Jicable'15 Welcome LectureJosias Matos de Araujo

Eletrobras

June, 2015

Regulatory framework in Brazil

Regulatory Framework in Brazil

3

Politics

Regulation

and

Supervision

Market

Institutional

Agents

National

Congress

Electricity Sector

Monitoring

Committee - CMSE

Brazilian Electricity

Regulatory Agency

ANEEL

National Council for Energy Policy - CNPE

Electric Energy

Trading Chamber

CCEE

National System

Operator - ONS

Energy Research

Company - EPE

President of the

Republic of Brazil

G

T

D

C

Ministry of Mines

and Energy - MME

EletrobrasPlayers

BNDES

and other

banks

State

Agencies

ANP, ANATEL

Consumers

Council

SNRH, MMA,

ANA, IBAMA

SDE, SEAD,

CADE

Brazilian Electricity Market

&

Generation, Transmission and

Distribution Overview

Population1:

201,901,000

Area:

8,514,876,599 km²

Network Energy Consumption2,3:

463,335 GWh

Energy Consumption per Capita1,2,3:

2,295 kWh/yr.

Average Energy Consumption:

64,003 aMW

Number of Consumers 4:

77,069,509

Residential Consumers 4 :

65,928,608

Average Monthly Energy Consumption:

516,1 kWh/mo.

Average Monthly Residential Energy Consumption :

163,0 kWh/mo.

Sources: 1 IBGE (Brazilian Institute of Geography and Statistics), 20132 Include self-produced energy3 EPE (Energy Research Company), 20134 ANEEL (Brazilian Electricity Regulatory Agency), 2014

Electric Energy Consumption Statistics in Brazil

5

Electric Energy Consumption by Sector

23,01%

31,03%15,65%

4,50%

8,30%

17,51%

463,335

GWh

Residential

Industry

Commercial

Rural

Other

Losses

Source: EPE (Energy Research Company), 20136

Brazilian Electric Energy Market Players

Source: CCEE (Electric Energy Trading Chamber), 20157

0

500

1000

1500

2000

2500

3000

Trader Independent

producer

Generator Special

consumer

Free

consumer

Self-producer Distributor Total Players

2,222

2,5792,715

2012 2013 2014

Generation in Brazil

- Actual Status and Prospects -

National Installed Capacity (GW), 1974-2014

41

58

91

134

0

20

40

60

80

100

120

140

1974 1979 1984 1989 1994 1999 2004 2009 2014

Source: National Energy Balance (BEN 2014), EPE9

Energy Generation: How the installed capacity is shared by type source? 1974 --

2014

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1974 1979 1984 1989 1994 1999 2004 2009 2014

Hydroelectric Termoelectric Eolic Nuclear Solar (< 0.01%)

Source: National Energy Balance (BEN 2014), EPE10

WindThermoeletric

National Installed Capacity (MW)

89,193

37,827

4,888

1,990

Hydroelectric

Termoelectric

Eolic

Nuclear

Solar (15 MW)

133,913

MW

Source: National Energy Balance (BEN 2014), EPE11

Wind

1st. Bid of solar (2014) : 890 MW contracted

Evolution of Brazilian Installed Capacity by Geographic Region (GW)

Source: PDE 2023 (Ten-year Energy Expansion Plan 2023), EPE

+57%

12

N

NE

S

SE & CW+20%

+210%

+31%

+107%

70 84

14 45

18 38

20 27

2

0

2

3

2

0

1

3124 195

Hydro

82,620

Import

6,032

SHP

5,538

Wind

5,452

Biomass

10,684

Solar

0

Others

21,674

Evolution of Renewable Energy Generation (MW)

