institutional presentation (eng) march 2015 finalv1

TRANSCRIPT

Institutional PresentationMarch 2015

2

This information is property of Wilson Sons and can not be used or reproduced without written permission

Disclaimer

This presentation contains statements that may constitute “forward-looking statements”, based on

current opinions, expectations and projections about future events. Such statements are also based on

assumptions and analysis made by Wilson, Sons and are subject to market conditions which are

beyond the Company’s control.

Important factors which may lead to significant differences between real results and these forward-

looking statements are: national and international economic conditions; technology; financial market

conditions; uncertainties regarding results in the Company’s future operations, its plans, objectives,

expectations, intentions; and other factors described in the section entitled "Risk Factors“, available in

the Company’s Prospectus, filed with the Brazilian Securities and Exchange Commission (CVM).

The Company’s operating and financial results, as presented on the following slides, were prepared in

conformity with International Financial Reporting Standards (IFRS), except as otherwise expressly

indicated. An independent auditors’ review report is an integral part of the Company’s condensed

consolidated financial statements.

3

This information is property of Wilson Sons and can not be used or reproduced without written permission

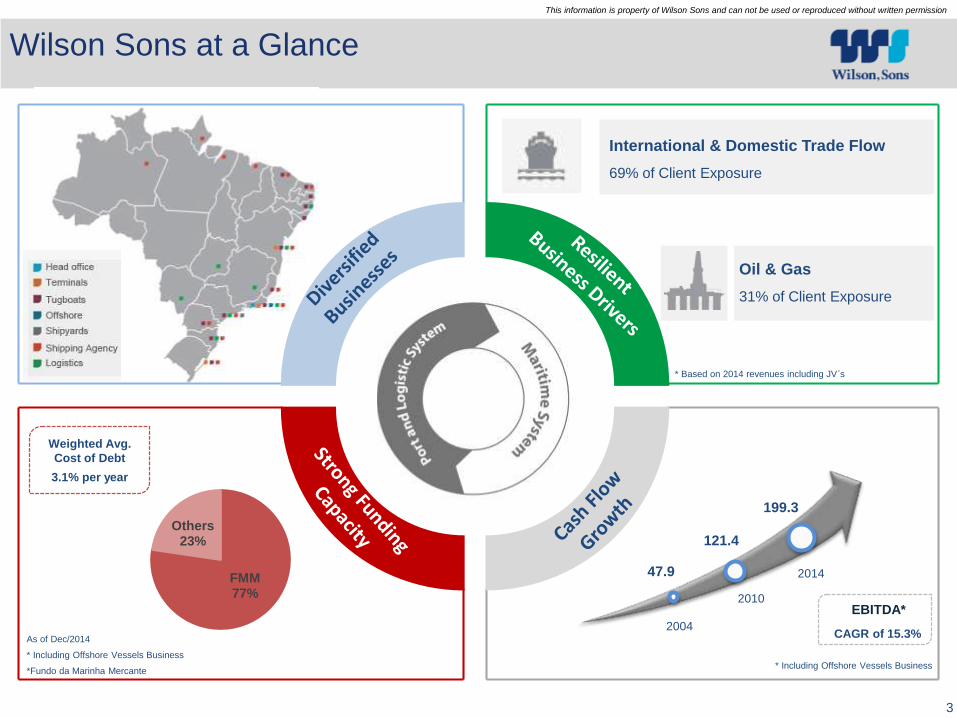

FMM77%

Others23%

International & Domestic Trade Flow

69% of Client Exposure

Wilson Sons at a Glance

*Fundo da Marinha Mercante

Oil & Gas

31% of Client Exposure

Weighted Avg.

Cost of Debt

3.1% per year

As of Dec/2014

* Based on 2014 revenues including JV´s

199.3

47.9

2004

2014

CAGR of 15.3%

121.4

2010EBITDA*

* Including Offshore Vessels Business* Including Offshore Vessels Business

Our Growth Drivers

5

This information is property of Wilson Sons and can not be used or reproduced without written permission

International & Domestic Trade Flow

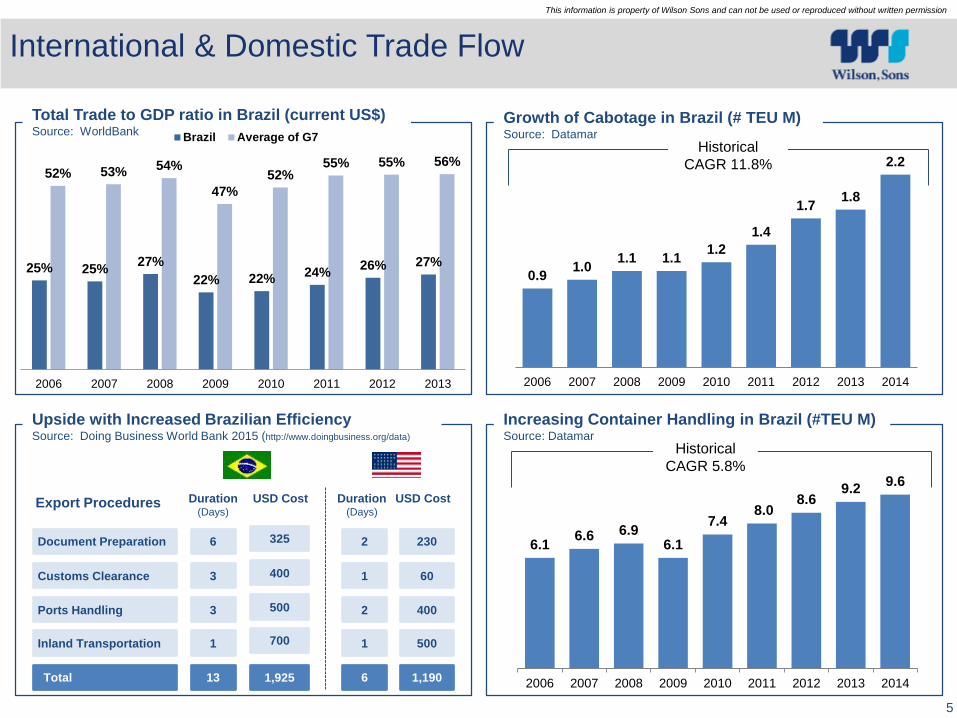

Document Preparation

Customs Clearance

Ports Handling

Inland Transportation

Duration(Days)

USD Cost

6

3

3

1

325

400

500

700

Total 13 1,925

2

1

2

1

6

230

60

400

500

1,190

Duration(Days)

USD CostExport Procedures

Total Trade to GDP ratio in Brazil (current US$)Source: WorldBank

Growth of Cabotage in Brazil (# TEU M)Source: Datamar

Upside with Increased Brazilian EfficiencySource: Doing Business World Bank 2015 (http://www.doingbusiness.org/data)

Increasing Container Handling in Brazil (#TEU M)Source: Datamar

Historical

CAGR 5.8%

Historical

CAGR 11.8%

25% 25%27%

22% 22%24%

26% 27%

52% 53%54%

47%

52%55% 55% 56%

2006 2007 2008 2009 2010 2011 2012 2013

Brazil Average of G7

0.91.0

1.1 1.11.2

1.4

1.71.8

2.2

2006 2007 2008 2009 2010 2011 2012 2013 2014

6.16.6 6.9

6.1

7.48.0

8.69.2

9.6

2006 2007 2008 2009 2010 2011 2012 2013 2014

6

This information is property of Wilson Sons and can not be used or reproduced without written permission

