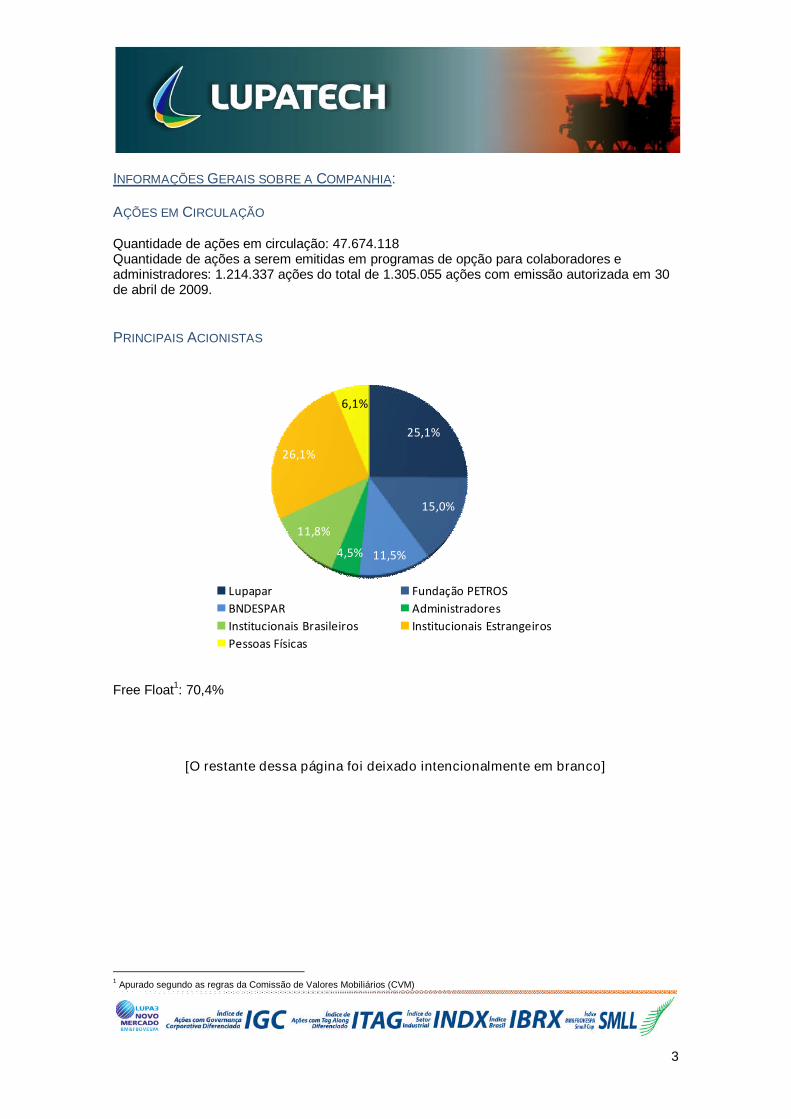

INFORMAÇÕES GERAIS SOBRE A COMPANHIA:

AÇÕES EM CIRCULAÇÃO

Quantidade de ações em circulação: 47.674.118Quantidade de ações a serem emitidas em programas de opção para colaboradores eadministradores: 1.214.337 ações do total de 1.305.055 ações com emissão autorizada em 30de abril de 2009.

PRINCIPAIS ACIONISTAS

Free Float1: 70,4%

[O restante dessa página foi deixado intencionalmente em branco]

1Apurado segundo as regras da Comissão de Valores Mobiliários (CVM)

25,1%

15,0%

11,5%4,5%

11,8%

26,1%

6,1%

Lupapar Fundação PETROS

BNDESPAR Administradores

Institucionais Brasileiros Institucionais Estrangeiros

Pessoas Físicas

4

Prezados Senhores,

A Administração da Lupatech S.A. (“Companhia”) apresenta o Relatório da Administração e asInformações Financeiras Anuais Consolidadas da Companhia referentes ao exercícioencerrado em 31 de dezembro de 2009 (2009).

Recomenda-se a leitura deste material em conjunto com as Notas Explicativas às InformaçõesFinanceiras Anuais Consolidadas.

PERFIL DA COMPANHIA E DESCRIÇÃO DOS NEGÓCIOS

A Lupatech S.A. possui três segmentos de negócios: Energy Products2, Flow Control

3e

Metalurgia4, e conta com aproximadamente 2.971 colaboradores.

O Segmento Energy Products oferece produtos de alto valor agregado e serviços para aindústria de petróleo e gás, como cabos para ancoragem de plataformas em águas profundas,válvulas, equipamentos para exploração de poços, revestimentos de tubos, compressores paraGNV, sensores e serviços, através das marcas “Lupatech MNA”, “Lupatech CSL”, “LupatechTecval”, “Lupatech Oil Tools”, “Lupatech Esferomatic”, “Lupatech Oil & Gas Services”,“Lupatech Tubular Services”, “Lupatech Monitoring Systems”, “Aspro”, “Sinergás” e“Norpatagonica”.

O Segmento Flow Control possui posição de liderança no Mercosul na produção ecomercialização de válvulas industriais, principalmente para as indústrias química,farmacêutica, papel e celulose e construção civil, através das marcas “Lupatech Valmicro”,“Lupatech Mipel”, “ValBol” e “Jefferson”.

O Segmento de Metalurgia ocupa posição de destaque no mercado internacional e éespecializado no desenvolvimento e na produção de peças, partes complexas e subconjuntosdirecionados principalmente para a indústria automotiva mundial através dos processos defundição de precisão e de injeção de aço, onde a Companhia é pioneira na América Latina.Opera ainda na fundição de peças em ligas metálicas com alta resistência a corrosão, voltadaspara os setores de válvulas industriais e bombas, principalmente para aplicações nosprocessos para a indústria de petróleo e gás, através das marcas “Microinox”, “Steelinject” e“Itasa”.

[O restante dessa página foi deixado intencionalmente em branco]

2Antigo Oil & Gas

3Antigo Flow

4Antigo Metal

5

MENSAGEM DA ADMINISTRAÇÃO AOS ACIONISTAS E AGENTES DO MERCADO DE CAPITAIS

Prezados acionistas e agentes do mercado de capitais,

Apresentamos os resultados da Lupatech S.A. para o exercício social de 2009.

O exercício de 2009 foi, sem dúvida, o mais difícil para os negócios da Companhia nos últimosdez anos, quando a demanda por nossos produtos foi fortemente impactada pela crisefinanceira mundial que teve início nos últimos meses de 2008.

Nossos negócios do Segmento Energy Products, voltados essencialmente para o mercadobrasileiro de petróleo e gás, foram impactados negativamente por atrasos na execução deinvestimentos discricionários traçados anteriormente para o setor, decorrentes da forte reduçãona oferta de fontes de financiamento de longo prazo e da queda generalizada do preço dopetróleo. No Segmento Flow Control, de válvulas industriais, também foi sentida retração dosnegócios, principalmente na Argentina. No Segmento Metalurgia, nossos negócios seressentiram da retração na demanda oriunda da cadeia automotiva no hemisfério norte. Aconsequência sentida foi queda da Receita Líquida da Companhia em 21,2% em 2009 quandocomparada a 2008.

Desde 2007 vínhamos num processo de expansão de capacidade de nossas unidadesindustriais, principalmente as voltadas para o Segmento Energy Products e a grande maioriadesses investimentos entrou em operação justamente em 2009. Apesar de operarem ao longodo ano com baixa utilização de capacidade, cerca de 35% do total disponível, acreditamos queessa nova capacidade permitirá a Lupatech atender mais e maiores projetos nos anos a frente,para quando é esperada a retomada da demanda.

No transcorrer do ano as condições macro-econômicas mundiais evoluíram e no encerramentodo exercício começamos a perceber melhoria na demanda. Nosso conforto advêm de diversosprocessos de licitação ou de tomada de preços que participamos através dos segmentosEnergy Products e Flow Control, cujos reflexos serão percebidos ao longo de 2010 e nos anosseguintes.

Durante o ano de 2009 iniciamos diversos projetos que visam melhorar o grau de integração erealização de sinergias nas 15 empresas que foram adquiridas nos últimos anos como parte donosso processo de diversificação de linhas de produtos e serviços. Entendemos que ao longode 2010 os primeiros efeitos positivos dessas medidas serão sentidos, principalmente naredução de custos fixos e de despesas administrativas e gerais. Dentre as principais medidasem curso estão a centralização de atividades industriais e a implantação do Centro de ServiçosCompartilhados Lupatech.

Abaixo destacamos os principais objetivos concluídos ao longo de 2009:

Joint Venture V&M: fornecimento de revestimento para tubos

Joint Venture Cameron: fabricação de compressores recíprocos

Fornecimento de válvulas e cabos de ancoragem para projetos da Petrobras como as

plataforma P-55, P-57 e Capixaba, refinarias como REPLAN, REPAR entre outras; e

Bloco 31 da British Petroleum (em Angola)

Conclusão da expansão das unidades Lupatech MNA, Lupatech Oil Services e

Lupatech Oil Tools.

Implantação do conceito de EVA na gestão dos negócios da Companhia

Nova estrutura de endividamento

6

Redução do capital de giro utilizado nas operações

Mesmo com o ambiente adverso para nossos negócios e após dois anos consecutivos deprejuízos, a Companhia apresentou Lucro Líquido de R$15,4 milhões (R$0,03 por lote de 100ações), evolução de R$44,9 milhões sobre o resultado que apresentamos em 2008.

VISÃO GERAL DOS SEGMENTOS DE NEGÓCIOS

SEGMENTO ENERGY PRODUCTS

O segmento Energy Products, conforme acima mencionado, vem observando importanteretomada dos projetos relacionados a produção de petróleo e gás no Brasil, que beneficiamdiretamente a Lupatech. A Companhia participou desde o final de 2009 de diversas cotaçõesrelacionadas a válvulas, serviços e revestimentos sendo vitoriosa em grande parte delas. Comisso, foi capaz de montar uma carteira de pedidos significativa para os próximos períodos.

A recuperação da demanda por projetos de produção no setor de petróleo e gás no Brasiliniciou-se primeiramente com projetos relacionados a manutenção, reposição e operação(MRO), e com prestação de serviços. Estes contratos caracterizam-se por serem de longoprazo (acima de um ano) e negociados diretamente com os clientes finais (petroleiras),trazendo boa previsibilidade de receita para a Companhia.

A demanda oriunda de novos projetos como plataformas, refinarias, etc., que se caracteriza porcontratos de curto prazo (até um ano) e negociados com EPCistas, começou a apresentarrecuperação, principalmente aqueles voltados para refinarias, sendo que os projetos deplataformas ainda apresentam baixo nível de atividade.

SEGMENTO FLOW CONTROL

O segmento Flow Control tem grande exposição à atividade industrial no Brasil e na Argentina.Com a recuperação econômica de grande parte dos setores da economia no Brasil, estesegmento tem observado não só crescente melhoria na atividade comercial como também nautilização de sua capacidade, o que refletirá em melhores índices operacionais durante oexercício de 2010.

SEGMENTO METALURGIA

O segmento Metalurgia tem grande exposição à cadeia automotiva. Ainda que tenha seobservado melhora no setor automotivo no Brasil, a demanda deste segmento para aCompanhia é direcionada para exportações para Europa e México (mercado americano),mercados onde este setor ainda não se recuperou ou apresentou sinais muito leves derecuperação.

[O restante dessa página foi deixado intencionalmente em branco]

7

ARGENTINA

A Companhia possui negócios na Argentina com exposição aos setores industriais,destacadamente o de petróleo e gás. Ainda que a melhora no cenário mundial tenha impactadotambém a Argentina, o país enfrenta outros problemas de caráter interno que nos leva aesperar que em 2010 o nível de atividade ainda seja modesto, dado a falta de incentivos parainvestimentos no país neste momento. A expectativa é que as unidades presentes naArgentina, com exceção do negócio de compressores de gás que apresentou considerávelrecuperação comercial no encerramento de 2009, devam trabalhar em patamares próximos a60% daqueles registrados no exercício de 2008.

PERSPECTIVAS PARA 2010

O ambiente macro-econômico para 2010 em diversos aspectos apresenta-se mais favorável doque o verificado em 2009, o que permite a Companhia trabalhar com a expectativa decrescimento da Receita Líquida, que deverá situar-se próxima à verificada em 2008.

A distribuição da Receita Líquida ao longo de 2010 terá maior concentração no segundosemestre, marcando a saída de um período de fraca demanda durante o primeiro semestrepara entrar num período mais robusto de demanda para nossos produtos e serviços.

Observamos desde outubro de 2009 recuperação na atividade comercial que já impactou econtinuará por impactar a carteira de pedidos da Companhia, contribuindo para receitasmaiores que as verificadas em 2009.

Eventuais impactos nas margens operacionais para 2010 estão associados aos progressos desinergias e reduções de custos e gastos fixos iniciados ainda em 2009. Entendemos ainda queexiste espaço para ganhos com a alavancagem operacional na medida em que a utilização dacapacidade ocupada cresça.

Em relação às perspectivas para 2011 em diante, a Companhia continua esperando fortecrescimento do setor de petróleo e gás especialmente no Brasil. A grande quantidade decampos de petróleo e gás que foram descobertos, traduzindo-se em reservas que necessitamser desenvolvidas, criarão ambiente extremamente favorável para os negócios da Lupatech.Há também novas reservas a serem exploradas e desenvolvidas assim como novos entrantesno mercado que poderão tornar-se clientes da Companhia.

COMPORTAMENTO DE MERCADO – CONCORRÊNCIA E CONTEÚDO LOCAL

A Companhia acompanha de perto a competição nos mercados onde atua, e onde observamaior atratividade para novos competidores é no mercado brasileiro de equipamentos eserviços para petróleo e gás, que cresce a taxas superiores aos demais mercados em queatua.

O market share dos nossos negócios mantiveram-se estáveis em 2009, ainda que a demandageral tenha caído. Temos observado condições de competição similares a de outros anos namaioria dos nossos negócios, exceto em válvulas, por serem produtos com menor barreiratecnológica e maior número de fornecedores. Embora esse seja o cenário, não percebemosalteração na participação de mercado em válvulas.

8

Para manter nossa posição de mercado, investimos constantemente em tecnologia, novaslinhas de produtos e redesenho de linhas de produtos, nos antecipando a possíveis demandasde mercado e melhor posicionando a Companhia. Temos também buscado oferecer soluçõesaos nossos clientes e não apenas produtos, agregando aos equipamentos que fornecemosserviços de instalação, manutenção e operação, entregando soluções customizadas, criandomais um diferencial competitivo em nossos mercados.

A tendência de crescimento da exigência mínima de Conteúdo Local no mercado brasileiro éuma realidade que promove nosso modelo de negócio. Somos uma Companhia quedesenvolve, produz e comercializa seus produtos e serviços com alto índice de ConteúdoLocal. Temos observado que as novas concessões licitadas pela Agência Nacional de Petróleo(ANP) têm apresentado percentuais mínimos de Conteúdo Local cada vez maiores, o que nosfaz acreditar que estamos bem posicionados para fornecer equipamentos que se adequam àsexigências mínimas de Conteúdo Local da ANP e das empresas produtoras de petróleo e gás,dadas a nossas competências industriais aliadas a capacidade instalada no Brasil.