Source: PDE 2023 (Ten-year Energy Expansion Plan 2023), EPE

Hydro

112,178

Import

4,716

SHP

7,319

Wind

22,439

Biomass

13,983

Solar

3,500

Others

47,241

2013

2023

13

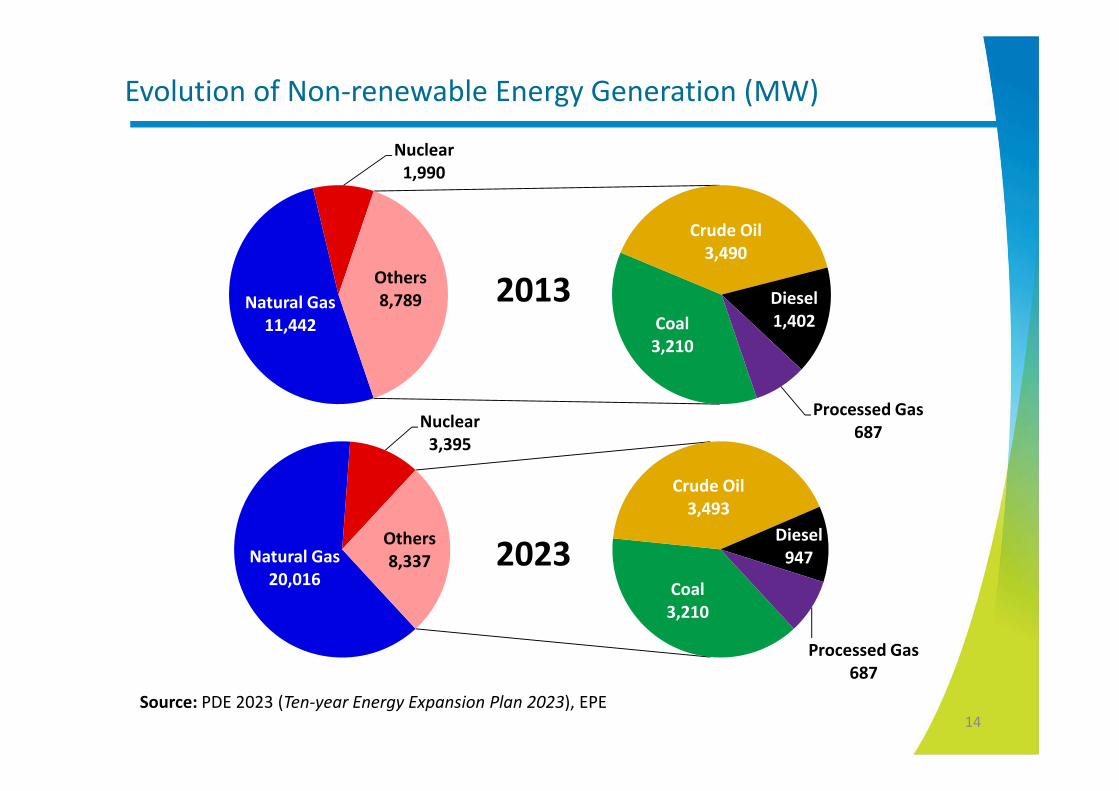

Natural Gas

20,016

Nuclear

3,395

Coal

3,210

Crude Oil

3,493

Diesel

947

Processed Gas

687

Others

8,337

Evolution of Non-renewable Energy Generation (MW)

Source: PDE 2023 (Ten-year Energy Expansion Plan 2023), EPE

2013

2023

14

Natural Gas

11,442

Nuclear

1,990

Coal

3,210

Crude Oil

3,490

Diesel

1,402

Processed Gas

687

Others

8,789

Transmission in Brazil

- Current Status and Prospects -

Interconnected National System - SIN

99% Integrated1% Isolated

Source: MME (Ministry of Mines and Energy), 201416

0

20

40

60

80

100

120

140

1989 1994 1999 2004 2009 2014

230 kV 345 kV 440 kV 500 kV ±600 kV 750 kV

Transmission Lines (Thousand km), 1989-2014

Source: National Energy Balance (BEN 2014), EPE17

52,680

10,303

6,728

40,649

12,816

2,683

230 kV

345 kV

440 kV

500 kV

±600 kV

750 kV

Source: Electrical System Monitoring Bulletin, CMSE, 2014

Transmission Lines (km)