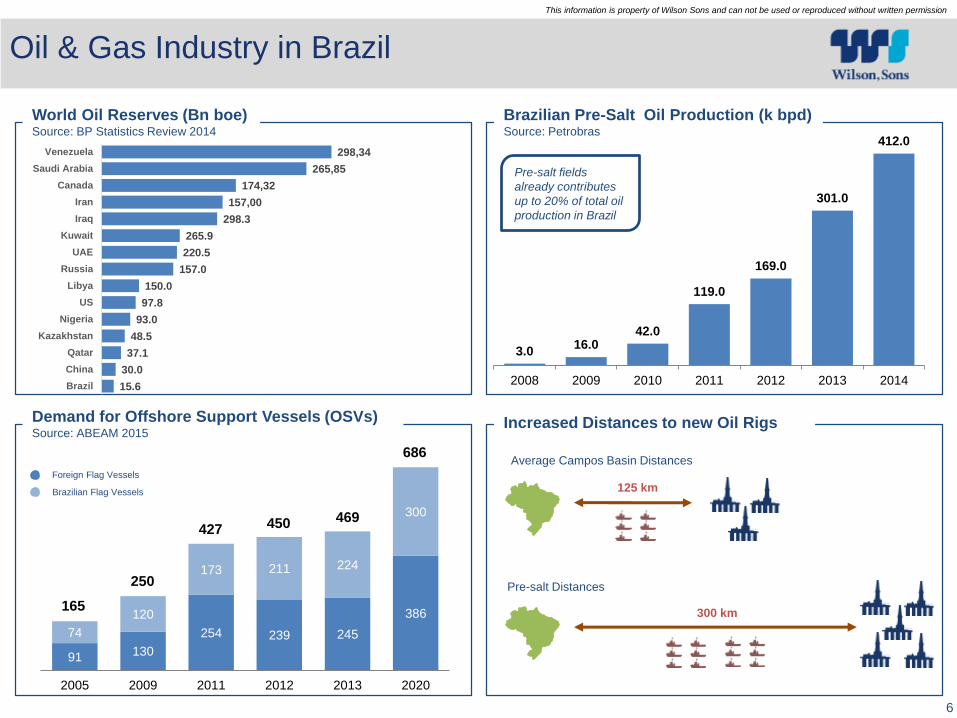

3.016.0

42.0

119.0

169.0

301.0

412.0

2008 2009 2010 2011 2012 2013 2014

Oil & Gas Industry in Brazil

World Oil Reserves (Bn boe)Source: BP Statistics Review 2014

Brazilian Pre-Salt Oil Production (k bpd)Source: Petrobras

Demand for Offshore Support Vessels (OSVs)Source: ABEAM 2015

Increased Distances to new Oil Rigs

125 km

300 km

Average Campos Basin Distances

Pre-salt Distances

Foreign Flag Vessels

Brazilian Flag Vessels

Pre-salt fields

already contributes

up to 20% of total oil

production in Brazil

91 130

254 239 245

386

74

120

173 211 224

300

2005 2009 2011 2012 2013 2020

250

427 450 469

686

165

15.6

30.0

37.1

48.5

93.0

97.8

150.0

157.0

220.5

265.9

298.3

157,00

174,32

265,85

298,34

Brazil

China

Qatar

Kazakhstan

Nigeria

US

Libya

Russia

UAE

Kuwait

Iraq

Iran

Canada

Saudi Arabia

Venezuela

Our Business

8

This information is property of Wilson Sons and can not be used or reproduced without written permission

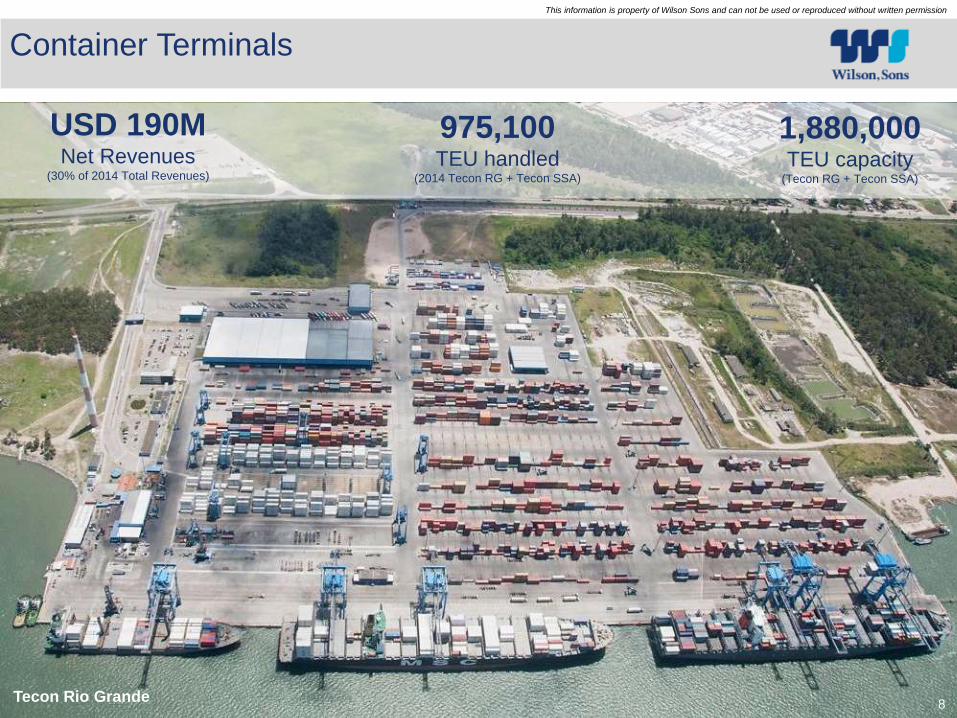

Container Terminals

Tecon Rio Grande8

975,100TEU handled

(2014 Tecon RG + Tecon SSA)

1,880,000TEU capacity

(Tecon RG + Tecon SSA)

USD 190MNet Revenues

(30% of 2014 Total Revenues)

9

This information is property of Wilson Sons and can not be used or reproduced without written permission

Container Terminals

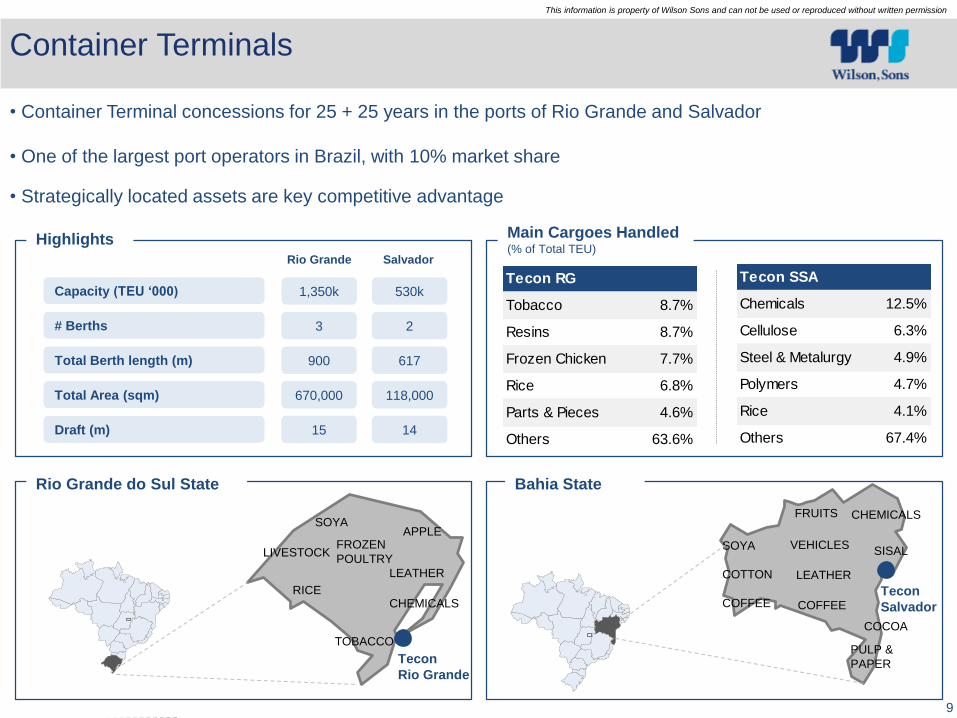

• Container Terminal concessions for 25 + 25 years in the ports of Rio Grande and Salvador