JOINT VENTURES E PARCERIAS

Com o crescimento esperado para o setor de petróleo e gás no Brasil, tem crescido também ointeresse de outras empresas de entrarem neste mercado. Dado as peculiaridades do mercadobrasileiro e da exigência de Conteúdo Local mínimo, muitas delas tem como alternativa estaentrada através de parcerias estratégicas e joint ventures. A Lupatech é um parceiro naturalpara essas empresas, e temos sido procurados por algumas empresas que gostariam de sealiar à Lupatech para adentrarem no mercado brasileiro, permitindo à Companhia oferecer linhamais ampla de produtos e serviços.

Consideramos estas possíveis joint ventures e parcerias extremamente positivas para aCompanhia, que poderá em alguns casos acelerar o desenvolvimento tecnológico de produtos,acessar melhores fontes de matéria-prima assim como relacionamento comercial com novosclientes e mercados.

CRESCIMENTO DOS INVESTIMENTOS NO SETOR

A Lupatech tem seu posicionamento e estratégia focados no setor de petróleo e gás emdiversos mercados, mas com maior exposição ao mercado brasileiro onde o crescimentohistórico e projetado para os próximos anos vem crescendo a taxas anuais expressivas.Somente a Petrobras pretende investir nos próximos cinco anos entre US$200 bilhões eUS$220 bilhões, sendo que no decorrer de 2010 os investimentos deverão somar R$88,5bilhões.

Existe a expectativa no mercado de que a Petrobras receba uma capitalização. Em nossaavaliação, este movimento é positivo para todos os fornecedores da Petrobras, que terá maiorcapacidade de investimento bem como novas reservas a serem exploradas.

O mercado brasileiro, apesar de concentrado em Petrobras, vem mostrando evolução emtermos de novos entrantes e potenciais clientes para a Lupatech. Temos observado a presençade algumas empresas de petróleo evoluindo no mercado brasileiro, destacadamente a OGX,assim como novos EPCistas, com os quais pretendemos estabelecer relações comerciais.

[O restante dessa página foi deixado intencionalmente em branco]

9

IMPACTO PROCESSO ELEITORAL DE 2010

A Companhia espera que o processo eleitoral de 2010, que definirá o próximo presidente doBrasil, tenha reduzido impacto no mercado brasileiro. Acreditamos que os diversos programasde investimentos em vigor superarão a agenda política.

PROCESSO DE REESTRUTURAÇÃO

A estratégia de crescimento mais recente da Lupatech contempla aquisições, principalmenteno segmento Energy Products e Flow Control. Assim sendo, adquirimos 15 empresas desde2006. Num primeiro momento optamos por incorporar essas empresas à Lupatech semgrandes alterações na gestão e dia-a-dia, de forma a garantir a normal continuidade dosnegócios. Em 2009 aprofundamos o processo de integração desses quinze negóciosadquiridos entre 2006 e 2008 depois da fase inicial de incorporação.

Elaboramos um plano de incorporação destas empresas focando na geração de sinergias.Para isso foram revistas as práticas industriais, comerciais, administrativas, de recursoshumanos, entre outras, buscando eficiência de gestão e redução de custos e despesas fixas.

A conclusão dessa etapa está projetada para o ano de 2010 e deverá representar importantesevoluções em produtividade, eficiência e ganhos de competitividade.

Acreditamos que este é um grande passo para nos tornarmos cada vez mais preparados parao forte crescimento orgânico esperado para o setor de petróleo e gás, buscando cada vez maiscriação de valor para os acionistas.

CAPEX

A Companhia investiu nos últimos três anos cerca de R$250 milhões em expansão orgânica deseus negócios. Ampliamos a capacidade industrial de grande parte de nossos negócios nospreparando para o crescimento esperado para o setor de petróleo e gás, e esperamos que estacapacidade seja totalmente ocupada entre 2012 e 2013. Em 2009 operamos com utilização dacapacidade instalada próxima a 35% (média das unidades fabris) e para 2010 estimamosocupação média ao longo do ano da ordem de 50%.

Para os próximos dois anos não prevemos grandes investimentos de capital dada acapacidade industrial atualmente disponível na Companhia.

[O restante dessa página foi deixado intencionalmente em branco]

10

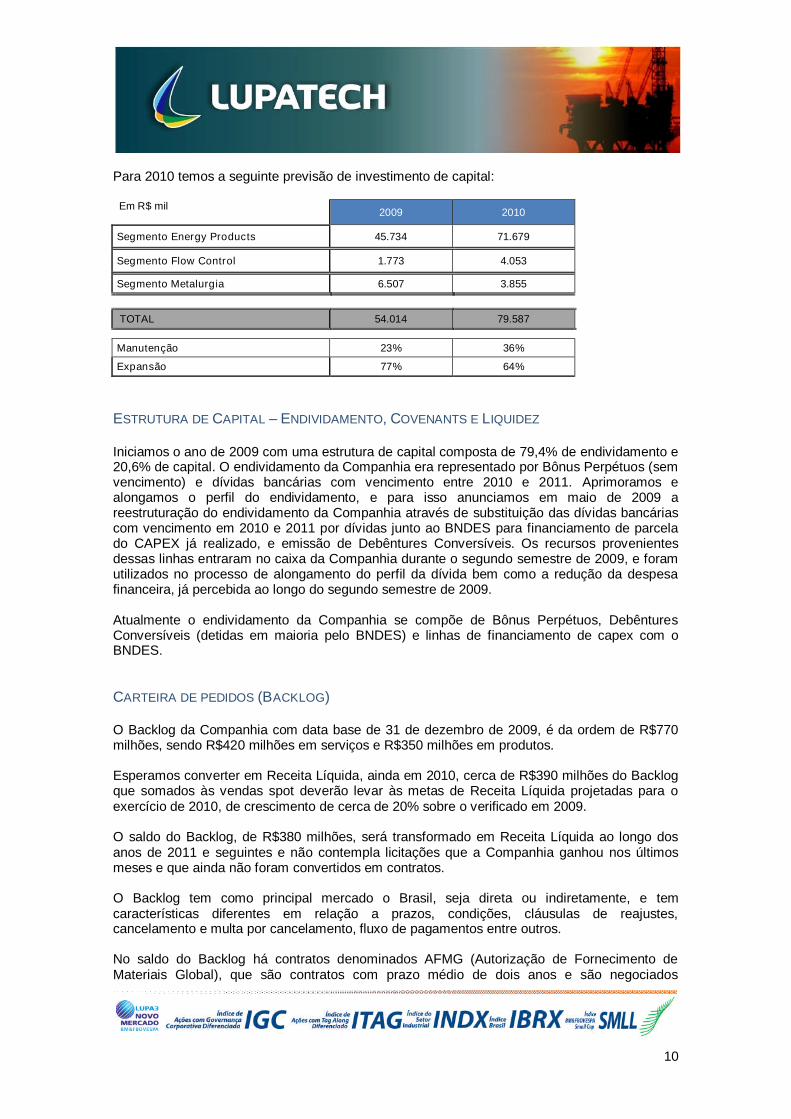

Para 2010 temos a seguinte previsão de investimento de capital:

Em R$ mil2009 2010

Segmento Energy Products 45.734 71.679

Segmento Flow Control 1.773 4.053

Segmento Metalurgia 6.507 3.855

TOTAL 54.014 79.587

Manutenção 23% 36%

Expansão 77% 64%

ESTRUTURA DE CAPITAL – ENDIVIDAMENTO, COVENANTS E LIQUIDEZ

Iniciamos o ano de 2009 com uma estrutura de capital composta de 79,4% de endividamento e20,6% de capital. O endividamento da Companhia era representado por Bônus Perpétuos (semvencimento) e dívidas bancárias com vencimento entre 2010 e 2011. Aprimoramos ealongamos o perfil do endividamento, e para isso anunciamos em maio de 2009 areestruturação do endividamento da Companhia através de substituição das dívidas bancáriascom vencimento em 2010 e 2011 por dívidas junto ao BNDES para financiamento de parcelado CAPEX já realizado, e emissão de Debêntures Conversíveis. Os recursos provenientesdessas linhas entraram no caixa da Companhia durante o segundo semestre de 2009, e foramutilizados no processo de alongamento do perfil da dívida bem como a redução da despesafinanceira, já percebida ao longo do segundo semestre de 2009.

Atualmente o endividamento da Companhia se compõe de Bônus Perpétuos, DebênturesConversíveis (detidas em maioria pelo BNDES) e linhas de financiamento de capex com oBNDES.

CARTEIRA DE PEDIDOS (BACKLOG)

O Backlog da Companhia com data base de 31 de dezembro de 2009, é da ordem de R$770milhões, sendo R$420 milhões em serviços e R$350 milhões em produtos.

Esperamos converter em Receita Líquida, ainda em 2010, cerca de R$390 milhões do Backlogque somados às vendas spot deverão levar às metas de Receita Líquida projetadas para oexercício de 2010, de crescimento de cerca de 20% sobre o verificado em 2009.

O saldo do Backlog, de R$380 milhões, será transformado em Receita Líquida ao longo dosanos de 2011 e seguintes e não contempla licitações que a Companhia ganhou nos últimosmeses e que ainda não foram convertidos em contratos.

O Backlog tem como principal mercado o Brasil, seja direta ou indiretamente, e temcaracterísticas diferentes em relação a prazos, condições, cláusulas de reajustes,cancelamento e multa por cancelamento, fluxo de pagamentos entre outros.

No saldo do Backlog há contratos denominados AFMG (Autorização de Fornecimento deMateriais Global), que são contratos com prazo médio de dois anos e são negociados

11

diretamente com clientes finais, ou seja, sem intermediação de EPCistas (empresas deEngineering, Procurement and Constructing - Engenharia, Compras e Construção).

As AFMGs são direcionadas, principalmente, para manutenção, reposição e operação da infra-estrutura já instalada, onde se determina o preço para os produtos a serem fornecidos, sendoautomaticamente reajustado anualmente refletindo a variação dos custos, destacadamentematérias-primas e mão-de-obra.

[O restante dessa página foi deixado intencionalmente em branco]

12

CONSIDERAÇÕES FINAIS

A Administração deseja reafirmar seu compromisso de longo prazo com clientes, acionistas,credores, colaboradores e com o mercado de capitais.

Os Auditores Independentes, Deloitte Touche Tohmatsu Auditores Independentes (Deloitte),que examinam as demonstrações financeiras desde 2008, prestaram somente serviços àLupatech S.A. relacionados à auditoria das demonstrações financeiras.

Estão disponíveis no site www.lupatech.com.br/ri os comentários sobre o desempenhoconsolidado dos negócios da Companhia.

A Companhia está vinculada à arbitragem na Câmara de Arbitragem do Mercado, conformecláusula compromissória constante do Estatuto Social.

Caxias do Sul, 29 de março de 2010.

Conselho de AdministraçãoNestor PeriniAlcinei Cardoso RodriguesClóvis Benoni MeurerJosé Coutinho BarbosaJosé Mauro Mettrau Carneiro da CunhaJosé Teófilo Abu-JamraMarcelo Cabrera da Costa

Conselheiros SuplentesFabio Sotelino da RochaTeresa Rodriguez Cao

DiretoresNestor PeriniJosé Teófilo Abu-JamraGilberto Pasquale da SilvaThiago Alonso de Oliveira

[O restante dessa página foi deixado intencionalmente em branco]

13

COMENTÁRIOS DA ADMINISTRAÇÃO AO DESEMPENHO ECONÔMICO-FINANCEIRO

CONSOLIDADO – BASE IFRS

RECEITA LÍQUIDA

Receita Líquida (em R$ Mil) 3T09 4T09 Var. % 2008 2009 Var. %

Energy Products 85.634 66.670 -22,1% 450.934 386.404 -14,3%

Energy Products - Mercado Interno 71.725 39.233 -45,3% 339.095 251.096 -26,0%

Energy Products - Mercado Externo 13.909 27.437 97,3% 111.839 135.308 21,0%

Flow Control 29.623 28.034 -5,4% 164.203 117.080 -28,7%

Flow Control - Mercado Interno 28.000 26.488 -5,4% 149.809 108.312 -27,7%

Flow Control - Mercado Externo 1.623 1.546 -4,7% 14.394 8.768 -39,1%

Metalurgia 12.972 13.114 1,1% 89.535 51.678 -42,3%

Metalurgia - Mercado Interno 10.771 10.633 -1,3% 59.216 37.642 -36,4%

Metalurgia - Mercado Externo 2.201 2.481 12,7% 30.319 14.036 -53,7%

Total 128.230 107.818 -15,9% 704.673 555.162 -21,2%

% Energy Products 66,8% 61,8% 64,0% 69,6%

% Energy Products - Mercado Interno 83,8% 58,8% 75,2% 65,0%

% Energy Products - Mercado Externo 16,2% 41,2% 24,8% 35,0%

% Flow Control 23,1% 26,0% 23,3% 21,1%

% Flow Control - Mercado Interno 94,5% 94,5% 91,2% 92,5%

% Flow Control - Mercado Externo 5,5% 5,5% 8,8% 7,5%

% Metalurgia 10,1% 12,2% 12,7% 9,3%

% Metalurgia - Mercado Interno 83,0% 81,1% 66,1% 72,8%

% Metalurgia - Mercado Externo 17,0% 18,9% 33,9% 27,2%

A Receita Líquida Consolidada do exercício de 2009 é 21,2% menor em comparação com oexercício de 2008, atingindo R$555,2 milhões. A queda é atribuída às condiçõesmercadológicas que causaram desaquecimento de demanda em todos os segmentos deatuação da Companhia assim como queda de preços.

A Receita Líquida Consolidada do 4T09 atingiu R$107,8 milhões, 15,9% inferior ao 3T09quando somou R$128,2 milhões. A queda observada durante o 4T09 é consequência da quedade atividade comercial observadas durante o exercício de 2009 que teve seus maioresimpactos neste trimestre.

A Receita Líquida do Segmento Energy Products no exercício de 2009 alcançou R$386,4milhões, queda de 14,3% em comparação ao exercício de 2008 quando atingiu R$450,9milhões. Este segmento foi fortemente afetado pela queda de demanda no setor de petróleo egás, especificamente nos projetos de produção onde a Companhia tem grande exposição, equeda de preços.

A Receita Líquida do Segmento Energy Products no 4T09 alcançou R$66,7 milhões, queda de22,1% em comparação ao 3T09 quando atingiu R$85,6 milhões. Conforme acima mencionado,a queda observada durante o 4T09 é consequência da queda de atividade comercialobservada durante o exercício de 2009 que teve maiores impactos neste trimestre.

A Receita Líquida do Segmento Flow Control no exercício de 2009 alcançou R$117,1 milhões,queda de 28,7% em comparação ao exercício de 2008 quando atingiu R$164,2 milhões. Este

14

segmento foi fortemente afetado pela queda de atividade industrial no Brasil e Argentina, frutoda crise mundial iniciada em 2008, assim como queda de preços.