18

125,859

km

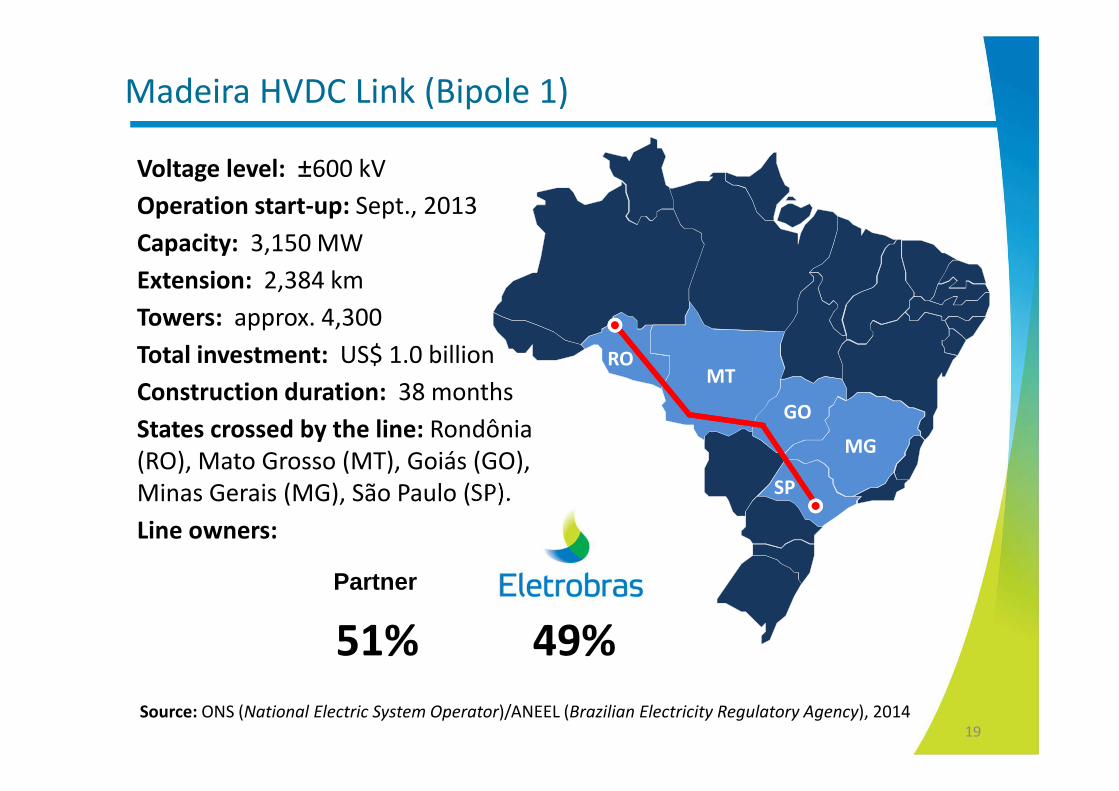

Madeira HVDC Link (Bipole 1)

Voltage level: ±600 kV

Operation start-up: Sept., 2013

Capacity: 3,150 MW

Extension: 2,384 km

Towers: approx. 4,300

Total investment: US$ 1.0 billion

Construction duration: 38 months

States crossed by the line: Rondônia

(RO), Mato Grosso (MT), Goiás (GO),

Minas Gerais (MG), São Paulo (SP).

Line owners:

ROMT

GO

SP

MG

51% 49%

Source: ONS (National Electric System Operator)/ANEEL (Brazilian Electricity Regulatory Agency), 201419

Partner

Madeira HVDC Link (Bipole 1)

Source: Internet20

Madeira HVDC Link (Bipole 2)

Voltage level: ±600 kV

Operation start-up: 2015 (prevision)

Capacity: 3,150 MW

Extension: 2,412 km

Towers: approx. 4,300

Total investment: US$ 973 million

Construction duration: 50 months

States crossed by the line: Rondônia

(RO), Mato Grosso (MT), Goiás (GO),

Minas Gerais (MG), São Paulo (SP).

Line owners:

ROMT

GO

SP

MG

51% 49%

Source: ONS (National Electric System Operator)/ANEEL (Brazilian Electricity Regulatory Agency), 2014 21

Partner

Belo Monte UHVDC Link (Bipole 1)

PA

TO

GOMG

Voltage level: ±800 kV

Under construction

Capacity: 4,000 MW

Extension: 2,096 km

Towers: approx. 4,500

Total investment: US$ 1.67 billion

Construction duration: 46 months

States crossed by the line: Pará (PA),

Tocantis (TO), Goiás (GO), Minas

Gerais (MG).