• One of the largest port operators in Brazil, with 10% market share

• Strategically located assets are key competitive advantage

Rio Grande do Sul State

Highlights Main Cargoes Handled (% of Total TEU)

Total Berth length (m)

# Berths

Total Area (sqm)

900

3

670,000

617

2

118,000

Rio Grande Salvador

Draft (m) 15 14

Capacity (TEU ‘000) 1,350k 530k

Bahia State

RICE

TOBACCO

APPLE

LIVESTOCK

SOYA

LEATHER

CHEMICALS

Tecon

Rio Grande

FROZEN

POULTRYSOYA

COTTON

COFFEE

FRUITS

COFFEE

PULP &

PAPER

COCOA

LEATHER

VEHICLES

Tecon

Salvador

CHEMICALS

SISAL

Tecon RG

Tobacco 8.7%

Resins 8.7%

Frozen Chicken 7.7%

Rice 6.8%

Parts & Pieces 4.6%

Others 63.6%

Tecon SSA

Chemicals 12.5%

Cellulose 6.3%

Steel & Metalurgy 4.9%

Polymers 4.7%

Rice 4.1%

Others 67.4%

10

This information is property of Wilson Sons and can not be used or reproduced without written permission

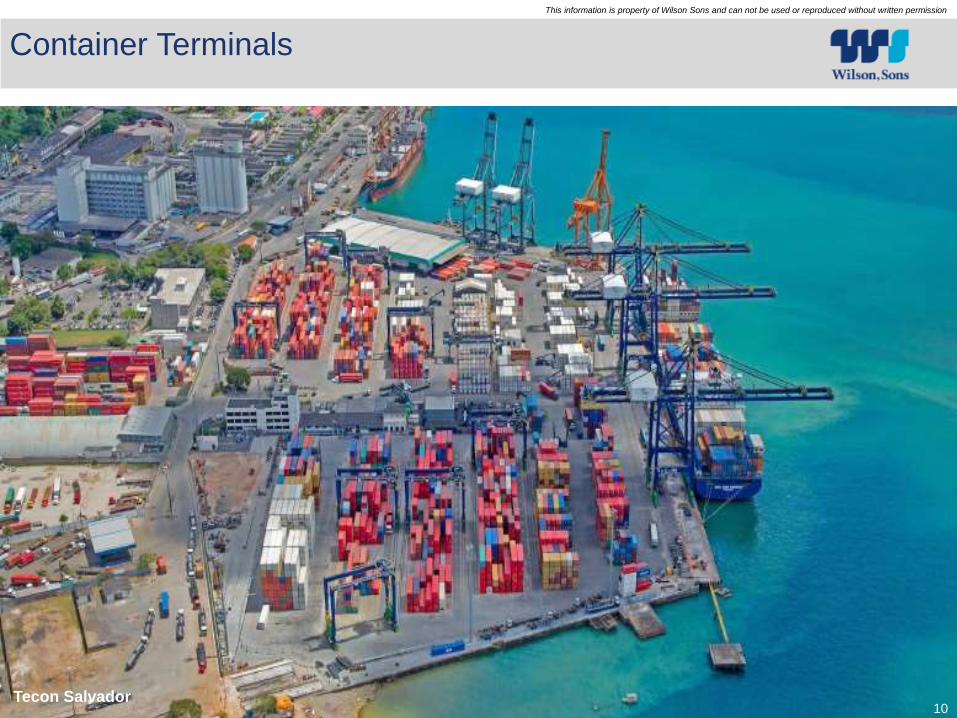

Container Terminals

10Tecon Salvador

11

This information is property of Wilson Sons and can not be used or reproduced without written permission

Container Terminals

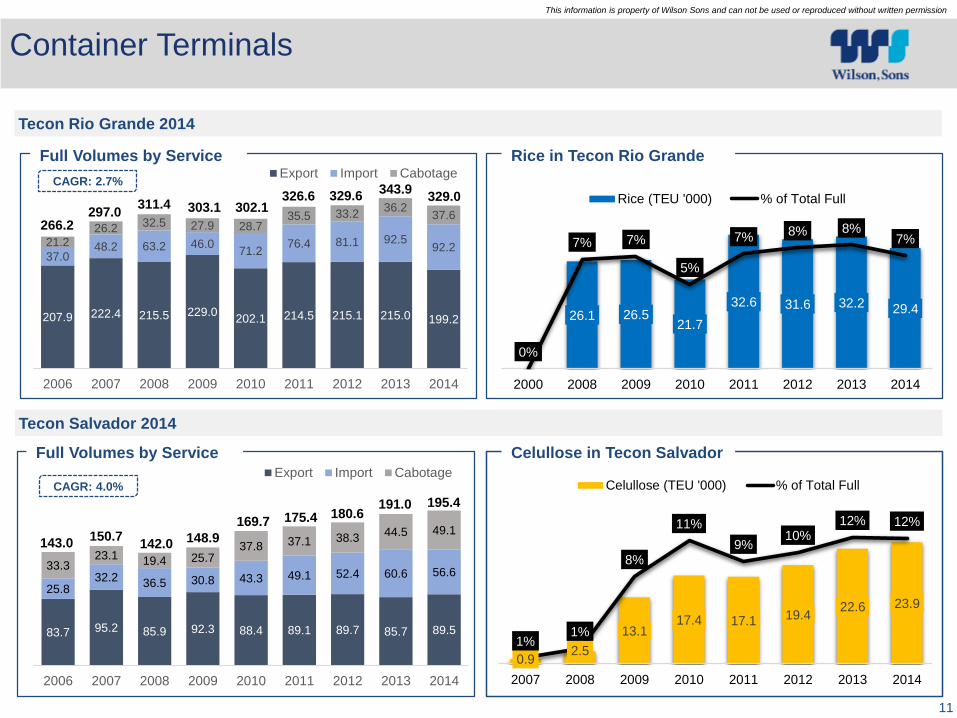

Rice in Tecon Rio GrandeFull Volumes by Service

Tecon Rio Grande 2014

Tecon Salvador 2014

Celullose in Tecon SalvadorFull Volumes by Service

83,7 95,2 86,0 92,3 88,5 89,1 89,7 85,8

25,932,3

36,6 30,8 43,3 49,1 52,5 60,733,4

23,219,4 25,7

37,9 37,1 38,444,6

2006 2007 2008 2009 2010 2011 2012 2013

Export Import Cabotage

143,0150,7

142,0148,9

169,7 175,4 180,6191,0

83,7 95,2 86,0 92,3 88,5 89,1 89,7 85,8

25,932,3

36,6 30,8 43,3 49,1 52,5 60,733,4

23,219,4 25,7

37,9 37,1 38,444,6

2006 2007 2008 2009 2010 2011 2012 2013

Export Import Cabotage

143,0150,7

142,0148,9

169,7 175,4 180,6191,0

207.9 222.4 215.5 229.0202.1 214.5 215.1 215.0 199.2

37.048.2 63.2 46.0

71.276.4 81.1 92.5

92.221.226.2 32.5 27.9 28.7

35.5 33.236.2

37.6

2006 2007 2008 2009 2010 2011 2012 2013 2014

266.2297.0

311.4 303.1 302.1326.6 329.6 329.0

343.9

83.7 95.2 85.9 92.3 88.4 89.1 89.7 85.7 89.5

25.832.2

36.5 30.8 43.3 49.1 52.4 60.6 56.633.3

23.1 19.4 25.737.8 37.1 38.3

44.5 49.1

2006 2007 2008 2009 2010 2011 2012 2013 2014

143.0150.7

142.0 148.9

169.7 175.4 180.6195.4191.0

CAGR: 4.0%

CAGR: 2.7%

26.1 26.521.7

32.6 31.6 32.2 29.4

0%

7% 7%

5%

7% 8% 8%7%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2000 2008 2009 2010 2011 2012 2013 2014