A Receita Líquida do Segmento Flow Control no 4T09 alcançou R$28,0 milhões, queda de5,4% em comparação ao 3T09 quando atingiu R$29,6 milhões. Esta queda é fruto do mix depedidos com menor valor agregado que foram produzidos nas unidades de válvulas no Brasil.

A Receita Líquida do Segmento Metalurgia no exercício de 2009 alcançou R$51,7 milhões,queda de 42,3% em comparação ao exercício de 2008 quando atingiu R$89,5 milhões. Estesegmento foi fortemente impactado pela crise mundial que afetou diretamente o setorautomobilístico, principalmente nos EUA e Europa, mercados de grande representatividade nofaturamento das unidades deste segmento.

A Receita Líquida do Segmento Metalurgia no 4T09 alcançou R$13,1 milhões, crescimento de1,1% em comparação ao 3T09 quando atingiu R$13,0 milhões. Este crescimento é fruto deleve recuperação nos pedidos relacionados à indústria automotiva no Brasil.

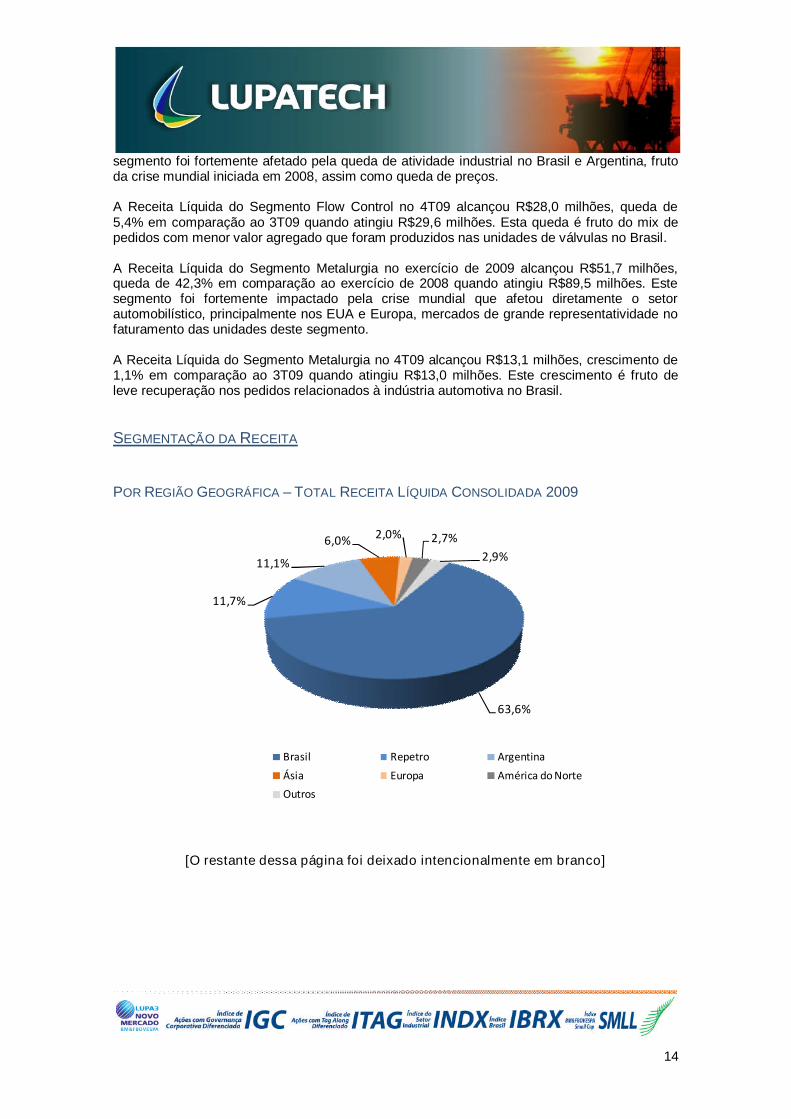

SEGMENTAÇÃO DA RECEITA

POR REGIÃO GEOGRÁFICA – TOTAL RECEITA LÍQUIDA CONSOLIDADA 2009

[O restante dessa página foi deixado intencionalmente em branco]

63,6%

11,7%

11,1%

6,0% 2,0% 2,7%

2,9%

Brasil Repetro Argentina

Ásia Europa América do Norte

Outros

15

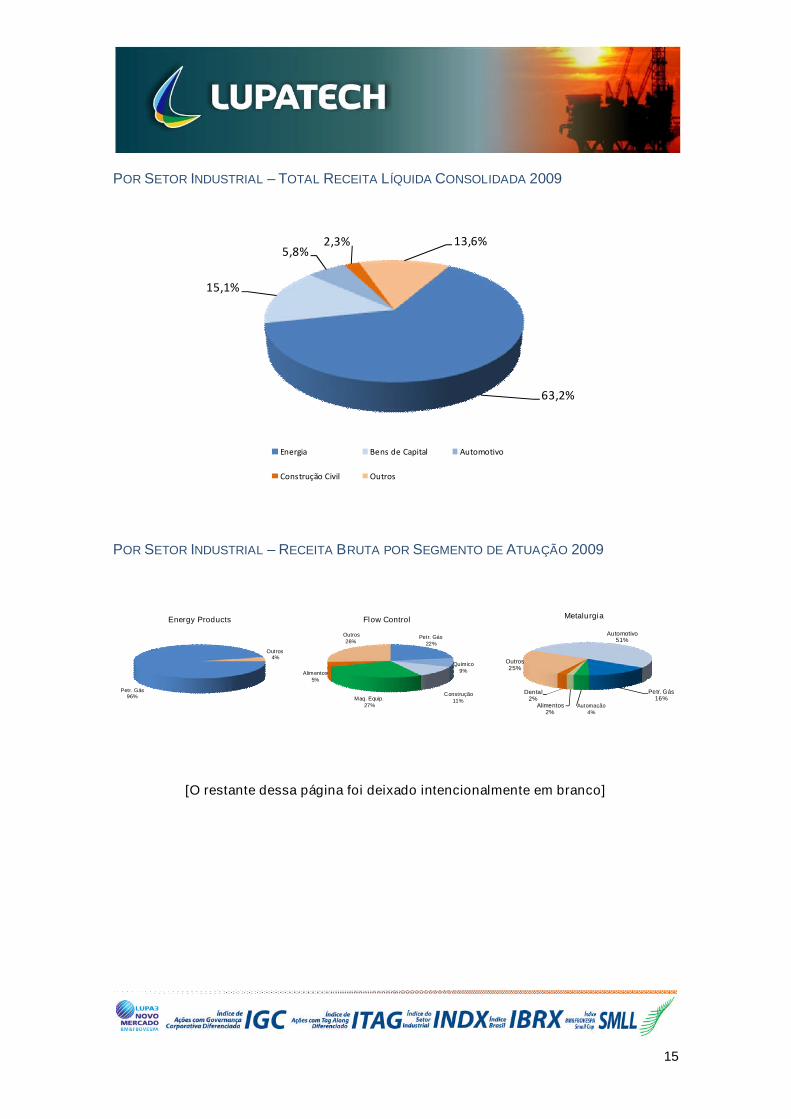

POR SETOR INDUSTRIAL – TOTAL RECEITA LÍQUIDA CONSOLIDADA 2009

POR SETOR INDUSTRIAL – RECEITA BRUTA POR SEGMENTO DE ATUAÇÃO 2009

[O restante dessa página foi deixado intencionalmente em branco]

63,2%

15,1%

5,8%2,3% 13,6%

Energia Bens de Capital Automotivo

Construção Civil Outros

Petr. Gás22%

Químico9%

Construção11%Maq. Equip.

27%

Alimentos5%

Outros26%

Automotivo51%

Petr. Gás16%

Automação4%

Alimentos2%

Dental2%

Outros25%

Petr. Gás96%

Outros4%

Energy Products Flow Control Metalurgia

16

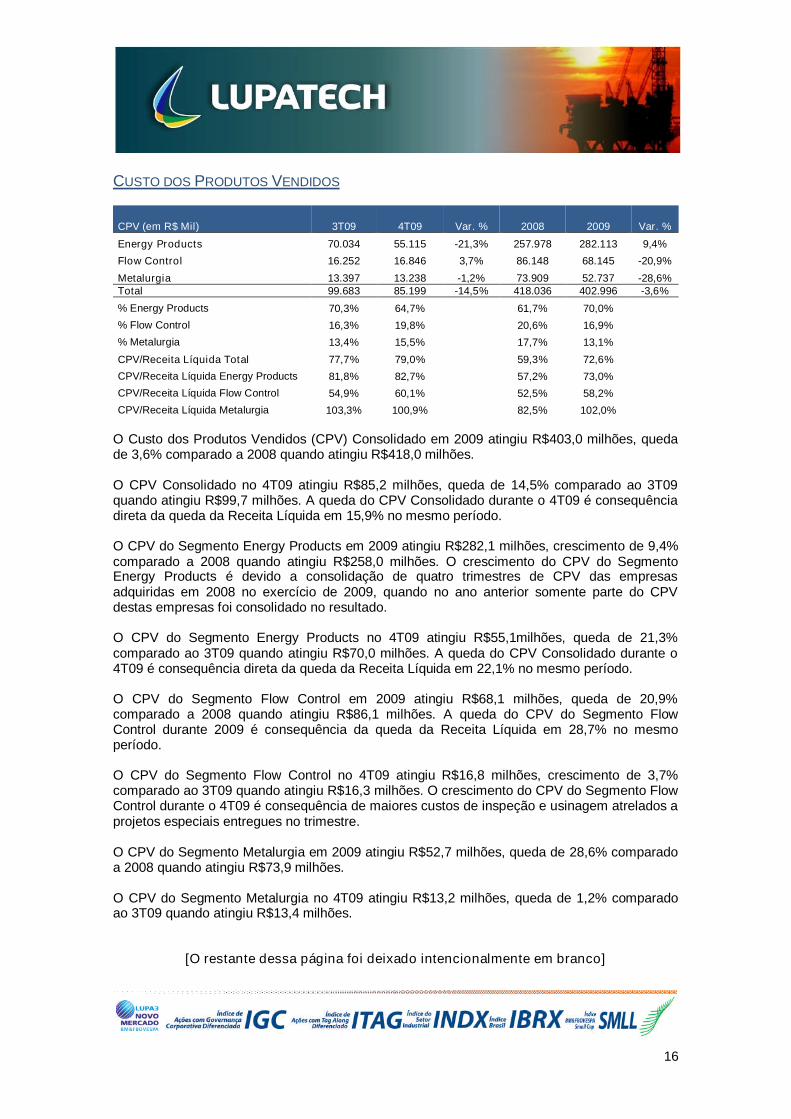

CUSTO DOS PRODUTOS VENDIDOS

CPV (em R$ Mil) 3T09 4T09 Var. % 2008 2009 Var. %

Energy Products 70.034 55.115 -21,3% 257.978 282.113 9,4%

Flow Control 16.252 16.846 3,7% 86.148 68.145 -20,9%

Metalurgia 13.397 13.238 -1,2% 73.909 52.737 -28,6%Total 99.683 85.199 -14,5% 418.036 402.996 -3,6%

% Energy Products 70,3% 64,7% 61,7% 70,0%

% Flow Control 16,3% 19,8% 20,6% 16,9%

% Metalurgia 13,4% 15,5% 17,7% 13,1%

CPV/Receita Líquida Total 77,7% 79,0% 59,3% 72,6%

CPV/Receita Líquida Energy Products 81,8% 82,7% 57,2% 73,0%

CPV/Receita Líquida Flow Control 54,9% 60,1% 52,5% 58,2%

CPV/Receita Líquida Metalurgia 103,3% 100,9% 82,5% 102,0%

O Custo dos Produtos Vendidos (CPV) Consolidado em 2009 atingiu R$403,0 milhões, quedade 3,6% comparado a 2008 quando atingiu R$418,0 milhões.

O CPV Consolidado no 4T09 atingiu R$85,2 milhões, queda de 14,5% comparado ao 3T09quando atingiu R$99,7 milhões. A queda do CPV Consolidado durante o 4T09 é consequênciadireta da queda da Receita Líquida em 15,9% no mesmo período.

O CPV do Segmento Energy Products em 2009 atingiu R$282,1 milhões, crescimento de 9,4%comparado a 2008 quando atingiu R$258,0 milhões. O crescimento do CPV do SegmentoEnergy Products é devido a consolidação de quatro trimestres de CPV das empresasadquiridas em 2008 no exercício de 2009, quando no ano anterior somente parte do CPVdestas empresas foi consolidado no resultado.

O CPV do Segmento Energy Products no 4T09 atingiu R$55,1milhões, queda de 21,3%comparado ao 3T09 quando atingiu R$70,0 milhões. A queda do CPV Consolidado durante o4T09 é consequência direta da queda da Receita Líquida em 22,1% no mesmo período.

O CPV do Segmento Flow Control em 2009 atingiu R$68,1 milhões, queda de 20,9%comparado a 2008 quando atingiu R$86,1 milhões. A queda do CPV do Segmento FlowControl durante 2009 é consequência da queda da Receita Líquida em 28,7% no mesmoperíodo.

O CPV do Segmento Flow Control no 4T09 atingiu R$16,8 milhões, crescimento de 3,7%comparado ao 3T09 quando atingiu R$16,3 milhões. O crescimento do CPV do Segmento FlowControl durante o 4T09 é consequência de maiores custos de inspeção e usinagem atrelados aprojetos especiais entregues no trimestre.

O CPV do Segmento Metalurgia em 2009 atingiu R$52,7 milhões, queda de 28,6% comparadoa 2008 quando atingiu R$73,9 milhões.

O CPV do Segmento Metalurgia no 4T09 atingiu R$13,2 milhões, queda de 1,2% comparadoao 3T09 quando atingiu R$13,4 milhões.

[O restante dessa página foi deixado intencionalmente em branco]

17

ESTRUTURA DE CUSTOS

Abaixo, apresenta-se a evolução da estrutura de custos do 1T09 até o 4T09.

Estrutura de Custos (em %) 1T09 2T09 3T09 4T09

Energy Products

Matéria-Prima 64,5 60,6 52,0 37,5

Mão de Obra 20,1 20,6 25,5 32,5

GGF 9,0 13,8 15,1 21,4

Depreciações 6,4 5,0 7,4 8,6

Flow Control

Matéria-Prima 62,6 66,1 63,5 61,2

Mão de Obra 20,2 18,7 18,8 23,7

GGF 11,4 9,2 12,4 8,9

Depreciações 5,8 6,0 5,3 6,2

Metalurgia

Matéria-Prima 36,5 36,4 39,5 36,9

Mão de Obra 27,6 29,8 30,0 29,5

GGF 15,2 12,4 11,4 14,9

Energia Elétrica 5,7 6,5 5,2 5,9

Depreciações 15,0 14,9 13,9 12,8*GGF: gastos gerais de fabricação (água, luz, etc.)