Line owners:

51% 49%Source: ANEEL (Brazilian Electricity Regulatory Agency), 2014

22

Partner

Belo Monte UHVDC Link (Bipole 2)

PA

TO

GOMG

Voltage level: ±800 kV

Capacity: 3,850 MW

Extension: 2,518 km

Total investment: US$ 2.58

billion

Prevision for commercial

operation: September, 2020.

States crossed by the line: Pará

(PA), Tocantis (TO), Goiás (GO),

Minas Gerais (MG), Rio de

Janeiro (RJ).

Line owners:

Source: ANEEL (Brazilian Electricity Regulatory Agency), 201423

RJ

Evolution of Transmission Lines (km)

Source: PDE 2023 (Ten-year Energy Expansion Plan 2023), EPE24

63.48%

0

50000

100000

150000

200000

250000

300000

230 kV 345 kV 440 kV 500 kV ±600 kV ±800 kV Total

49,897

10,2726,728

39,083

3,996

109,976

68,656

11,9186,922

76,408

6,371 9,518

179,793

Existing in 2013 in 2023

Transmission Line Investments from 2013-2023

Source: PDE 2023 (Ten-year Energy Expansion Plan 2023), EPE. 25

15%

4%

65%

1%

3%

12%

±800 kV ±600 kV 500 kV 440 kV 345 kV 230 kV

US$ 16.71

Billion

Substations Investments from 2013-2023

Source: PDE 2023 (Ten-year Energy Expansion Plan 2023), EPE. 26

24%

3%

46%

2%

7%

18%

±800 kV ±600 kV 500 kV 440 kV 345 kV 230 kV

US$ 9.47

Billion

2023

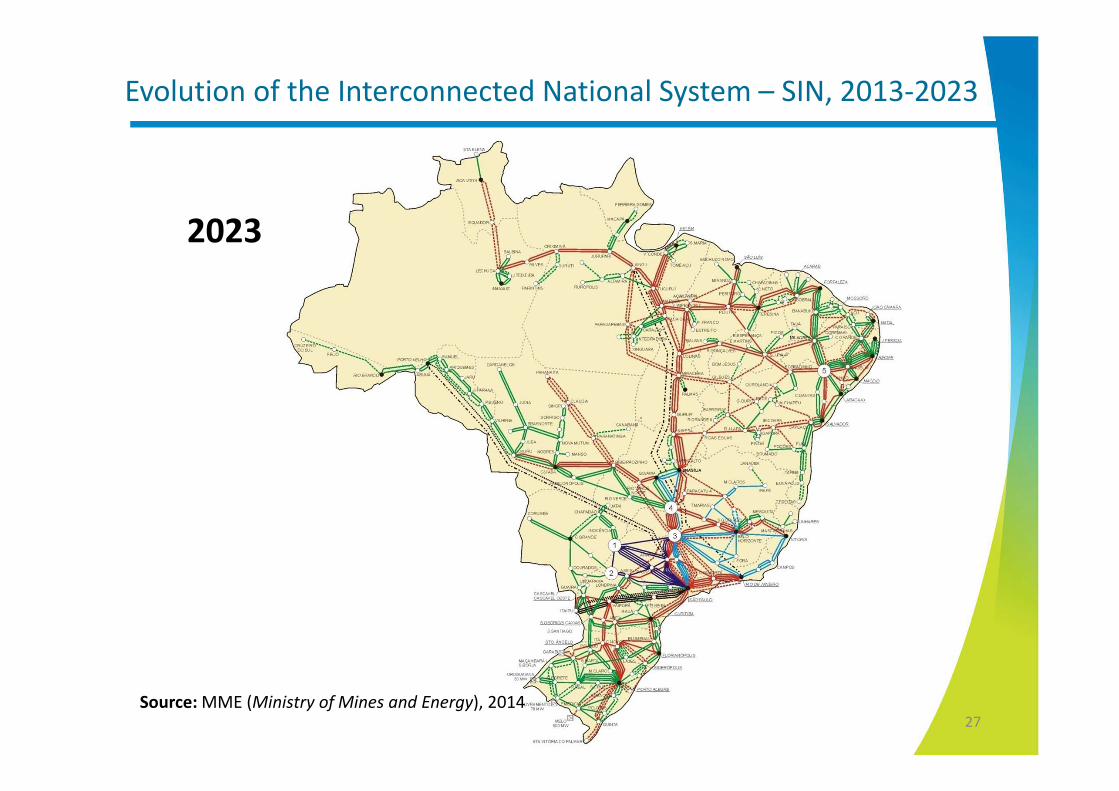

Evolution of the Interconnected National System – SIN, 2013-2023

Source: MME (Ministry of Mines and Energy), 201427

Distribution in Brazil

- Current Status and Prospects -

Distribution Utilities in Brazil

Source: ABRADEE, 2014 29

Distribution Utilities in Brazil

Source: ABRADEE, ANEEL and companies sites, 201430

Total Consumers 77.1 Million