Rice (TEU '000) % of Total Full

0.92.5

13.117.4 17.1 19.4

22.6 23.9

1%1%

8%

11%

9%10%

12% 12%

0%

2%

4%

6%

8%

10%

12%

14%

0.0

5.0

10.0

15.0

20.0

25.0

30.0

2007 2008 2009 2010 2011 2012 2013 2014

Celullose (TEU '000) % of Total Full

12

This information is property of Wilson Sons and can not be used or reproduced without written permission

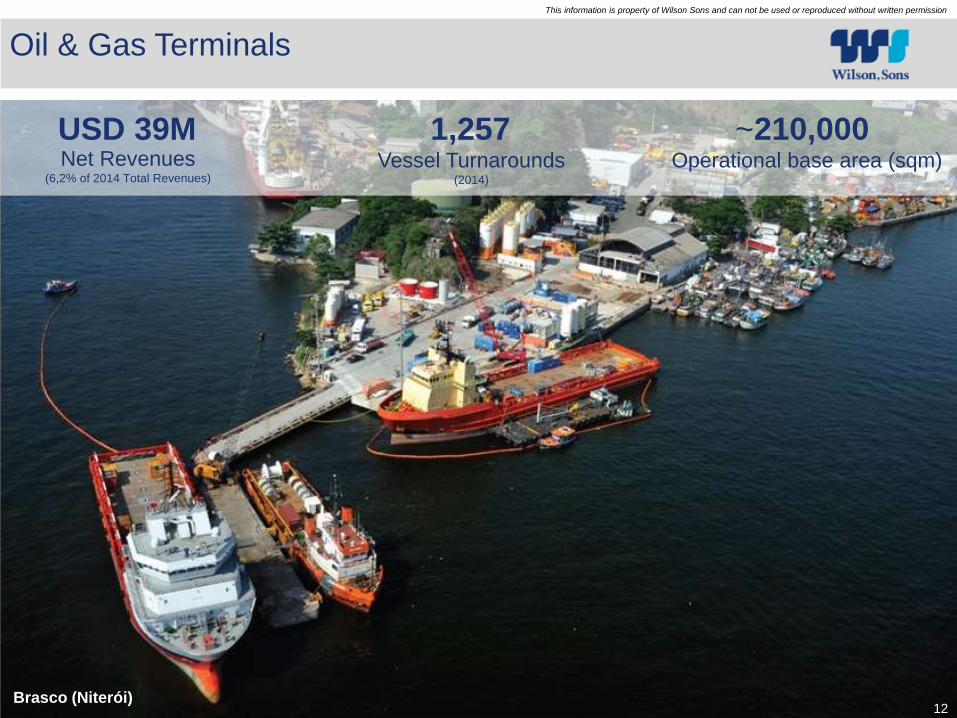

Oil & Gas Terminals

Brasco (Niterói)12

1,257Net Revenues

(6,2% of 2014 Total Revenues)

Vessel Turnarounds (2014)

~210,000Operational base area (sqm)

USD 39M

13

This information is property of Wilson Sons and can not be used or reproduced without written permission

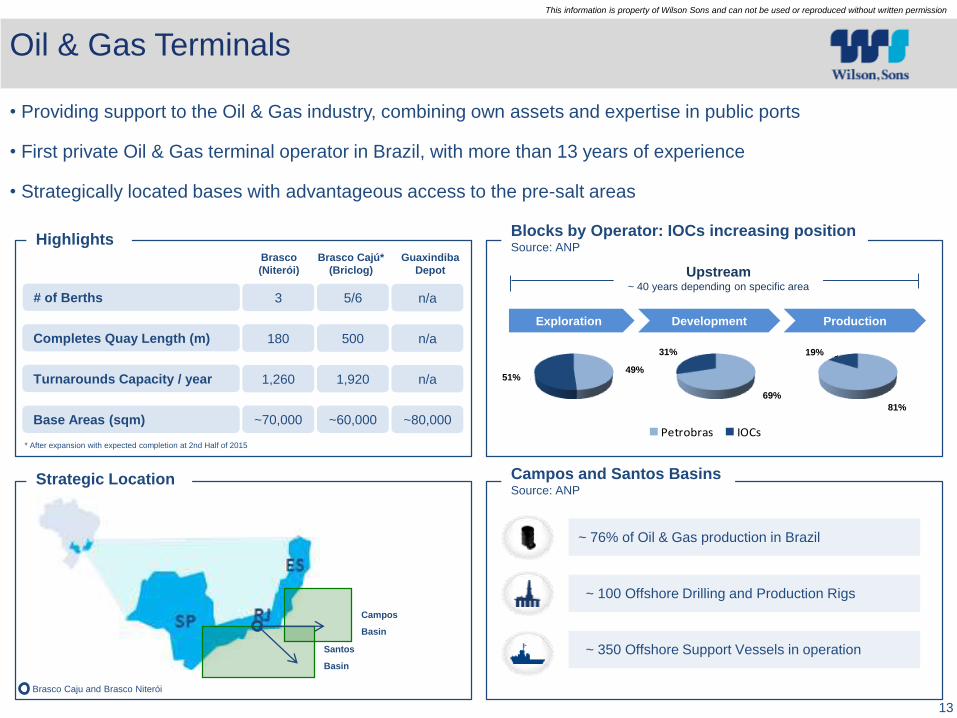

Oil & Gas Terminals

• Providing support to the Oil & Gas industry, combining own assets and expertise in public ports

• First private Oil & Gas terminal operator in Brazil, with more than 13 years of experience

• Strategically located bases with advantageous access to the pre-salt areas

Campos

Basin

Santos

Basin

Exploration Development Production

Upstream~ 40 years depending on specific area

~ 76% of Oil & Gas production in Brazil

~ 100 Offshore Drilling and Production Rigs

~ 350 Offshore Support Vessels in operation

84%

16%

70%

30%49%

51%

70%

30%

Petrobras IOCs / OGXBase Areas (sqm)

Completes Quay Length (m)

~70,000

180

~60,000

500

# of Berths 3 5/6

n/a

n/a

Brasco

(Niterói)

Brasco Cajú*

(Briclog)

Guaxindiba

Depot

Turnarounds Capacity / year 1,260 1,920 n/a

~80,000

* After expansion with expected completion at 2nd Half of 2015

69%

31%

81%

19%

Blocks by Operator: IOCs increasing positionSource: ANP

Strategic Location Campos and Santos BasinsSource: ANP

Highlights

49%51%

Brasco Caju and Brasco Niterói

14

This information is property of Wilson Sons and can not be used or reproduced without written permission