CPV - PRINCIPAIS COMPONENTES DO TOTAL DE MATÉRIA-PRIMA EM 2009

[O restante dessa página foi deixado intencionalmente em branco]

17,2%

23,0%12,1%

47,7%

Aço inoxidável

Aço carbono

Poliéster

Ceras & Outros

18

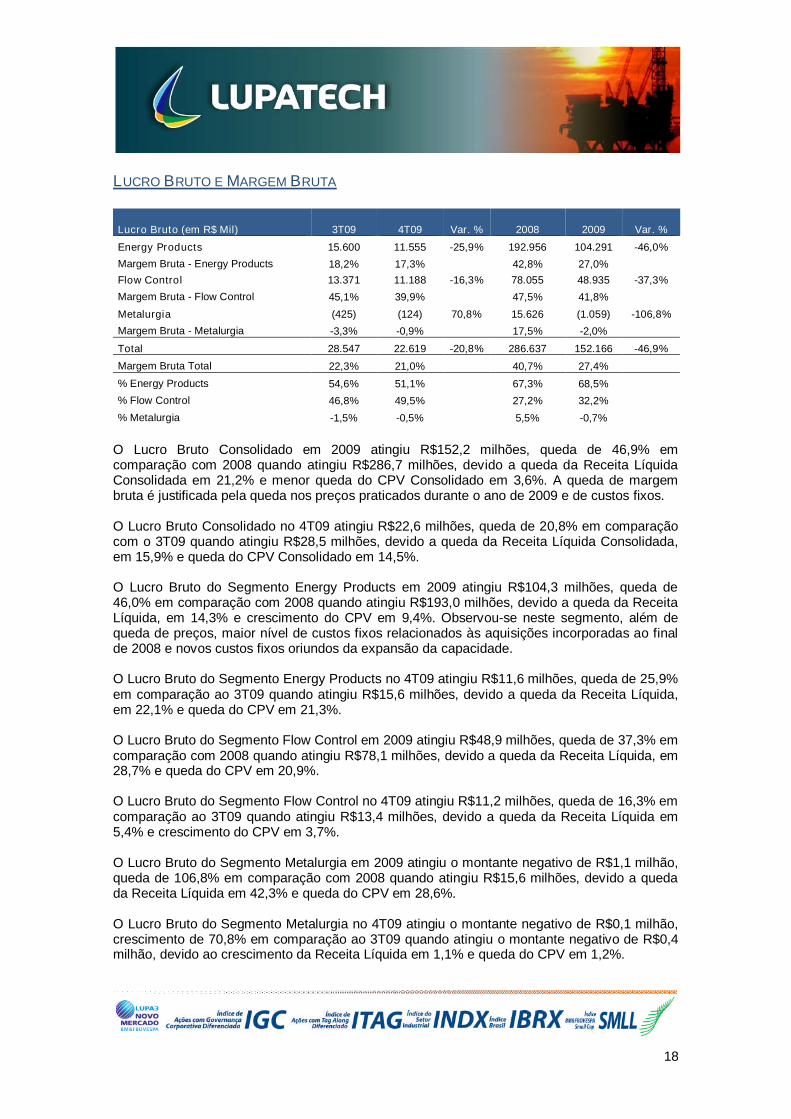

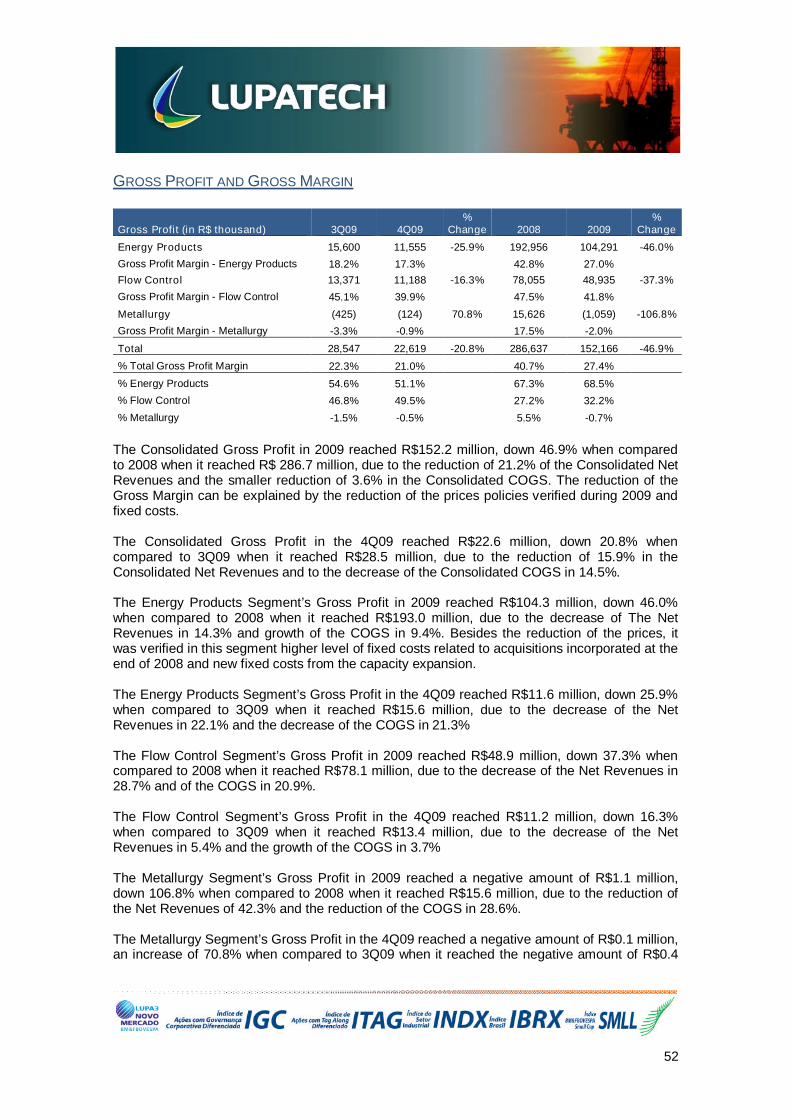

LUCRO BRUTO E MARGEM BRUTA

Lucro Bruto (em R$ Mil) 3T09 4T09 Var. % 2008 2009 Var. %

Energy Products 15.600 11.555 -25,9% 192.956 104.291 -46,0%

Margem Bruta - Energy Products 18,2% 17,3% 42,8% 27,0%

Flow Control 13.371 11.188 -16,3% 78.055 48.935 -37,3%

Margem Bruta - Flow Control 45,1% 39,9% 47,5% 41,8%

Metalurgia (425) (124) 70,8% 15.626 (1.059) -106,8%

Margem Bruta - Metalurgia -3,3% -0,9% 17,5% -2,0%

Total 28.547 22.619 -20,8% 286.637 152.166 -46,9%

Margem Bruta Total 22,3% 21,0% 40,7% 27,4%

% Energy Products 54,6% 51,1% 67,3% 68,5%

% Flow Control 46,8% 49,5% 27,2% 32,2%

% Metalurgia -1,5% -0,5% 5,5% -0,7%

O Lucro Bruto Consolidado em 2009 atingiu R$152,2 milhões, queda de 46,9% emcomparação com 2008 quando atingiu R$286,7 milhões, devido a queda da Receita LíquidaConsolidada em 21,2% e menor queda do CPV Consolidado em 3,6%. A queda de margembruta é justificada pela queda nos preços praticados durante o ano de 2009 e de custos fixos.

O Lucro Bruto Consolidado no 4T09 atingiu R$22,6 milhões, queda de 20,8% em comparaçãocom o 3T09 quando atingiu R$28,5 milhões, devido a queda da Receita Líquida Consolidada,em 15,9% e queda do CPV Consolidado em 14,5%.

O Lucro Bruto do Segmento Energy Products em 2009 atingiu R$104,3 milhões, queda de46,0% em comparação com 2008 quando atingiu R$193,0 milhões, devido a queda da ReceitaLíquida, em 14,3% e crescimento do CPV em 9,4%. Observou-se neste segmento, além dequeda de preços, maior nível de custos fixos relacionados às aquisições incorporadas ao finalde 2008 e novos custos fixos oriundos da expansão da capacidade.

O Lucro Bruto do Segmento Energy Products no 4T09 atingiu R$11,6 milhões, queda de 25,9%em comparação ao 3T09 quando atingiu R$15,6 milhões, devido a queda da Receita Líquida,em 22,1% e queda do CPV em 21,3%.

O Lucro Bruto do Segmento Flow Control em 2009 atingiu R$48,9 milhões, queda de 37,3% emcomparação com 2008 quando atingiu R$78,1 milhões, devido a queda da Receita Líquida, em28,7% e queda do CPV em 20,9%.

O Lucro Bruto do Segmento Flow Control no 4T09 atingiu R$11,2 milhões, queda de 16,3% emcomparação ao 3T09 quando atingiu R$13,4 milhões, devido a queda da Receita Líquida em5,4% e crescimento do CPV em 3,7%.

O Lucro Bruto do Segmento Metalurgia em 2009 atingiu o montante negativo de R$1,1 milhão,queda de 106,8% em comparação com 2008 quando atingiu R$15,6 milhões, devido a quedada Receita Líquida em 42,3% e queda do CPV em 28,6%.

O Lucro Bruto do Segmento Metalurgia no 4T09 atingiu o montante negativo de R$0,1 milhão,crescimento de 70,8% em comparação ao 3T09 quando atingiu o montante negativo de R$0,4milhão, devido ao crescimento da Receita Líquida em 1,1% e queda do CPV em 1,2%.

19

DESPESAS

Despesas (em R$ Mil) 3T09 4T09 Var. % 2008 2009 Var. %

Total de Despesas com vendas 11.959 14.859 24,2% 60.993 57.170 -6,3%

Total de Despesas administrativas 14.360 12.056 -16,0% 47.621 51.972 9,1%

Energy Products 16.775 17.396 3,7% 64.764 72.484 11,9%

Despesas com vendas - Energy Products 7.070 9.490 34,2% 36.592 37.822 3,4%

Despesas administrativas - Energy Products 9.705 7.906 -18,5% 28.172 34.662 23,0%

Flow Control 7.099 7.329 3,2% 30.008 27.190 -9,4%

Despesas com vendas - Flow Control 3.676 4.077 10,9% 15.828 14.118 -10,8%

Despesas administrativas - Flow Control 3.423 3.252 -5,0% 14.180 13.072 -7,8%

Metalurgia 2.445 2.190 -10,4% 13.841 9.469 -31,6%

Despesas com vendas - Metalurgia 1.213 1.292 6,5% 8.572 5.230 -39,0%

Despesas administrativas - Metalurgia 1.232 898 -27,1% 5.269 4.239 -19,6%

Total de vendas e administrativas 26.319 26.915 2,3% 108.614 109.142 0,5%

Honorários dos Administradores 678 870 28,3% 1.991 2.750 38,1%

Total Desp. vendas, admin. e honorários 26.997 27.785 2,9% 110.604 111.892 1,2%

% Energy Products 63,7% 64,6% 59,6% 66,4%

% Flow Control 27,0% 27,2% 27,6% 24,9%

% Metalurgia 9,3% 8,1% 12,7% 8,7%

Despesas com vendas/Total Rec. Líquida 9,3% 13,8% 8,7% 10,3%

Despesas administrativas/Total Rec. Líquida 11,2% 11,2% 6,8% 9,4%

Despesas com honorários/Total Rec. Líquida 0,5% 0,8% 0,3% 0,5%

Despesas/Receita Líquida Total 21,1% 25,8% 15,7% 20,2%

Despesas/Receita Líquida Energy Products 19,6% 26,1% 14,4% 18,8%

Despesas/Receita Líquida Flow Control 24,0% 26,1% 18,3% 23,2%

Despesas/Receita Líquida Metalurgia 18,8% 16,7% 15,5% 18,3%

As Despesas Gerais com Vendas, Administrativas e Honorários Consolidadas cresceram 1,2%em 2009 e atingiram R$111,9 milhões, contra R$110,6 milhões em 2008. Essa variaçãodecorre principalmente do crescimento das despesas administrativas em 9,1% atingindoR$52,0 milhões, devido à maior nível de despesas administrativas para dar suporte à novaestrutura industrial oriunda das expansões concluídas ao final de 2008 e durante o ano de2009, assim como a consolidação de quatro trimestres de despesas das empresas adquiridasem 2008 no exercício de 2009, quando no ano anterior somente parte das despesas destasempresas foram consolidadas no resultado.

As Despesas Gerais com Vendas, Administrativas e Honorários Consolidadas cresceram 2,9%no 4T09 e atingiram R$27,8 milhões, contra R$27,0 milhões no 3T09. Ainda que tenha seobservado queda nas Despesas Administrativas Consolidadas no 4T09 em 16,0%, primeirosfrutos do processo de reestruturação, houve crescimento das Despesas com VendasConsolidadas em 24,2%, devido a principalmente custos de frete, aumento de despesas comcomissões e outras despesas comerciais.

As Despesas Gerais com Vendas e Administrativas do Segmento Energy Products cresceram11,9% em 2009 e atingiram R$72,5 milhões, contra R$64,8 milhões em 2008. Este crescimentoé decorrente principalmente do crescimento das Despesas Administrativas deste segmento em23,0%. As expansões que foram efetuadas nas unidades assim como novas unidades que

20

foram construídas neste segmento, resultaram em maior nível de despesas administrativasnecessárias para dar suporte às operações.

As Despesas Gerais com Vendas e Administrativas do Segmento Energy Products cresceram3,7% no 4T09 e atingiram R$17,4 milhões, contra R$16,8 milhões no 3T09. Este crescimento édecorrente principalmente do crescimento das Despesas com Vendas deste segmento em34,2%, devido maiores custos com frete e outras despesas comerciais.

As Despesas Gerais com Vendas e Administrativas do Segmento Flow Control decresceram9,4% em 2009 e atingiram R$27,2 milhões, contra R$30,0 milhões em 2008. Esta queda édecorrente da queda das Despesas com Vendas em 10,8%, fruto de menor atividade comercialno ano, e também queda das Despesas Administrativas em 7,8%.

As Despesas Gerais com Vendas e Administrativas do Segmento Flow Control cresceram 3,2%no 4T09 e atingiram R$7,3 milhões, contra R$7,1 milhões no 3T09. Este crescimento édecorrente principalmente do crescimento das Despesas com Vendas deste segmento em10,9%.

As Despesas Gerais com Vendas e Administrativas do Segmento Metalurgia decresceram31,6% em 2009 e atingiram R$9,5 milhões, contra R$13,8 milhões em 2008. Esta queda édecorrente da queda das Despesas com Vendas em 39,0%, fruto de menor atividade comercialno ano, e também queda das Despesas Administrativas em 19,6%.

As Despesas Gerais com Vendas e Administrativas do Segmento Metalurgia decresceram10,4% no 4T09 e atingiram R$2,2 milhões, contra R$2,4 milhões no 3T09. Esta queda édecorrente da queda das Despesas Administrativas deste segmento em 27,1%.