Residential Consumers 65.9 Million

Nº of new consumers/Year 2.9 Million

Distribution lines (km) More than 3.1 Million

Undergrounded transmission lines (km) Almost 13,000

Gross Revenues US$ 56.7 Billion

Annual investments US$ 3.85 Billion

Market (free + captive) 432 mil GWh (343 captive)

Underground Distribution Systems Installed in Brazil

Source: ANEEL, 201431

Jardim dos Namorados System – Salvador (BA)

Ibirapuera Park – São Paulo (SP)

Porto Maravilha Region – Rio de Janeiro (RJ)Before After

Downtown Zone – Belo Horizonte (MG)

Energy Integration in South America

Source: MME (Ministry of Mines and Energy), 201533

Electric Energy

Natural Gas

Energy import/export

A brief overview of the

Eletrobras System

(100.00%)

(94.26%)

(100.00%)

SPEs

G 7

T 9

∑ 16

Belo Monte

Rouar S.A.

Centrales Hidroeléctricas de Nicaragua

– CHN

(100.00%)

(83.71%)(99.91%)

(99.99%)

(50,00%)

(99.56%)

(99.58%)

(99.47%)

(99.88%)

SPEs

G 43

T 10

∑ 53

SPEs

G 59

T 18

∑ 77

SPEs

G 10

T 10

∑ 20

Minorities

G, T and D 26

Binational Generation

Shareholdings Abroad

Inambari Geração de Energia S.A. –

IGESA

(50.00%)

(50.00%)

(29.40%)

(15.00%)

(49.00%)

Generation and Transmission Generation

(100.00%)

(100.00%)

(100.00%)

DistributorsShareholdings

Mangue Seco 2 Eolic

Eletrobras System

(50,93%)

Research Center

35

Eletrobras System

36

33.0%

48.4%Transmission Lines

125,858 km

Generation (Installed capacity)

133,918 MW

BRAZILBRAZIL

Source: Eletrobras Anual Report 2014

*>=230 KV (including partnerships)

Eletrobras

System

Transmission

lines (Total length

- km) (*)

Generation

(Installed capacity

- MW)