Towage

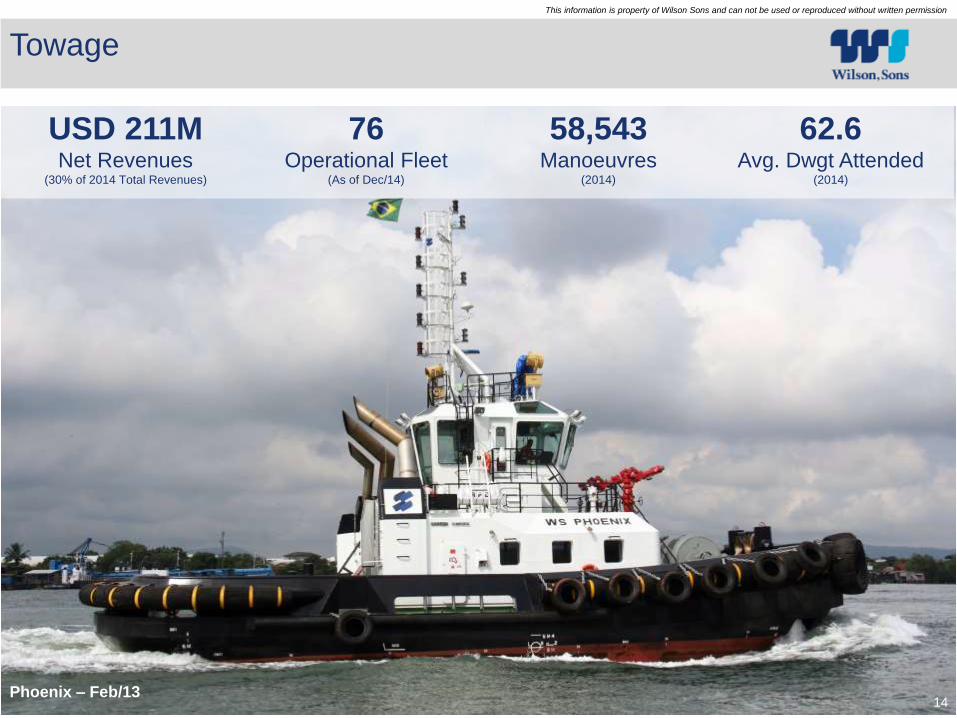

Phoenix – Feb/1314

USD 211MNet Revenues

(30% of 2014 Total Revenues)

58,543Manoeuvres

(2014)

62.6Avg. Dwgt Attended

(2014)

76Operational Fleet

(As of Dec/14)

15

This information is property of Wilson Sons and can not be used or reproduced without written permission

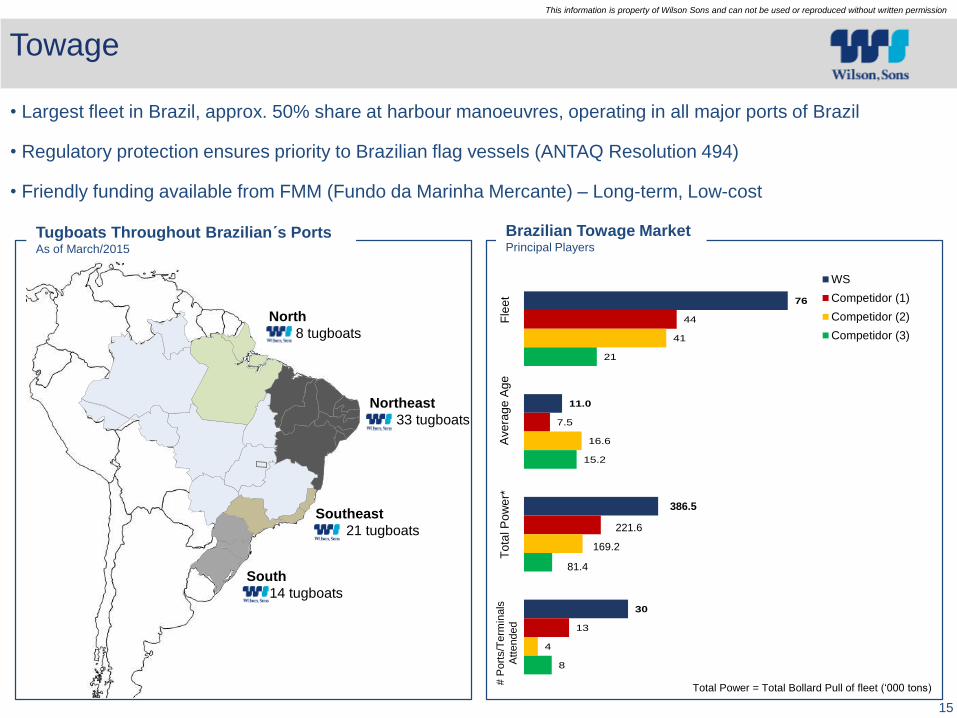

76

11.0

30

44

7.5

13

41

16.6

4

21

15.2

8

Fle

etA

vera

ge

Ag

eT

ota

l Po

wer

# P

ort

s A

tten

ded

WS

Competidor (1)

Competidor (2)

Competidor (3)

Towage

• Largest fleet in Brazil, approx. 50% share at harbour manoeuvres, operating in all major ports of Brazil

• Regulatory protection ensures priority to Brazilian flag vessels (ANTAQ Resolution 494)

• Friendly funding available from FMM (Fundo da Marinha Mercante) – Long-term, Low-cost

Tugboats Throughout Brazilian´s PortsAs of March/2015

Brazilian Towage MarketPrincipal Players

North

8 tugboats

Northeast

33 tugboats

Southeast

21 tugboats

South

14 tugboats

Fle

et

Ave

rag

eA

ge

To

tal P

ow

er*

# P

ort

s/T

erm

inals

Att

ended

73

11.0

124.4

26

44

7.5

94.7

13

40

16.6

81.2

4

21

15.2

59.8

8

Fle

et

Av

era

ge

Ag

eT

ota

l P

ow

er

# P

ort

s A

tte

nd

ed

WS

Competidor (1)

Competidor (2)

Competidor (3)

81.4

169.2

221.6

386.5

Total Power = Total Bollard Pull of fleet (‘000 tons)

16

This information is property of Wilson Sons and can not be used or reproduced without written permission

Offshore Support Vessels

PSV Alcatraz – Apr/14 2

USD 77MNet Revenues

(2014)

19 OSVsOperational Fleet

(As of Dec/14)

6,683Days in Operation

(Own Vessels 2014)

US$ 23,007Average Daily Rate

(As of Dec/14)

17

This information is property of Wilson Sons and can not be used or reproduced without written permission

PT 1607

PT 1624

Offshore Support Vessels

• Regulatory protection ensures priority to Brazilian flag vessels (ANTAQ Resolution 495)

• Friendly funding available from FMM (Fundo da Marinha Mercante) – Long-term, Low-cost

• Wilson Sons 100%-owned shipyard is a key competitive advantage

2015 2016 2017 2018 2019 2020 2021 2028 2029 2030

Albatroz Jun/11 4 years

Gaivota Jun/11 4 years

Cormoran Jan/15 2 years

Fragata Apr/07 6+2.5 years

Biguá Feb/10 6+2.5 years

Pelicano Jun/10 6+2.5 years

Atoba Jun/10 6+2.5 years

Petrel Jun/10 6+2.5 years

Skua Jun/10 6+2.5 years

Fulmar Jun/10 6+2.5 years

Talha-Mar Mar/11 6+2.5 years

Torda Oct/11 6+2.5 years

Sterna Mar/12 8+8 years

Batuíra Aug/12 8+8 years

Tagaz Mar/13 8+8 years

Prion Sep/13 8+8 years

Alcatraz Nov/13 8+8 years

Zarapito Apr/14 8+8 years

Mandrião Nov/13 4+4 years

Vessel Start Date Contract

PT 1606 2015 Under Negociation

2016 Under Negociation

2016 Under Negociation

PSV WS134

PSV WS135

Jul/16 6+6 years

Sep/16 6+6 years

Foreign Flag Vessel

In Contract (Petrobras)

In Contract with Client Option automatically maintaining day rate

Contract Option

18

This information is property of Wilson Sons and can not be used or reproduced without written permission