OUTRAS RECEITAS E DESPESAS OPERACIONAIS E RESULTADO DE EQUIVALÊNCIA EM

OUTRAS COLIGADAS

Receitas e Despesas Operacionais (em R$Mil) 3T09 4T09 Var. % 2008 2009 Var. %

Receitas Operacionais 794 3.859 386,0% 6.088 6.631 8,9%

Despesas Operacionais (2.488) (6.909) 177,7% (13.512) (17.775) 31,6%

Despesas Operacionais (1.758) (6.482) 268,7% (6.540) (10.588) 61,9%

Despesas Operacionais não recorrentes (730) (427) -41,5% (6.970) (7.187) 3,1%

Resultado da Equivalência Patrimonial 217 92 -57,6% 928 749 -19,3%

Total (1.477) (2.958) 100,3% (6.495) (10.394) 60,0%

As Outras Receitas Operacionais somaram R$6,7 milhões em 2009, contra R$6,1 milhões em2008. Estas receitas operacionais são relacionadas à venda de imobilizado, recuperação decontingências e impostos.

As Outras Receitas Operacionais somaram R$3,9 milhões no 4T09, contra R$0,8 milhão no3T09. Estas receitas operacionais são relacionadas a recuperação de contingências eimpostos.

As Outras Despesas Operacionais somaram R$17,8 milhões em 2009 contra R$13,5 milhõesem 2008. Essas despesas são relacionadas a perdas com contingências, baixa de estoqueobsoleto, custo do imobilizado baixado, e outras despesas não recorrentes relacionadasprincipalmente a gastos diferidos apropriados no resultado quando da realização de aquisições,que em 2009 somaram R$7,2 milhões versus R$7,0 milhões em 2008.

21

As Outras Despesas Operacionais somaram R$6,9 milhões no 4T09 contra R$2,5 milhões no3T09. Essas despesas se referem a baixa de estoque obsoleto e custo do imobilizado baixado,assim como despesas não recorrentes no valor de R$0,4 milhão.

O Resultado da Equivalência Patrimonial decresceu 19,3% em 2009 em comparação com2008, atingindo R$0,7 milhão, devido aos resultados das empresas coligadas Aspro Carwal eAspro Serviços (ver Nota Explicativa nº. 08). No 4T09, o Resultado da Equivalência Patrimonialrepresentou R$0,1 milhão versus R$0,2 milhão no 3T09.

As Outras Receitas e Despesas Operacionais verificadas em 2009 alcançaram o valor negativo(despesa) de R$10,4 milhões, contra uma despesa de R$6,5 milhões em 2008, o querepresenta crescimento de 60,0%.

As Outras Receitas e Despesas Operacionais verificadas no 4T09 alcançaram o valor negativo(despesa) de R$3,0 milhões, contra uma despesa de R$1,5 milhão no 3T09, o que representacrescimento de 100,3%.

RESULTADO FINANCEIRO

Resultado Financeiro Líquido (R$ Mil) 2008 2009 Var. %

Receita com Juros 6.562 11.412 73,9%

Outros 1.977 14.978 657,4%

Receita Financeira (excluindo VC*) 8.540 26.390 209,0%

Despesa com Juros 92.498 99.743 7,8%

Derivativos embutidos (debêntures conversíveis) - 11.597 n.a.

Impostos Financeiros 6.373 4.575 -28,2%

Outros 4.992 10.898 118,3%

Despesa Financeira (excluindo VC*) 103.863 126.813 22,1%

Resultado Financeiro Líquido (excluindo VC*) (95.323) (100.423) 5,4%

Receita de Variação Cambial 34.956 162.933 366,1%

Despesa de Variação Cambial (134.151) (65.029) -51,5%

Variação Cambial Líquida (99.195) 97.904 198,7%

Resultado Financeiro Líquido TOTAL (194.518) (2.519) -98,7%

*Variação Cambial

A Receita Financeira (excluindo Variação Cambial) Total da Companhia em 2009 atingiuR$26,4 milhões, 209,0% superior a 2008 quando atingiu R$8,5 milhões. Este crescimento édecorrente de maior receita com juros consequência da aplicação de recursos financeiros noBrasil, que permitiu à companhia acessar melhores taxas de remuneração do que as obtidasem 2008 quando os excedentes de caixa estavam no exterior. A variação também pode serjustificada pela inclusão de receitas financeiras relacionadas ao Ajuste a Valor Presente (AVP)sobre o Contas a Receber.

A Despesa Financeira (excluindo Variação Cambial) Total da Companhia em 2009 cresceu22,1% atingindo o valor de R$126,8 milhões versus R$103,9 milhões em 2008. Ainda que coma reestruturação da dívida mencionada no Relatório da Administração que resultou em menorcusto total de endividamento, o crescimento da Despesa Financeira pode ser justificado pordiversos fatores, entre eles (i) o pagamento de juros sobre o total dos Bônus Perpétuos

22

(US$275 milhões) durante todo o ano de 2009 enquanto 2008 foram pagos juros sobre o totalsomente a partir de junho (até aquela data representavam apenas US$200 milhões); (ii) opagamento de juros relacionados às Debêntures Conversíveis a partir de abril de 2009; e (iii) ainclusão da despesa relacionada a precificação a valor justo de derivativos embutidos naescritura das Debêntures Conversíveis relacionados a cláusula de conversão mandatória ouresgate antecipado (item não caixa).

A Variação Cambial Líquida em 2009 resultou em receita de R$97,9 milhões versus despesade R$99,2 milhões em 2008. Este resultado é justificado pela apreciação da moeda brasileira(Real) perante o Dólar Americano durante o ano de 2009.

Efeito da variação cambial sobre ativos e passivos

A Companhia possui ativos e passivos denominados em moedas estrangeiras, principalmenteo dólar americano, o que pode gerar ganhos ou perdas com flutuações nas taxas de câmbio.

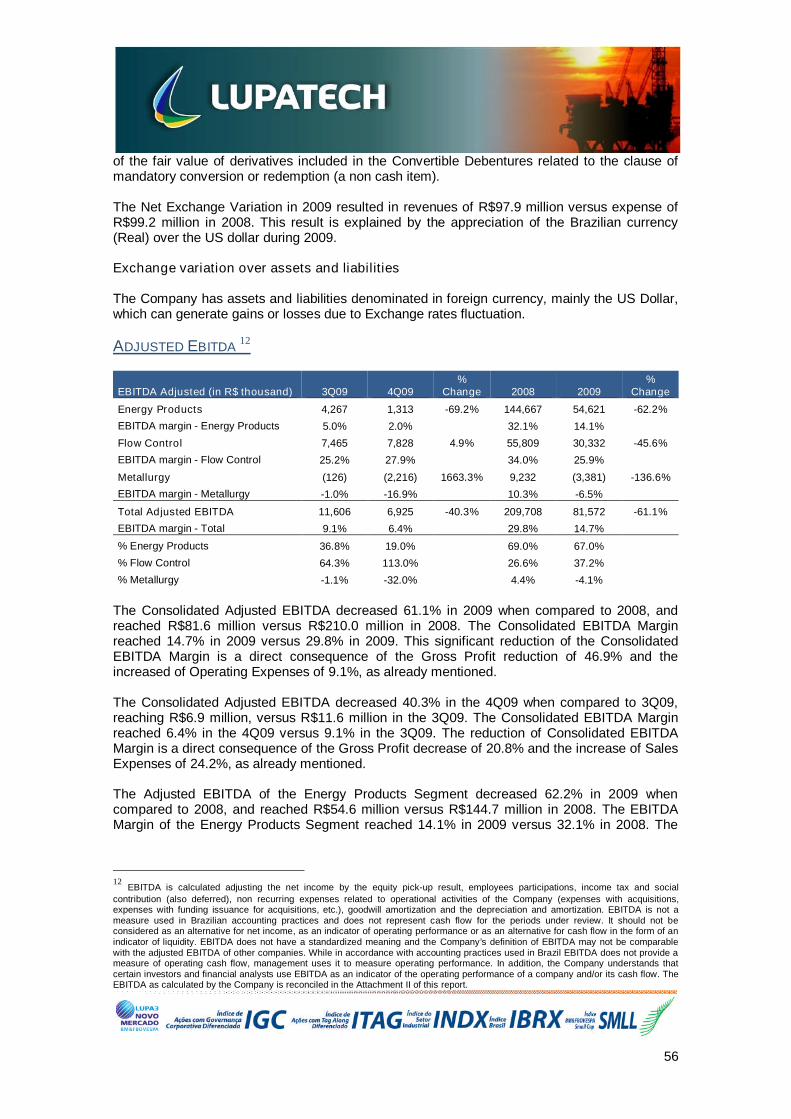

EBITDA AJUSTADO5

EBITDA Ajustado (em R$ Mil) 3T09 4T09 Var. % 2008 2009 Var. %

Energy Products 4.267 1.313 -69,2% 144.667 54.621 -62,2%

Margem EBITDA - Energy Products 5,0% 2,0% 32,1% 14,1%

Flow Control 7.465 7.828 4,9% 55.809 30.332 -45,6%

Margem EBITDA - Flow Control 25,2% 27,9% 34,0% 25,9%

Metalurgia (126) (2.216) 1663,3% 9.232 (3.381) -136,6%

Margem EBITDA - Metalurgia -1,0% -16,9% 10,3% -6,5%

Total EBITDA Ajustado 11.606 6.925 -40,3% 209.708 81.572 -61,1%

Margem EBITDA Total 9,1% 6,4% 29,8% 14,7%

% Energy Products 36,8% 19,0% 69,0% 67,0%

% Flow Control 64,3% 113,0% 26,6% 37,2%

% Metalurgia -1,1% -32,0% 4,4% -4,1%

O EBITDA Ajustado Consolidado recuou 61,1% em 2009 quando comparado a 2008, e atingiuR$81,6 milhões versus R$210,0 milhões em 2008. A Margem EBITDA Consolidada alcançou14,7% em 2009 versus 29,8% em 2009. A expressiva queda da Margem EBITDA Consolidadaé consequência direta da queda do Lucro Bruto em 46,9% e aumento das DespesasAdministrativas em 9,1%, conforme já apresentado.

O EBITDA Ajustado Consolidado decresceu 40,3% no 4T09 quando comparado ao 3T09, eatingiu R$6,9 milhões, versus R$11,6 milhões no 3T09. A Margem EBITDA Consolidadaalcançou 6,4% no 4T09 versus 9,1% no 3T09. A queda da Margem EBITDA Consolidada é

5EBITDA é calculado ajustando o lucro líquido pelo resultado de equivalência patrimonial, participações de empregados, imposto de

renda e contribuição social (e diferimentos), despesas não recorrentes relacionadas às atividades operacionais da Companhia(despesas com aquisições de empresas, gastos com captações de recursos atrelados a aquisições de companhias, etc.), amortizaçãode ágio e a depreciação e amortização. O EBITDA não é uma medida utilizada nas práticas contábeis adotadas no Brasil, nãorepresentando o fluxo de caixa para os períodos apresentados e não deve ser considerado como sendo uma alternativa ao lucro líquidona qualidade de indicador do desempenho operacional ou como uma alternativa ao fluxo de caixa na qualidade de indicador de liquidez.O EBITDA não tem um significado padronizado e a definição de EBITDA da Companhia pode não ser comparável ao EBITDA ouEBITDA ajustado conforme definido por outras Companhias. Ainda que o EBITDA não forneça, de acordo com as práticas contábeisutilizadas no Brasil uma medida do fluxo de caixa operacional, a Administração o utiliza para mensurar seu desempenho operacional.Adicionalmente, a Companhia entende que determinados investidores e analistas financeiros utilizam o EBITDA como indicador dodesempenho operacional de uma Companhia e/ou de seu fluxo de caixa. A reconciliação do EBITDA conforme calculado pelaCompanhia pode ser encontrado no Anexo II deste relatório.

23

consequência direta da queda do Lucro Bruto em 20,8% e aumento das Despesas com Vendasem 24,2%, conforme já apresentado.

O EBITDA Ajustado do Segmento Energy Products decresceu 62,2% em 2009 quandocomparado a 2008, e atingiu R$54,6 milhões versus R$144,7 milhões em 2008. A MargemEBITDA do Segmento Energy Products alcançou 14,1% em 2009 versus 32,1% em 2008. Aexpressiva queda da Margem EBITDA deste segmento é consequência direta da queda doLucro Bruto em 46,0% e aumento das Despesas Administrativas em 23,0%.

O EBITDA Ajustado do Segmento Energy Products decresceu 69,2% no 4T09 quandocomparado ao 3T09, e atingiu R$1,3 milhão versus R$4,3 milhões no 3T09. A Margem EBITDAdo Segmento Energy Products alcançou 2,0% no 4T09 versus 5,0% no 3T09. A queda daMargem EBITDA deste segmento é consequência direta da queda do Lucro Bruto em 25,9% eaumento das Despesas com Vendas em 34,2%.

O EBITDA Ajustado do Segmento Flow Control decresceu 45,6% em 2009 quando comparadoa 2008, e atingiu R$30,3 milhões versus R$55,8 milhões em 2008. A Margem EBITDA doSegmento Flow Control alcançou 25,9% em 2009 versus 34,0% em 2008. A queda da MargemEBITDA deste segmento é consequência direta da queda do Lucro Bruto em 37,3% frente apolíticas de preços mais agressivas praticadas durante o ano.

O EBITDA Ajustado do Segmento Flow Control cresceu 4,9% no 4T09 quando comparado ao3T09, e atingiu R$7,8 milhões versus R$7,5 milhões no 3T09. A Margem EBITDA do SegmentoFlow Control alcançou 27,9% no 4T09 versus 25,2% no 3T09. O crescimento da MargemEBITDA deste segmento é consequência do crescimento da depreciação em 4,4%.

O EBITDA Ajustado do Segmento Metalurgia decresceu 136,6% em 2009 quando comparado a2008, e atingiu o montante negativo de R$3,4 milhões versus o montante positivo de R$9,2milhões em 2008. A Margem EBITDA do Segmento Metalurgia alcançou o percentual negativode 6,5% em 2009 versus 10,3% em 2008. A queda da Margem EBITDA deste segmento éconsequência direta da queda do Lucro Bruto em 106,8%.

O EBITDA Ajustado do Segmento Metalurgia atingiu o montante negativo de R$2,2 milhõesversus o montante negativo de R$0,1 milhão no 3T09. A Margem EBITDA do SegmentoMetalurgia alcançou o valor negativo de 16,9% no 4T09 versus o valor negativo de 1,0% no3T09. A queda da Margem EBITDA deste segmento é consequência direta da queda do LucroBruto em 70,8% e aumento das Despesas com Vendas em 6,5%.

Abaixo se encontra a reconciliação do EBITDA Ajustado por segmento, conforme calculadopela Companhia.

[O restante dessa página foi deixado intencionalmente em branco]

24

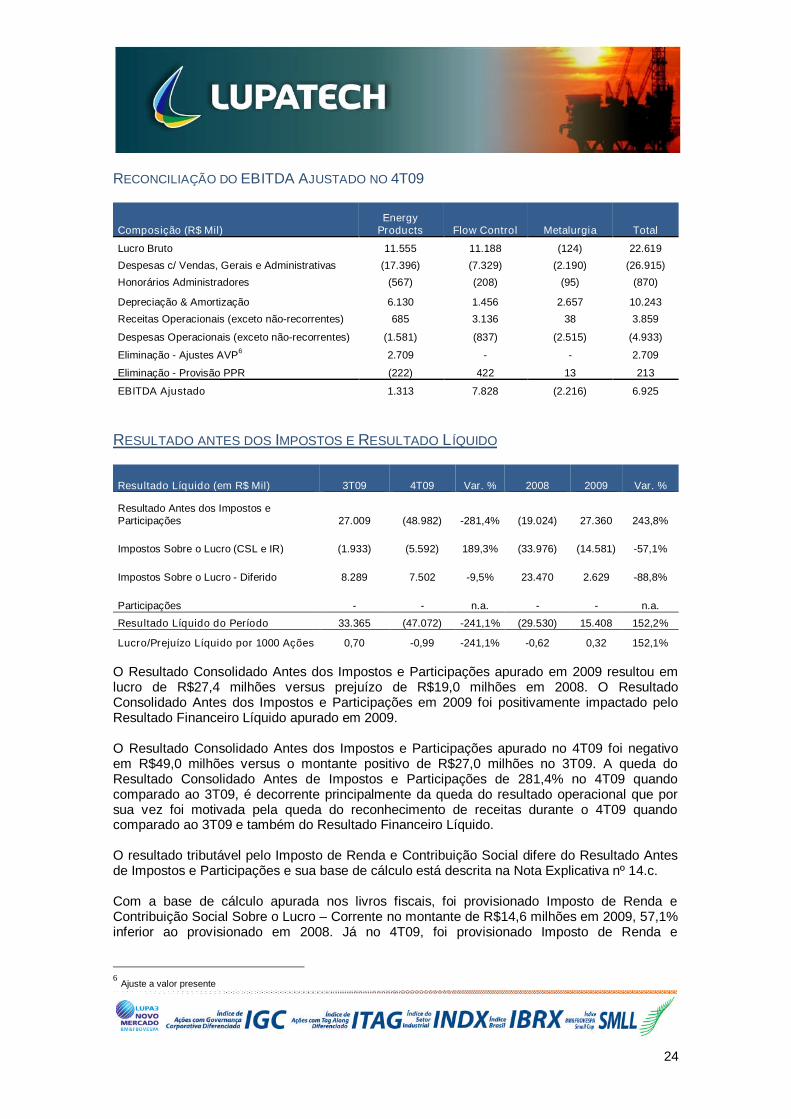

RECONCILIAÇÃO DO EBITDA AJUSTADO NO 4T09

Composição (R$ Mil)Energy

Products Flow Control Metalurgia Total

Lucro Bruto 11.555 11.188 (124) 22.619

Despesas c/ Vendas, Gerais e Administrativas (17.396) (7.329) (2.190) (26.915)

Honorários Administradores (567) (208) (95) (870)

Depreciação & Amortização 6.130 1.456 2.657 10.243

Receitas Operacionais (exceto não-recorrentes) 685 3.136 38 3.859

Despesas Operacionais (exceto não-recorrentes) (1.581) (837) (2.515) (4.933)

Eliminação - Ajustes AVP6

2.709 - - 2.709

Eliminação - Provisão PPR (222) 422 13 213

EBITDA Ajustado 1.313 7.828 (2.216) 6.925

RESULTADO ANTES DOS IMPOSTOS E RESULTADO LÍQUIDO

Resultado Líquido (em R$ Mil) 3T09 4T09 Var. % 2008 2009 Var. %

Resultado Antes dos Impostos eParticipações 27.009 (48.982) -281,4% (19.024) 27.360 243,8%

Impostos Sobre o Lucro (CSL e IR) (1.933) (5.592) 189,3% (33.976) (14.581) -57,1%

Impostos Sobre o Lucro - Diferido 8.289 7.502 -9,5% 23.470 2.629 -88,8%

Participações - - n.a. - - n.a.

Resultado Líquido do Período 33.365 (47.072) -241,1% (29.530) 15.408 152,2%

Lucro/Prejuízo Líquido por 1000 Ações 0,70 -0,99 -241,1% -0,62 0,32 152,1%

O Resultado Consolidado Antes dos Impostos e Participações apurado em 2009 resultou emlucro de R$27,4 milhões versus prejuízo de R$19,0 milhões em 2008. O ResultadoConsolidado Antes dos Impostos e Participações em 2009 foi positivamente impactado peloResultado Financeiro Líquido apurado em 2009.

O Resultado Consolidado Antes dos Impostos e Participações apurado no 4T09 foi negativoem R$49,0 milhões versus o montante positivo de R$27,0 milhões no 3T09. A queda doResultado Consolidado Antes de Impostos e Participações de 281,4% no 4T09 quandocomparado ao 3T09, é decorrente principalmente da queda do resultado operacional que porsua vez foi motivada pela queda do reconhecimento de receitas durante o 4T09 quandocomparado ao 3T09 e também do Resultado Financeiro Líquido.

O resultado tributável pelo Imposto de Renda e Contribuição Social difere do Resultado Antesde Impostos e Participações e sua base de cálculo está descrita na Nota Explicativa nº 14.c.

Com a base de cálculo apurada nos livros fiscais, foi provisionado Imposto de Renda eContribuição Social Sobre o Lucro – Corrente no montante de R$14,6 milhões em 2009, 57,1%inferior ao provisionado em 2008. Já no 4T09, foi provisionado Imposto de Renda e

6Ajuste a valor presente

25

Contribuição Social Sobre o Lucro – Corrente no montante de R$5,6 milhões versus R$1,9milhão no 3T09.

O Lucro Líquido Consolidado de 2009 foi de R$15,4 milhões versus prejuízo de R$29,5 milhõesapurado em 2008. Já no 4T09, o Resultado Líquido Consolidado atingiu prejuízo de R$47,1milhões, versus lucro de R$33,4 milhões no 3T09.

[O restante dessa página foi deixado intencionalmente em branco]

26

COMENTÁRIOS DA ADMINISTRAÇÃO A EVOLUÇÃO DO BALANÇO PATRIMONIAL

Os Comentários da Evolução do Balanço Patrimonial, exceto quando indicado o contrário,referem-se ao exercício de 2009 comparativamente ao exercício de 2008.

CAPITAL DE GIRO OPERACIONAL

Capital de Giro (R$ Mil) 2008 2009 Var. % Variação Nominal

Contas a Receber 264.294 188.116 -28,8% (76.178)

Estoques 195.801 164.015 -16,2% (31.786)

Fornecedores 54.064 35.897 -33,6% (18.167)

Adiantamentos de Clientes 17.564 8.126 -53,7% (9.438)

Capital de Giro Aplicado 388.467 308.108 -20,7% (80.359)

Variação do Capital de Giro Aplicado (80.359)

O saldo das Contas a Receber decresceu R$76,2 milhões em 2009, o que representa 28,8% amenos que o saldo de 2008. A queda do Contas a Receber decorre principalmente de menornível de atividades nos negócios assim como o efetivo recebimento de clientes.

O saldo do Estoque decresceu R$31,8 milhões em 2009, o que representa 16,2% a menos queo saldo de 2008, devido à diminuição dos volumes de compra assim como o efeito da variaçãocambial (R$20,6 milhões) entre o Real e o Peso Argentino que impactou a valorização contábildo saldo de estoque mantido na Argentina.

A conta Fornecedores apresentou queda de R$18,2 milhões em 2009, ou 33,6% sobre o saldode 2008, resultante de menores volumes de compras.

A conta Adiantamentos de Clientes apresentou queda de R$9,4 milhões em 2009, ou queda de53,7% em comparação com 2008. A queda é decorrente de menor atividade comercial emprojetos que trabalham com antecipação dos clientes.

A variação do Capital de Giro Operacional em 2009 resultou em geração de caixa de R$80,4milhões. O índice de Necessidade de Capital de Giro sobre Receita Líquida Consolidada daCompanhia acumulada nos últimos quatro trimestres ficou em 55,5%.

Abaixo encontra-se o gráfico demonstrando a evolução trimestral do uso de capital de girocomo percentual da Receita Líquida Consolidada dos últimos doze meses.

[O restante dessa página foi deixado intencionalmente em branco]

27

UTILIZAÇÃO DE CAPITAL DE GIRO COMO PERCENTUAL DA RECEITA LÍQUIDA ACUMULADA

DOS ÚLTIMOS QUATRO TRIMESTRES

POSIÇÃO DE CAIXA

Caixa (em R$ Mil) 2008 2009 Var. % Variação Nominal

Caixa e Equivalentes de Caixa 316.874 131.160 -58,6% (185.714)

Em função da conclusão do processo de alongamento do perfil da dívida da Companhia, aAdministração decidiu por reduzir a posição de caixa, que ainda assim é excedente aoscompromissos de amortização de juros e dívidas que a Companhia tem para o exercício de2010.

A posição consolidada de Caixa e Equivalentes de Caixa da Companhia em 2009 atingiuR$131,2 milhões. A queda de R$185,7 milhões em comparação com 2008 é justificadaprincipalmente pelo pagamento de aquisições de controladas no montante de R$71,3 milhões,de aquisição de imobilizado no valor de R$54,0 milhões e efeitos cambiais sobre o saldo emcaixa no valor de R$45,0 milhões.

[O restante dessa página foi deixado intencionalmente em branco]

460556

673704

716 719646

555

48,6%45,9%

49,9%

55,2% 56,6%54,8%

60,4%

55,5%

-5%

5%

15%

25%

35%

45%

55%

65%

-

100

200

300

400

500

600

700

800

900

1.000

1T08 2T08 3T08 4T08 1T09 2T09 3T09 4T09

R$ m

Receita Líquida (LTM) % KG sobre Receita Líquida

28

ENDIVIDAMENTO

Endividamento (em R$ Mil) 2008 2009 Var. % Variação Nominal

Curto Prazo 171.727 56.784 -66,9% (114.943)

Longo Prazo 377.978 174.304 -53,9% (203.674)

Debêntures - 340.228 n.a. 340.228

Bônus Perpétuos 634.999 475.023 -25,2% (159.976)

Total do Endividamento 1.184.704 1.046.339 -11,7% (138.365)

Disponibilidades 316.874 131.160 -58,6% (185.714)

Dívida Líquida de Disponibilidades (867.830) (915.179) 5,5% (47.349)

Conforme citado no Relatório da Administração, a Companhia concluiu durante ao fim doexercício de 2009 a reestruturação do perfil de seu endividamento. Esta reestruturação permitiua redução do custo total do endividamento bem como alongamento do prazo médio devencimento, resultando na alteração do saldo total de endividamento, que decresceu 11,7% emcomparação com 2008 atingindo R$1,0 bilhão.

A Dívida Consolidada de Curto Prazo em 2009 atingiu R$56,8 milhões, queda de 66,9%comparada a 2008 decorrente do pagamento de dívidas de curto prazo.

A Dívida de Longo Prazo, que não inclui os Perpetual Bonds e as Debêntures Conversíveis,apresentou queda de 53,9% ou R$203,7 milhões, também decorrente do pré pagamento delinhas de financiamento com vencimentos previstos para 2009 e 2010.

Os recursos utilizados para amortização das linhas de financiamento de curto e longo prazomencionadas acima são oriundos da captação de linhas de crédito junto ao Banco Nacional deDesenvolvimento Econômico e Social (BNDES), sendo R$121 milhões em linhas de repassealocados no longo prazo e R$320 milhões em Debêntures Conversíveis.

O preço de conversão para as Debêntures Conversíveis ainda não foi definido, sendo a datalimite para sua definição o dia 15 de Abril de 2011. Em decorrência da verificação das médiasmóveis, o piso do preço sobre o qual incidirá o prêmio, foi elevado de R$17,50 para R$26,93,reduzindo-se assim o percentual de diluição na hipótese de conversão das DebênturesConversíveis.

O saldo dos Perpetual Bonds em 2009 decresceu 25,2%, atingindo R$475,0 milhões quandocomparado a 2008, consequência da variação cambial verificada no período. A Companhia nãomantém hegde (proteção) para o principal dos Bônus Perpétuos.

Com isso, a Dívida Líquida Consolidada atingiu, no encerramento do exercício de 2009, opatamar de R$915,2 milhões, crescimento de 5,5% contra o exercício de 2008, que decorreessencialmente de redução da posição de caixa.

A Dívida Líquida Consolidada com vencimento (exclui os Bônus Perpétuos), que inclui asDebêntures, alcançou R$571,3 milhões, sendo 59,6% em Debêntures Conversíveis, 9,9% deCurto Prazo e 30,5% de Longo Prazo.

[O restante dessa página foi deixado intencionalmente em branco]