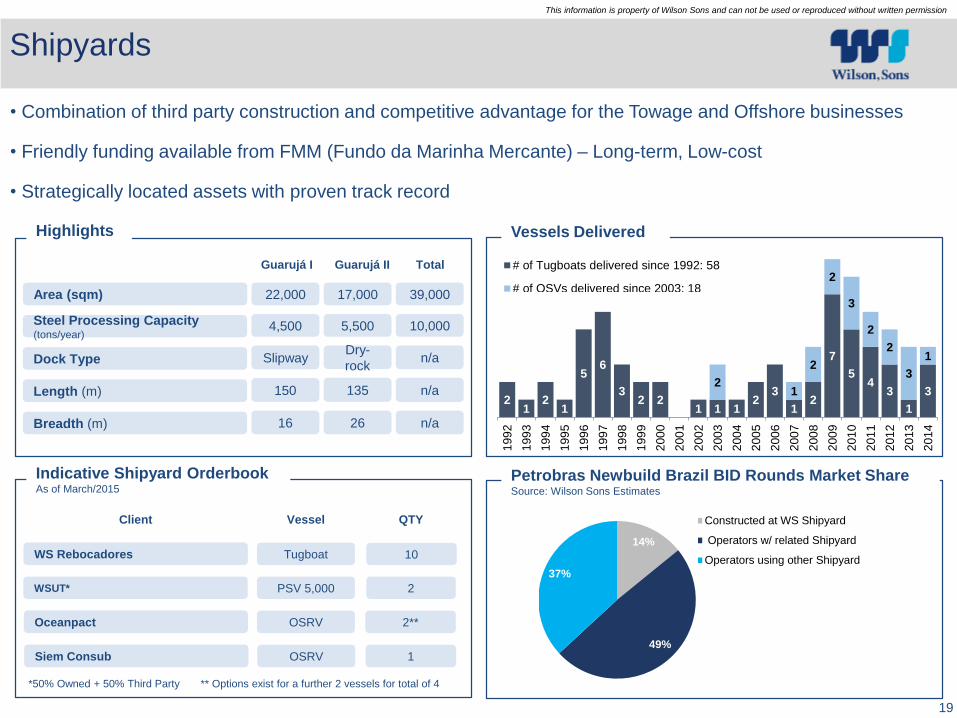

Shipyards

Guarujá II Shipyard 16Guarujá II Shipyard

49Vessels Delivered

(From 2004 to 2014)

10,000Processing Capacity

(Steel Tons / Year)

USD 103MNet Revenues

(16% of 2014 Total Revenues)

19

This information is property of Wilson Sons and can not be used or reproduced without written permission

Shipyards

Length (m)

Steel Processing Capacity(tons/year)

Dock Type

Vessels Delivered

Indicative Shipyard OrderbookAs of March/2015

Petrobras Newbuild Brazil BID Rounds Market ShareSource: Wilson Sons Estimates

Highlights

Guarujá I Guarujá II

WSUT* PSV 5,000 2

WS Rebocadores Tugboat 10

Oceanpact OSRV 2**

Client Vessel QTY

*50% Owned + 50% Third Party ** Options exist for a further 2 vessels for total of 4

Area (sqm)

Total

• Combination of third party construction and competitive advantage for the Towage and Offshore businesses

• Friendly funding available from FMM (Fundo da Marinha Mercante) – Long-term, Low-cost

• Strategically located assets with proven track record

Breadth (m)

22,000 17,000 39,000

4,500 5,500 10,000

SlipwayDry-

rockn/a

150 135 n/a

16 26 n/a

Siem Consub OSRV 1

14%

49%

37%

Constructed at WS Shipyard

Operators w/ related Shipyard

Operators using other Shipyard

14%

49%

37%

Constructed at WS Shipyard

Operators w/ related Shipyard

Operators using other Shipyard

21

21

56

32 2

1 1 12

3

12

7

54

3

1

32

1

2

2

3

2

2

3

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

2012

201

3

201

4

# of Tugboats delivered since 1992: 58

# of OSVs delivered since 2003: 18

21

21

56

32 2

1 1 12

3

12

7

54

3

1

32

1

2

2

3

2

2

3

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

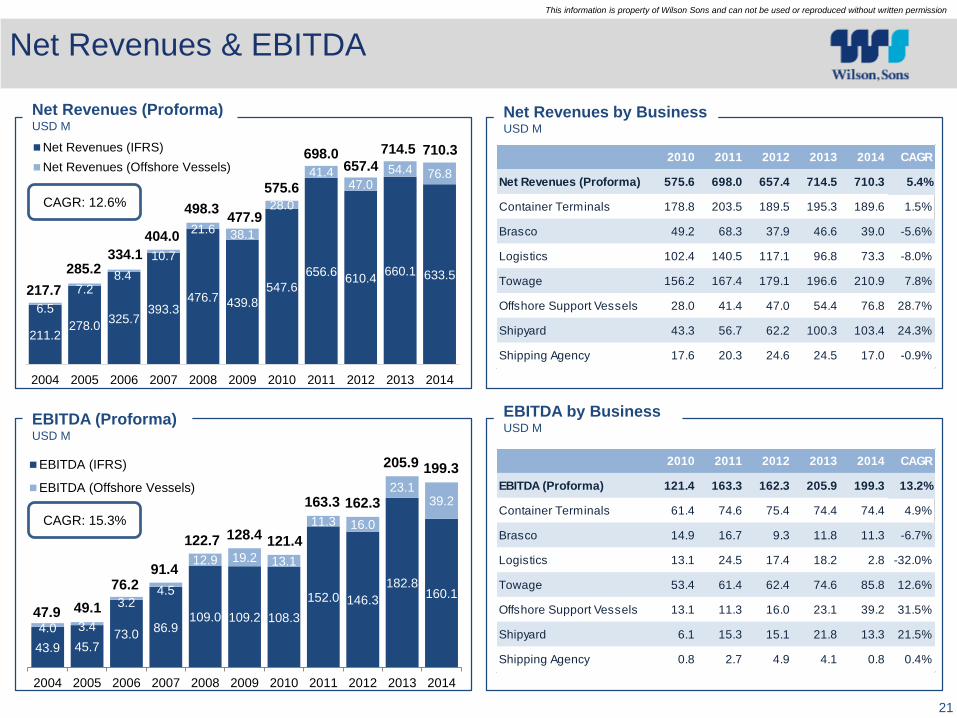

Financial Highlights

21

This information is property of Wilson Sons and can not be used or reproduced without written permission

43.9 45.773.0

86.9109.0 109.2 108.3

152.0 146.3

182.8160.1

4.0 3.4

3.24.5

12.9 19.2 13.1

11.3 16.0

23.139.2

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

EBITDA (IFRS)

EBITDA (Offshore Vessels)

47.9 49.1

76.291.4

122.7 128.4 121.4

163.3 162.3

205.9 199.3

211.2278.0

325.7393.3

476.7 439.8

547.6

656.6610.4

660.1 633.5

6.5

7.28.4

10.7

21.6 38.1

28.0

41.447.0

54.4 76.8

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Net Revenues (IFRS)

Net Revenues (Offshore Vessels)

217.7

285.2334.1

404.0

498.3477.9

575.6

657.4698.0 714.5 710.3

Net Revenues (Proforma)USD M

Net Revenues by BusinessUSD M

EBITDA (Proforma)USD M

EBITDA by BusinessUSD M

Net Revenues & EBITDA

CAGR: 12.6%

CAGR: 15.3%

2010 2011 2012 2013 2014 CAGR

Net Revenues (Proforma) 575.6 698.0 657.4 714.5 710.3 5.4%

Container Terminals 178.8 203.5 189.5 195.3 189.6 1.5%

Brasco 49.2 68.3 37.9 46.6 39.0 -5.6%

Logistics 102.4 140.5 117.1 96.8 73.3 -8.0%

Towage 156.2 167.4 179.1 196.6 210.9 7.8%

Offshore Support Vessels 28.0 41.4 47.0 54.4 76.8 28.7%

Shipyard 43.3 56.7 62.2 100.3 103.4 24.3%

Shipping Agency 17.6 20.3 24.6 24.5 17.0 -0.9%

2010 2011 2012 2013 2014 CAGR

EBITDA (Proforma) 121.4 163.3 162.3 205.9 199.3 13.2%

Container Terminals 61.4 74.6 75.4 74.4 74.4 4.9%

Brasco 14.9 16.7 9.3 11.8 11.3 -6.7%

Logistics 13.1 24.5 17.4 18.2 2.8 -32.0%

Towage 53.4 61.4 62.4 74.6 85.8 12.6%

Offshore Support Vessels 13.1 11.3 16.0 23.1 39.2 31.5%

Shipyard 6.1 15.3 15.1 21.8 13.3 21.5%

Shipping Agency 0.8 2.7 4.9 4.1 0.8 0.4%

22

This information is property of Wilson Sons and can not be used or reproduced without written permission