29

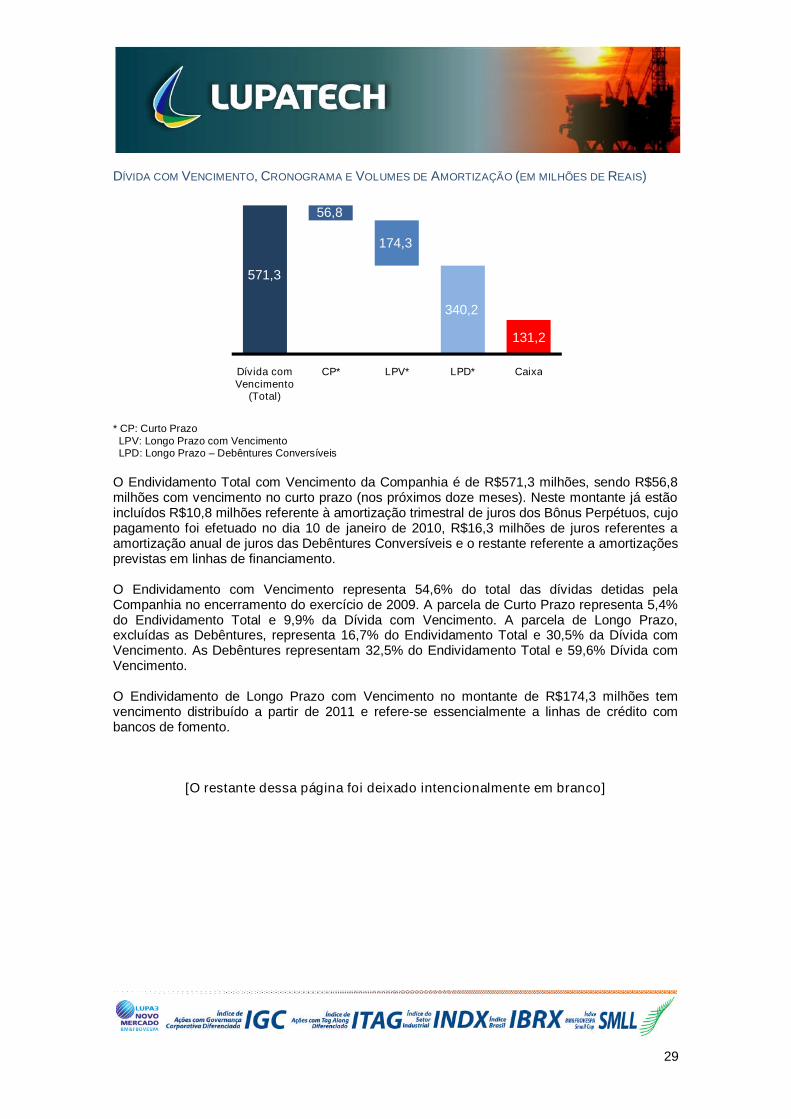

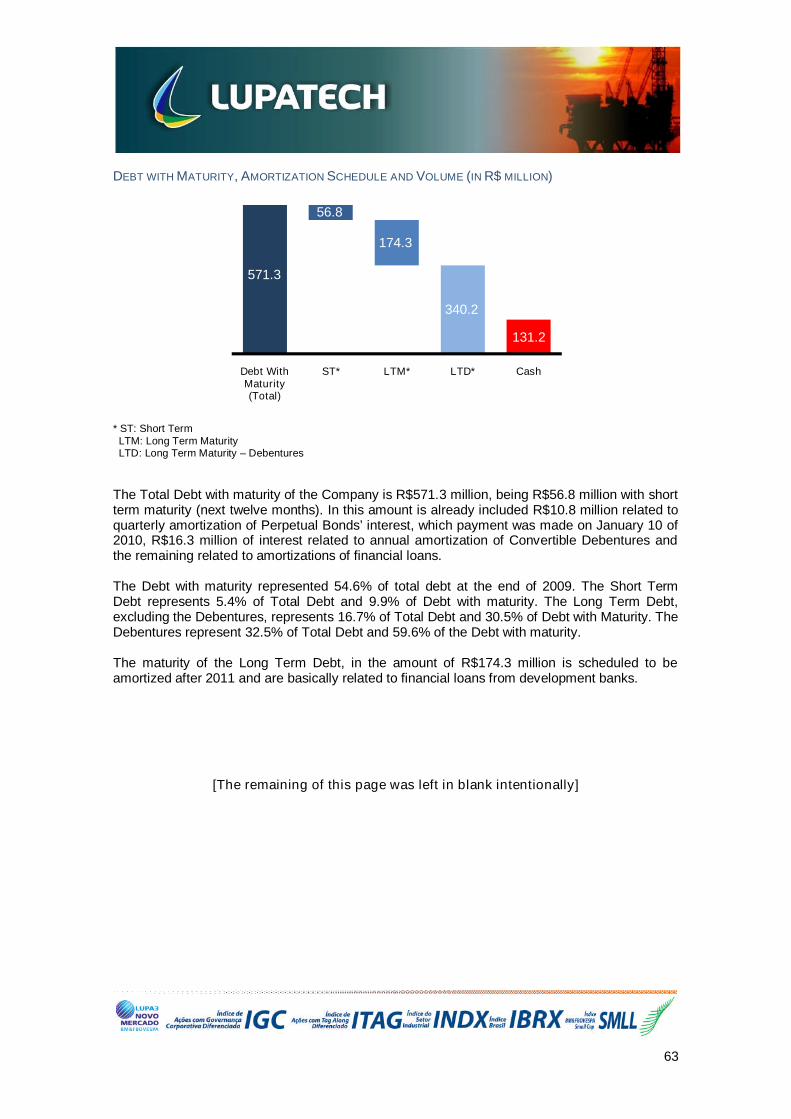

DÍVIDA COM VENCIMENTO, CRONOGRAMA E VOLUMES DE AMORTIZAÇÃO (EM MILHÕES DE REAIS)

* CP: Curto PrazoLPV: Longo Prazo com VencimentoLPD: Longo Prazo – Debêntures Conversíveis

O Endividamento Total com Vencimento da Companhia é de R$571,3 milhões, sendo R$56,8milhões com vencimento no curto prazo (nos próximos doze meses). Neste montante já estãoincluídos R$10,8 milhões referente à amortização trimestral de juros dos Bônus Perpétuos, cujopagamento foi efetuado no dia 10 de janeiro de 2010, R$16,3 milhões de juros referentes aamortização anual de juros das Debêntures Conversíveis e o restante referente a amortizaçõesprevistas em linhas de financiamento.

O Endividamento com Vencimento representa 54,6% do total das dívidas detidas pelaCompanhia no encerramento do exercício de 2009. A parcela de Curto Prazo representa 5,4%do Endividamento Total e 9,9% da Dívida com Vencimento. A parcela de Longo Prazo,excluídas as Debêntures, representa 16,7% do Endividamento Total e 30,5% da Dívida comVencimento. As Debêntures representam 32,5% do Endividamento Total e 59,6% Dívida comVencimento.

O Endividamento de Longo Prazo com Vencimento no montante de R$174,3 milhões temvencimento distribuído a partir de 2011 e refere-se essencialmente a linhas de crédito combancos de fomento.

[O restante dessa página foi deixado intencionalmente em branco]

571,3

56,8

174,3

340,2

131,2

Dívida comVencimento

(Total)

CP* LPV* LPD* Caixa

30

ESTRUTURA DE CAPITAL

As dívidas da Companhia têm vencimento de longo prazo, exceto por uma parcela de 5,4% dototal do endividamento ou 4,3% da estrutura de capital, que vence nos próximos doze meses.Nesse montante já se incluem os juros devidos pelas linhas de longo prazo.

Considerando a parcela dos Perpetual Bonds (fonte estável de financiamento para aCompanhia) no Patrimônio Líquido, observa-se a dívida (com vencimento) representando42,9% do capital empregado na Companhia.

No gráfico acima é possível notar a evolução da estrutura de capital e perfil de endividamentoda Companhia de 2008 para 2009. As dívidas de curto prazo que representavam 11,5% daestrutura de capital em 2008, no encerramento de 2009 representavam apenas 4,3%. Asdívidas de longo prazo que representavam 25,3%, passaram a representar 13,1%. Os BônusPerpétuos, que representavam 42,6% ao final de 2008, em 2009 representaram 35,6% daestrutura de capital da Lupatech.

INVESTIMENTOS (ATIVO PERMANENTE)

Investimentos (em R$ Mil) 2008 2009 Var. % Variação Nominal

Investimentos em Coligadas 2.435 2.386 -2,0% (49)

Imobilizado Líquido 307.156 317.960 3,5% 10.804

Intangível 503.674 506.670 0,6% 2.996

Total 813.265 827.016 1,7% 13.751

Os Investimentos Totais da Companhia em 2009 cresceram 1,7%, atingindo R$827,0 milhõesversus R$813,3 milhões em 2008, devido principalmente a investimentos em compras deimobilizado.

[O restante dessa página foi deixado intencionalmente em branco]

Debêntures25,5%

LP 25,3%

LP 13,1%

CP 11,5%

CP 4,3%

2008 2009

BônusPerpétuos

42,6% Dívida36,8%

Capital20,6%

BônusPerpétuos

35,6%

Capital21,5%

Dívida42,9%

ESTRUTURA DE CAPITAL2008

DÍVIDA COM VENCIMENTO COMOPERCENTUAL DA ESTRUTURA DE

CAPITAL TOTAL

ESTRUTURA DE CAPITAL2009

31

ANEXO I – DEMONSTRAÇÕES DE RESULTADOS (EM R$ MIL)

ANEXO II – RECONCILIAÇÃO DO EBITDA AJUSTADO7 (EM R$ MIL)

[O restante dessa página foi deixado intencionalmente em branco]

7Reconciliado partindo-se do Lucro Líquido Consolidado da Companhia.

Demonstrações do Resultado Consolidado 2009 2008 % Variação

Receita Bruta Vendas e Serviços 627.374 777.721 -19%

Impostos e Deduções da Receita Bruta (72.212) (73.048) -1%

Receita Líquida de Vendas e Serviços 555.162 704.673 -21%

Custo de Bens e Serviços Vendidos (402.996) (418.036) -4%

Resultado Bruto 152.166 286.637 -47%

Receitas/Despesas Operacionais (124.806) (305.661) -59%

Com Vendas (57.170) (60.993) -6%

Gerais e Administrativas (54.722) (49.612) 10%

Resultado Financeiro Líquido (2.519) (194.518) -99%

Receitas Financeiras 189.323 43.495 335%

Despesas Financeiras (191.842) (238.013) -19%

Outras Receitas Operacionais 6.631 6.088 9%

Deságio Aquisição de Investimentos - 5.958 -100%

Outras Despesas Operacionais (17.775) (13.512) 32%

Resultado da Equivalência Patrimonial 749 928 -19%

Resultado Operacional 27.360 (19.024) -244%

Resultados Antes dos Impostos e Participações 27.360 (19.024) -244%

Provisão para IR e Contribuição Social (14.581) (33.976) -57%

IR Diferido 2.629 23.470 -89%

Participação Minoritária - - n.a.

Resultado Líquido do Período 15.408 (29.530) 152%

Reconciliação do EBITDA Ajustado 2009 2008 % Variação

EBITDA Ajustado 81.572 209.708 -61%

Depreciação e Amortização (36.227) (23.607) 53%

Deságio realizado 0 5.958 n.a.

Despesas operacionais não recorrentes (7.187) (6.970) 3%

Despesas operacionais* (8.006) (2.265) 253%

Resultado Financeiro Líquido (2.519) (194.518) -99%

Imposto de Renda e Contribuição Social (14.581) (33.976) -57%

Imposto de Renda e CS - Diferidos 2.629 23.470 140%

Verbas trabalhistas (1.021) (8.258) -88%

Resultado da Equivalência Patrimonial 749 928 -19%Lucro Líquido 15.408 (29.530) 152%

*Despesas Não-Caixa referente ao Programa de Opções de Ações (stock option) e Ajuste a Valor Presente

32

ANEXO III – BALANÇO PATRIMONIAL (EM R$ MIL)

[O restante dessa página foi deixado intencionalmente em branco]

Balanço Patrimonial Consolidado (R$ mil) 2009 2008 % Variação

Ativo Total 1.477.442 1.729.699 -15%

Ativo Circulante 554.419 836.153 -34%

Disponibilidades 131.160 316.874 -59%

Caixa 131.160 316.874 -59%

Créditos 230.194 313.874 -27%

Clientes 184.659 262.062 -30%

Créditos Diversos 45.535 51.812 -12%

Impostos a Recuperar 45.535 51.812 -12%

Estoques 164.015 195.801 -16%

Outros 29.050 9.604 202%

Ativo Não Circulante 923.023 893.546 3%

Créditos Diversos 90.811 57.601 58%

Depósitos Judiciais 1214 5988 -80%

Clientes 3.457 2.232 55%

Impostos a Recuperar 23.432 10.544 122%

Imposto de Renda e Contribuição Social Diferido 62.708 38.837 61%

Outros 5.196 22.680 -77%

Investimentos 2.386 2.435 -2%

Imobilizado 317.960 307.156 4%

Intangível 506.670 503.674 1%

Passivo Total 1.477.442 1.729.699 -15%

Passivo Circulante 150.572 381.727 -61%

Empréstimos e Financiamentos 29.711 157.814 -81%

Juros Bônus Perpétuos 10.760 13.913 -23%

Juros de Debêntures 16.313 - n.a.

Fornecedores 35.897 54.064 -34%

Impostos, Taxas e Contribuições 17.648 28.152 -37%

Dividendos a Pagar - - n.a.

Provisões 8.782 8.614 2%

Dívidas com Pessoas Ligadas - - n.a.

Outros 31.461 119.170 -74%

Contas a pagar c/ Aquis. de Investimentos 2.240 78.620 n.a.

Salários a Pagar 5.398 4.979 8%

Adiantamento de Clientes 8.126 17.564 -54%

Participações no resultado 930 7.132 -87%

Outros 14.767 10.875 36%

Passivo Não Circulante 1.039.610 1.041.346 0%

Empréstimos e Financiamentos 174.304 377.978 -54%

Bônus Perpétuos 475.023 634.999 -25%

Debêntures 340.228 - n.a.

Provisões 42.682 27.195 57%

Provisão para Contingência 7.860 13.615 -42%

Imposto de Renda e Contr. Social Diferido 34.822 13.580 156%

Outros 7.373 1.174 528%

Part. De Acionistas Não Controladores - - n.a.

Patrimônio Líquido 287.260 306.626 -6%

Capital Social Realizado 311.525 309.850 1%

Reservas de Reavaliação - - n.a.

Reservas de Capital 11.002 7.516 46%

Reservas de Lucro - - n.a.

Ajustes de Avaliação Patrimonial (30.497) 9.438 -423%

Prejuízos Acumulados (4.770) (20.178) -76%

33

ANEXO IV – FLUXO DE CAIXA (EM R$ MIL)

[O restante dessa página foi deixado intencionalmente em branco]

Fluxo de Caixa Consolidado Findos em: 2009 2008 % Variação

Lucro líquido/prejuízo do período 15.408 (29.530) 255%

Ajustes para conciliar o resultado as disponibilidades geradas pelas atividades operacionais

Depreciação do imobilizado 36.227 23.607 53%

Deságio na aquisição de investimento - (5.958) n.a.

Resultado da Equivalência Patrimonial (749) (928) -19%

Custo na baixa ou alienação de ativo permanente 706 13.162 -95%

Encargos Financeiros e Variação Cambial 11.702 225.416 -95%

Despesas com opções outorgadas 3.486 2.532 38%

Imposto de renda e contribuição social diferido (2.629) (23.470) -89%

Variações nos ativos e passivos 32.574 (157.770) -121%

(Aumento) redução em contas a receber 55.703 (119.922) -146%

(Aumento) redução em estoques 9.415 (45.685) -121%

(Aumento) redução em impostos a recuperar (12.311) (26.784) -54%

(Aumento) redução em outros ativos 751 11.542 -93%

Aumento (redução) em fornecedores (11.988) 571 -2199%

Aumento (redução) em impostos a recolher (6.221) 4.429 -240%

Aumento (redução) em outras contas a pagar (2.775) 18.079 -115%

Disponibilidades líquidas aplicadas nas atividades operacionais 96.725 47.061 106%

Fluxos de caixa das atividades de investimentos

Investimentos (77.876) (105.372) -26%

Aquisição de imobilizado (54.014) (124.928) -57%

Adições ao Intangível (4.589) (6.437) -29%

Recebimento por venda de imobilizado - - n.a.

Títulos e valores mobiliários - conta restrita - (18.844) n.a.

Disponibilidades líquidas aplicadas nas atividades de investimento (136.479) (255.581) -47%

Fluxos de caixa das atividades de financiamentos

Captação de empréstimos e financiamentos 136.760 332.267 -59%

Captação de debêntures 328.631 - n.a.

Captação de Bônus Perpétuos - 118.900 n.a.

Integralização de capital 1.675 2.339 -28%

Pagamento de empréstimos e financiamentos (567.978) (224.813) 153%

Efeitos das oscilações de câmbio sobre o caixa e equivalentes de caixa (45.048) 58.385 -177%

de controladas no exterior

Disponibilidades líquidas geradas (aplicadas) nas atividades de financiamento (100.912) 228.693 -144%

Aumento (redução) nas disponibilidades (185.714) 78.558 -336%

No início do exercício 316.874 238.316 33%

No final do exercício 131.160 316.874 -59%

34

CONTATOS – RELAÇÕES COM INVESTIDORES

Thiago Alonso de Oliveira Cynthia BurinCFO & IRO Gerente de RI

Telefone: + 55 (11) 2134-7000 ou + 55 (11) 2134-7088Email: [email protected]

SOBRE A LUPATECH

A Lupatech S.A. possui três segmentos de negócios: Energy Products, Flow Control eMetalurgia. No Segmento Energy Products oferece produtos de alto valor agregado eserviços para a indústria de petróleo e gás, como cabos para ancoragem de plataformas emáguas profundas, válvulas, equipamentos para exploração de poços, revestimentos de tubos,compressores para GNV, sensores e serviços, através das marcas “Lupatech MNA”, “LupatechCSL”, “Lupatech Tecval”, “Lupatech Oil Tools”, “Lupatech Esferomatic”, “Lupatech Oil & GasServices”, “Lupatech Tubular Services”, “Lupatech Monitoring Systems”, “Aspro”, “Sinergás” e“Norpatagonica”. No Segmento Flow Control possui posição de liderança no Mercosul naprodução e comercialização de válvulas industriais, principalmente para as indústrias química,farmacêutica, papel e celulose e construção civil, através das marcas “Lupatech Valmicro”,“Lupatech Mipel”, “ValBol” e “Jefferson”. No Segmento de Metalurgia ocupa posição dedestaque no mercado internacional e especializa-se no desenvolvimento e na produção depeças, partes complexas e subconjuntos direcionados principalmente para a indústriaautomotiva mundial através dos processos de fundição de precisão e de injeção de aço, onde éa pioneira na América Latina. Opera, ainda, na fundição de peças em ligas metálicas com altaresistência a corrosão, voltadas para os setores de válvulas industriais e bombas,principalmente para aplicações nos processos para a indústria de petróleo e gás, através dasmarcas “Microinox”, “Steelinject” e “Itasa”.

A Companhia não faz declarações sobre eventos futuros que estão sujeitas a riscos e incertezas. Tais declarações têm como base estimativas e suposiçõesda Administração e informações a que a Companhia atualmente tem acesso. Declarações sobre eventos futuros incluem informações sobre suas intenções,estimattivas ou expectativas atuais, assim como aquelas dos membros do Conselho de Administração e Diretores da Companhia. As ressalvas com relação adeclarações e informações acerca do futuro também incluem informações sobre resultados operacionais possíveis ou presumidos, bem como declarações quesão precedidas, seguidas ou que incluem as palavras "acredita", "poderá", "irá", "continua", "espera", "prevê", "pretende", "planeja", "estima" ou expressõessemelhantes. As declarações e informações sobre o futuro não são garantias de desempenho. Elas envolvem riscos, incertezas e suposições porque sereferem a eventos futuros, dependendo, portanto, de circunstâncias que poderão ocorrer ou não. Os resultados futuros e a criação de valor para os acionistaspoderão diferir de maneira significativa daqueles expressos ou estimados pelas declarações com relação ao futuro. Muitos dos fatores que irão determinarestes resultados e valores estão além da capacidade de controle ou previsão da Lupatech

35

LUPATECH’S NET PROFIT REACHES

R$15.4 MILLION IN 2009

Caxias do Sul, March 29, 2010 – Lupatech S.A. (BM&FBovespa: LUPA3) (OTCQX: LUPAY)

(“Lupatech” or “Company”), leading manufacturer of industrial valves in Mercosul and producer

of equipment for the oil and gas sector and parts for the automotive chain, announces its results

for the fourth quarter of 2009 (4Q09) and 2009. The Company’s consolidated annual financial

statements are drawn up in line with the International Financial Reporting Standards (IFRS).

The comparisons, except when otherwise indicated, refers to the third quarter of 2009 (3Q09)

and to the 2008 results.

CONFERENCE CALLS – 4Q09

ENGLISH – ASIAN INVESTORS

Date: March 31, 2010Time: 09:30 am (HKT) / 10:30 p.m. (Brasilia) of 03/30Telephone: +1 412 858 4600Code: Lupatech

PORTUGUESE

Date: March 31, 2010Time: 09:00 a.m. (US-ET) / 10:00 a.m. (Brasilia)Telephone: + 55 11 2188 0188Code: Lupatech

ENGLISH

Date: March 31, 2010Time: 11:00 a.m. (US-ET) / 12:00 p.m. (Brasilia)Telephone: + 1 412 858 4600Code: Lupatech

INVESTOR RELATIONS - CONTACTS

Thiago Alonso de Oliveira - CFO & IROCynthia Burin – IR Manager

Telephone: + 55 (11) 2134-7000 or + 55 (11) 2134-7088Email: [email protected] : www.twitter.com/LupatechSA

Press Relations: MZ Consult +55 11 3529-3800

36

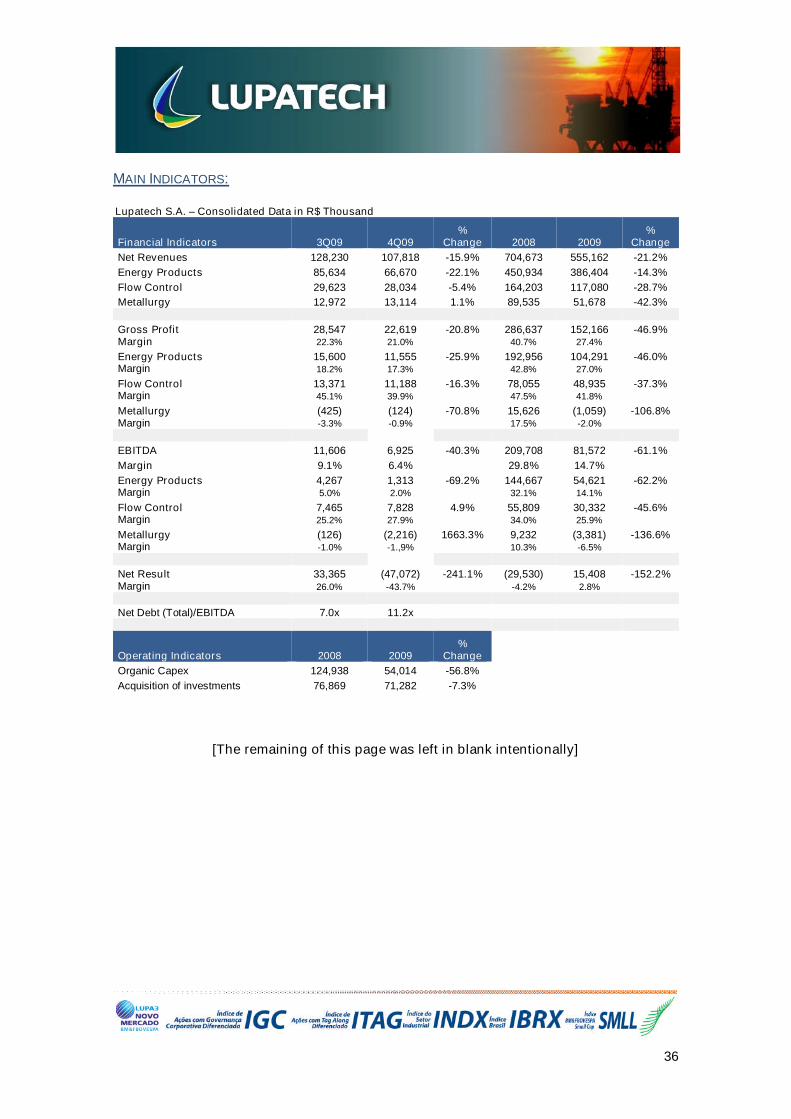

MAIN INDICATORS:

Lupatech S.A. – Consolidated Data in R$ Thousand

Financial Indicators 3Q09 4Q09%

Change 2008 2009%

Change

Net Revenues 128,230 107,818 -15.9% 704,673 555,162 -21.2%

Energy Products 85,634 66,670 -22.1% 450,934 386,404 -14.3%

Flow Control 29,623 28,034 -5.4% 164,203 117,080 -28.7%

Metallurgy 12,972 13,114 1.1% 89,535 51,678 -42.3%

Gross Profit 28,547 22,619 -20.8% 286,637 152,166 -46.9%Margin 22.3% 21.0% 40.7% 27.4%

Energy Products 15,600 11,555 -25.9% 192,956 104,291 -46.0%Margin 18.2% 17.3% 42.8% 27.0%

Flow Control 13,371 11,188 -16.3% 78,055 48,935 -37.3%Margin 45.1% 39.9% 47.5% 41.8%

Metallurgy (425) (124) -70.8% 15,626 (1,059) -106.8%Margin -3.3% -0.9% 17.5% -2.0%

EBITDA 11,606 6,925 -40.3% 209,708 81,572 -61.1%

Margin 9.1% 6.4% 29.8% 14.7%

Energy Products 4,267 1,313 -69.2% 144,667 54,621 -62.2%Margin 5.0% 2.0% 32.1% 14.1%

Flow Control 7,465 7,828 4.9% 55,809 30,332 -45.6%Margin 25.2% 27.9% 34.0% 25.9%

Metallurgy (126) (2,216) 1663.3% 9,232 (3,381) -136.6%Margin -1.0% -1.,9% 10.3% -6.5%

Net Result 33,365 (47,072) -241.1% (29,530) 15,408 -152.2%Margin 26.0% -43.7% -4.2% 2.8%

Net Debt (Total)/EBITDA 7.0x 11.2x

Operating Indicators 2008 2009%

Change

Organic Capex 124,938 54,014 -56.8%

Acquisition of investments 76,869 71,282 -7.3%

[The remaining of this page was left in blank intentionally]

37

38

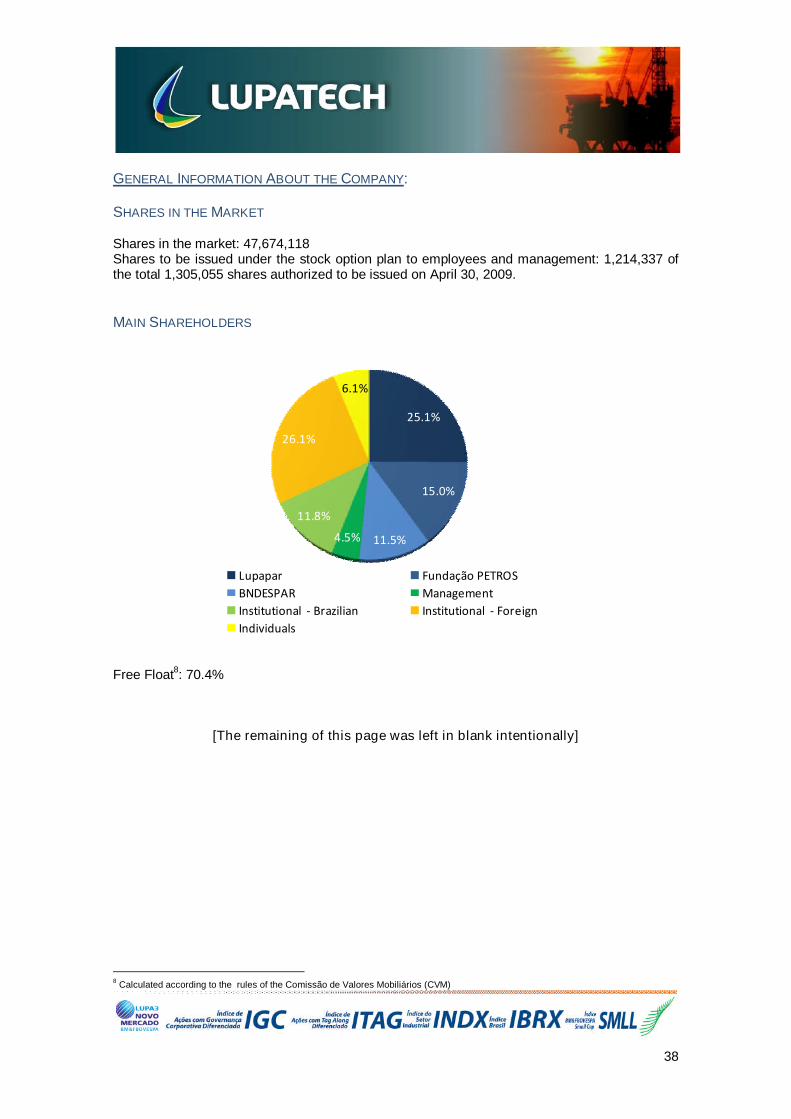

GENERAL INFORMATION ABOUT THE COMPANY:

SHARES IN THE MARKET

Shares in the market: 47,674,118Shares to be issued under the stock option plan to employees and management: 1,214,337 ofthe total 1,305,055 shares authorized to be issued on April 30, 2009.

MAIN SHAREHOLDERS

Free Float8: 70.4%

[The remaining of this page was left in blank intentionally]

8Calculated according to the rules of the Comissão de Valores Mobiliários (CVM)

25.1%

15.0%

11.5%4.5%

11.8%

26.1%

6.1%

Lupapar Fundação PETROS

BNDESPAR Management

Institutional - Brazilian Institutional - Foreign

Individuals

39

Dear Sirs,

Lupatech S.A. (“Company”) presents the Management Report and the Company’s ConsolidatedAnnual Financial Statements for the fiscal year ended on December 31, 2009 for yourappreciation.

It is recommended to read this material together with the Notes to the Consolidated FinancialStatements.

COMPANY AND BUSINESS PROFILE

Lupatech S.A. has three business segments: Energy Products9, Flow Control

10and

Metallurgy11

, and around 2,971 employees.

The Energy Products Segment offers high value-added products and services for the Oil &Gas sector, including deepwater platform anchoring ropes, valves, oil wells completion tools,coating, VNG compressors, sensors and services through “Lupatech MNA”, “Lupatech CSL”,“Lupatech Tecval”, “Lupatech Oil Tools”, “Lupatech Esferomatic”, “Lupatech Oil & GasServices”, “Lupatech Tubular Services”, “Lupatech Monitoring Systems”, “Aspro”, “Sinergás”and “Norpatagonica” brands.

The Flow Control Segment heads the national rankings in the Mercosul in the production andsale of industrial valves, primarily for the chemical, pharmaceutical, pulp and paper andconstruction industries, under “Lupatech Valmicro”, “Lupatech Mipel”, “ValBol” and “Jefferson”brands.

The Metallurgy Segment is among the international leaders in the development and productionof parts, complex parts and sub-assemblies, mainly for power train systems to the global autoindustry. It employs the precision casting and steel injection processes, techniques that itpioneered in Latin America. It also produces high-corrosion-resistant cast-alloy housings forindustrial valves and pumps, chiefly for applications in the oil and gas industry under“Microinox”, “Steelinject” and “Itasa” brands.

[The remaining of this page was left in blank intentionally]

9Former Oil & Gas

10Former Flow

11Former Metal

40

MESSAGE TO SHAREHOLDERS AND MARKET AGENTS

Dear shareholders and market agents,