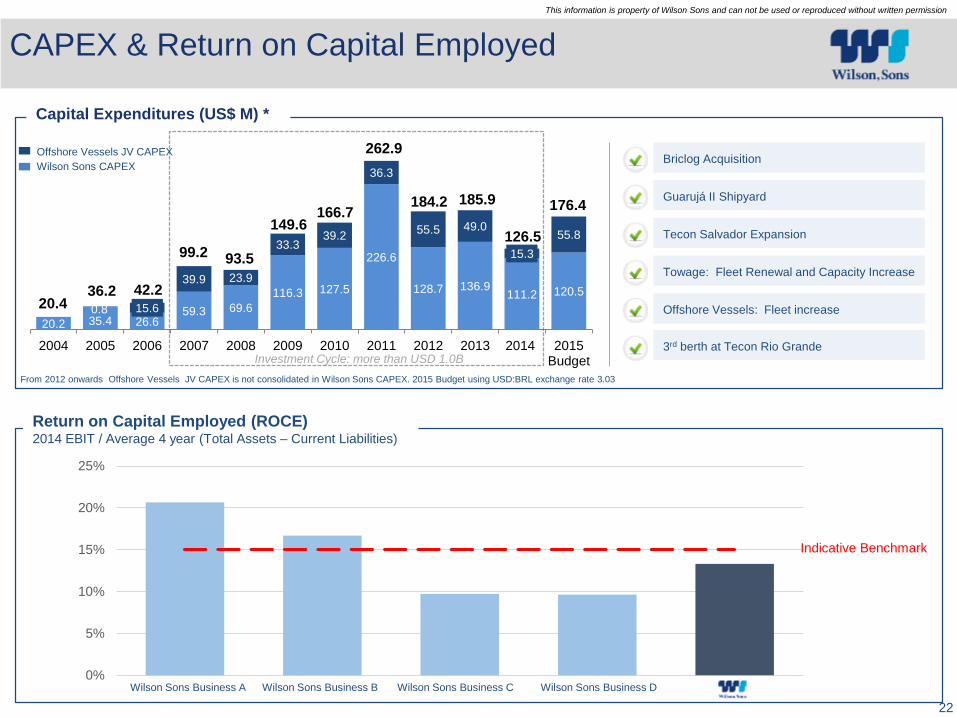

0%

5%

10%

15%

20%

25%

20.2 35.4 26.659.3 69.6

116.3 127.5

226.6

128.7 136.9111.2 120.5

0.8 15.6

39.9 23.9

33.339.2

36.3

55.5 49.0

15.3

55.8

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015Budget

93.5

166.7

262.9

20.436.2 42.2

99.2

149.6

176.4

126.5

185.9184.2

Capital Expenditures (US$ M) *

CAPEX & Return on Capital Employed

Return on Capital Employed (ROCE)2014 EBIT / Average 4 year (Total Assets – Current Liabilities)

Investment Cycle: more than USD 1.0B

Guarujá II Shipyard

Tecon Salvador Expansion

Towage: Fleet Renewal and Capacity Increase

Offshore Vessels: Fleet increase

3rd berth at Tecon Rio Grande

Briclog Acquisition

From 2012 onwards Offshore Vessels JV CAPEX is not consolidated in Wilson Sons CAPEX. 2015 Budget using USD:BRL exchange rate 3.03

Indicative Benchmark

Offshore Vessels JV CAPEX

Wilson Sons CAPEX

Wilson Sons Business A Wilson Sons Business B Wilson Sons Business C Wilson Sons Business D

23

This information is property of Wilson Sons and can not be used or reproduced without written permission

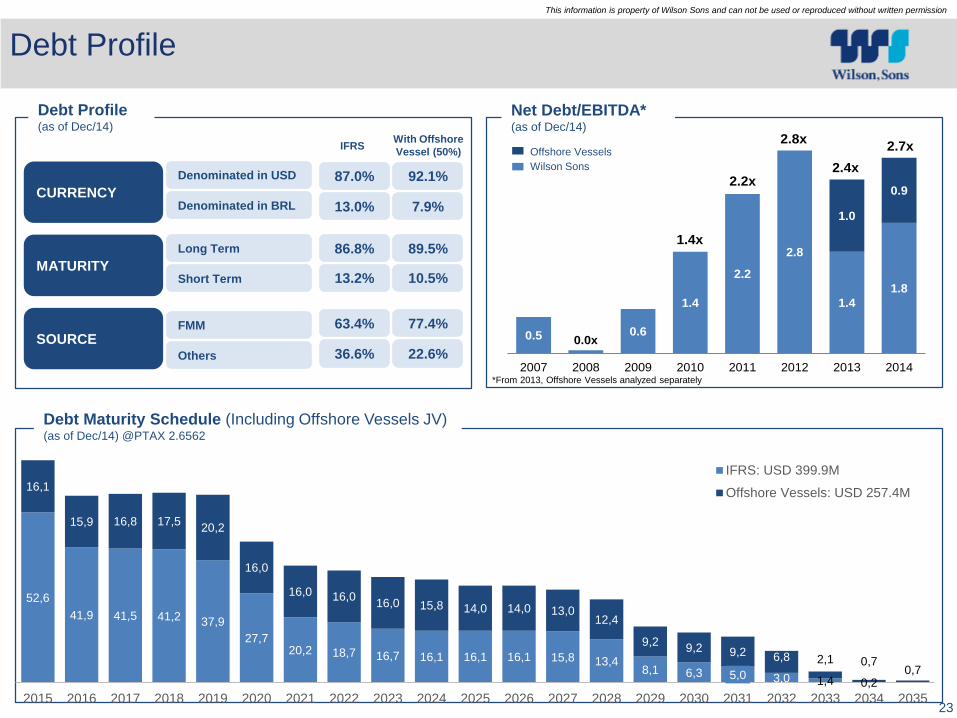

Debt Profile

0.5 0.0x0.6

1.4

2.2

2.8

1.4

1.8

1.0

0.9

2007 2008 2009 2010 2011 2012 2013 2014

1.4x

2.2x

2.8x

2.4x

2.7x

Net Debt/EBITDA*(as of Dec/14)

Debt Profile(as of Dec/14)

Debt Maturity Schedule (Including Offshore Vessels JV) (as of Dec/14) @PTAX 2.6562

*From 2013, Offshore Vessels analyzed separately

87.0%

13.0%

86.8%

13.2%

36.6%

63.4%

CURRENCY

Denominated in USD

Denominated in BRL

MATURITY

Long Term

Short Term

SOURCEOthers

FMM

92.1%

7.9%

89.5%

10.5%

22.6%

77.4%

IFRSWith Offshore

Vessel (50%) Offshore Vessels

Wilson Sons

52,6

41,9 41,5 41,2 37,9

27,720,2 18,7 16,7 16,1 16,1 16,1 15,8 13,4

8,1 6,3 5,0 3,0 1,4 0,2

16,1

15,9 16,8 17,520,2

16,0

16,0 16,016,0 15,8 14,0 14,0 13,0

12,4

9,29,2 9,2 6,8 2,1 0,7

0,7

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035

IFRS: USD 399.9M

Offshore Vessels: USD 257.4M

24

This information is property of Wilson Sons and can not be used or reproduced without written permission

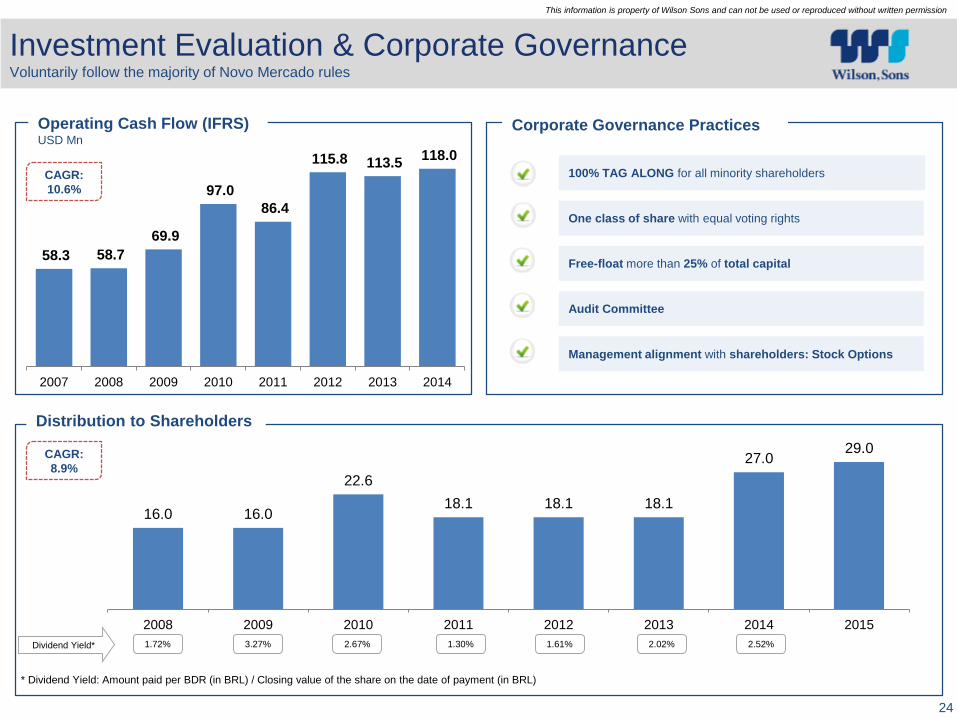

58.3 58.7

69.9

97.0

86.4

115.8 113.5 118.0

2007 2008 2009 2010 2011 2012 2013 2014

Operating Cash Flow (IFRS) USD Mn

Investment Evaluation & Corporate GovernanceVoluntarily follow the majority of Novo Mercado rules

100% TAG ALONG for all minority shareholders

One class of share with equal voting rights

Free-float more than 25% of total capital

Audit Committee

Management alignment with shareholders: Stock Options

Corporate Governance Practices

CAGR:

8.9%

1.72% 3.27% 2.67% 1.30% 1.61% 2.02%Dividend Yield*

* Dividend Yield: Amount paid per BDR (in BRL) / Closing value of the share on the date of payment (in BRL)

2.52%

Distribution to Shareholders

16.0 16.0

22.6

18.1 18.1 18.1

27.029.0

2008 2009 2010 2011 2012 2013 2014 2015

CAGR:

10.6%

Annex

26

This information is property of Wilson Sons and can not be used or reproduced without written permission

Brazilian Container Terminals24 Terminals competing against

Vila do Conde CONVICON

• CTOPecém

Suape • Tecon Suape

Salvador TECON Salvador

Rio Grande TECON Rio Grande

Vitória • TVV

Imbituba • TECON Imbituba

Rio de Janeiro • T1

• T2

Itaguaí • Sepetiba TECON

Santos

• TECON Santos

• Tecondi

• Rodrimar

• T-35/T-37

• BTP

• Embraport

Paranaguá • TCP

SFSul e Itapoá• TESC

• Tecon SC

Itajaí

Navegantes

• TECONVI

• Portonave

Manaus • Superterminais

• Chibatão

BRAZIL

AR

UY

CH

BO

PA

PE

Buenos Aires

Montvideo

27

This information is property of Wilson Sons and can not be used or reproduced without written permission

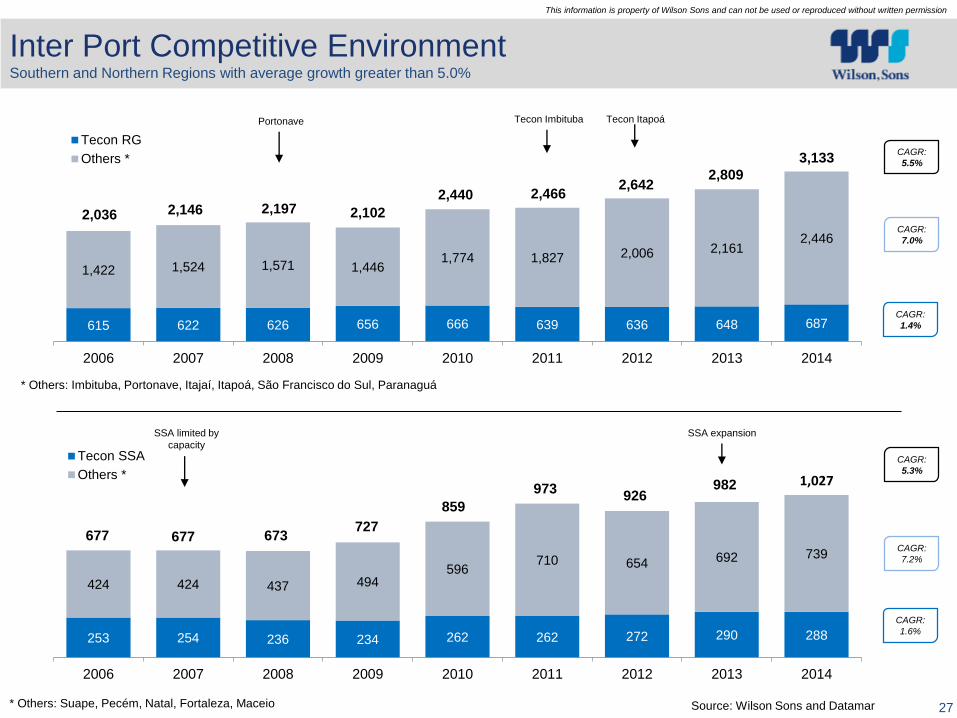

Inter Port Competitive EnvironmentSouthern and Northern Regions with average growth greater than 5.0%

Portonave Tecon Itapoá

CAGR:

1.4%

CAGR:

7.0%

CAGR:

5.5%

Tecon Imbituba

* Others: Imbituba, Portonave, Itajaí, Itapoá, São Francisco do Sul, Paranaguá

* Others: Suape, Pecém, Natal, Fortaleza, Maceio

CAGR:

1.6%

CAGR:

7.2%

CAGR:

5.3%

SSA limited by

capacity

SSA expansion

Source: Wilson Sons and Datamar

615 622 626 656 666 639 636 648 687

1,422 1,524 1,571 1,4461,774 1,827 2,006 2,161

2,446

2006 2007 2008 2009 2010 2011 2012 2013 2014

Tecon RG

Others *

2,036 2,146 2,197 2,102

2,440 2,4662,642

2,809

3,133

253 254 236 234 262 262 272 290 288

424 424 437 494596

710 654 692 739

2006 2007 2008 2009 2010 2011 2012 2013 2014

Tecon SSA

Others *

677 677 673727

859

973926

982 1,027

28

This information is property of Wilson Sons and can not be used or reproduced without written permission

Investor Relations Contact Info

BM&FBovespa: WSON33

IR website: www.wilsonsons.com/ir

Twitter: @WilsonSonsIR

Youtube Channel: WilsonSonsIR

Facebook: Wilson, Sons

Felipe Gutterres

CFO of the Brazilian Subsidiary and Investor Relations

+55 (21) 2126-4112

Michael Connell

IRO, International Finance & Finance Projects

+55 (21) 2126-4107

Kelly Calazans

Investor Relations

+55 (21) 2126-4105

Júlia Ornellas

Investor Relations

+55 (21) 2126-4293