Furnas 19,907 8,829

Chesf 19,692 10,616

Eletronorte 10,703 9,476

Eletrosul 11,140 428

Itaipu - 7,000

CGTEE - 840

Eletronuclear - 1,990

Eletrobras - 13

Amazonas En. 701 2,083

CERON - 3

Partnership 5,440 2,891

Total 67,582 44,156

85%

5%

1% 9%

Hydro

Nuclear

Solar+Wind

Fuel

Eletronuclear

Holding

Furnas

Eletronorte

Eletrosul

Chesf

Amazonas Energia

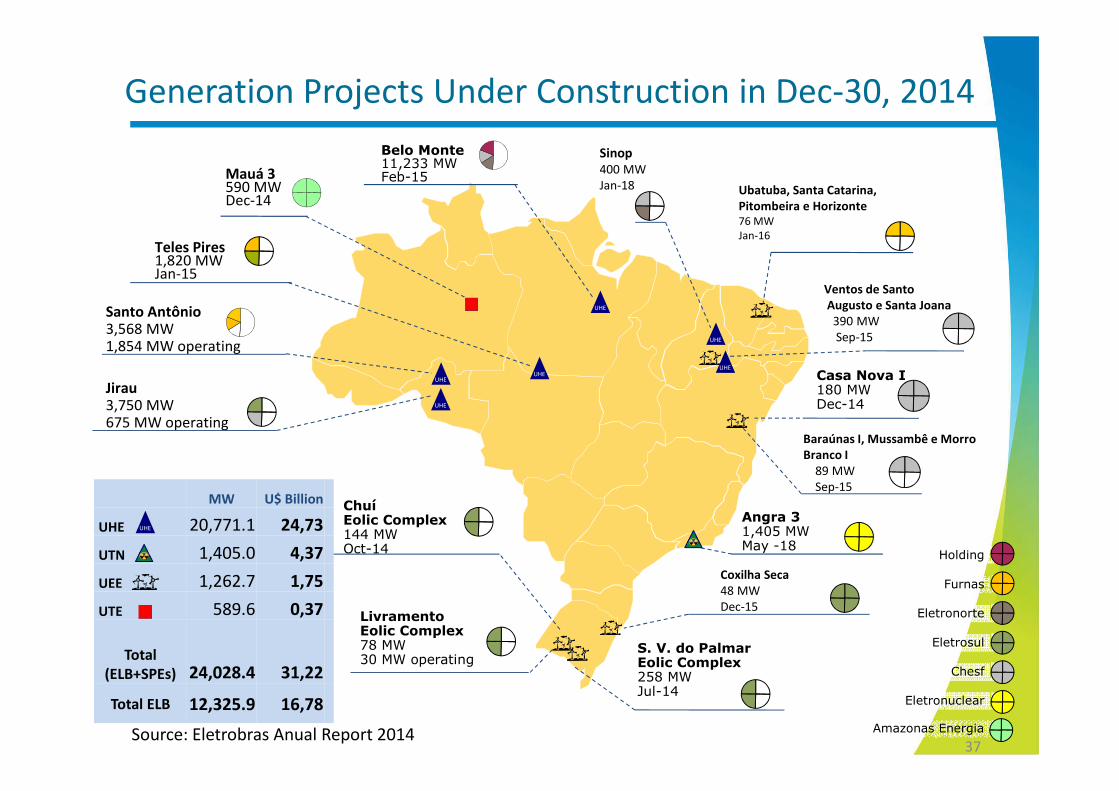

MW U$ Billion

UHE 20,771.1 24,73

UTN 1,405.0 4,37

UEE 1,262.7 1,75

UTE 589.6 0,37

Total

(ELB+SPEs) 24,028.4 31,22

Total ELB 12,325.9 16,78

Belo Monte11,233 MWFeb-15

Santo Antônio3,568 MW1,854 MW operating

Jirau3,750 MW675 MW operating

Teles Pires1,820 MWJan-15

Mauá 3590 MWDec-14

Angra 31,405 MWMay -18

LivramentoEolic Complex78 MW30 MW operating

Casa Nova I180 MWDec-14

UHE

S. V. do PalmarEolic Complex258 MWJul-14

ChuíEolic Complex144 MWOct-14

Ubatuba, Santa Catarina,

Pitombeira e Horizonte76 MW

Jan-16

Sinop400 MW

Jan-18

Ventos de Santo

Augusto e Santa Joana

390 MW

Sep-15

Coxilha Seca

48 MW

Dec-15

Baraúnas I, Mussambê e Morro

Branco I

89 MW

Sep-15

UHE

UHE

UHE

UHE

UHE

UHE

Generation Projects Under Construction in Dec-30, 2014

37Source: Eletrobras Anual Report 2014

BRA

ARG

RR

AC

PA

ROMT

MS

CE

TO

GO

MG

BA

SP

PR

SC

RJ

ES

SE

RN

PB

PEAL

DF

1 Project

220 MW

AP

1 Project

350 MW

7 Projects14,450.6 MW

2 Projects596 MW

6 Projects

1,412.2 MW

3 Projects

1,479 MW

5 Projects

483 MW

2 Projects

2,200 MW

Main Projects (Values in US$)

S. Luiz do Tapajós PA 8,040 MW 9,56 Bi

Jatobá PA 2,338 MW 3,39 Bi

Marabá PA 1,850 MW 4,16 Bi

Serra Quebrada MA/TO 1,328 MW 1,31 Bi

Garabi BRA/ARG 1,152 MW 1,54 Bi

Panambi BRA/ARG 1,048 MW 1,41 Bi

Total - 15,756 MW 21,38 Bi

Studies and Projects

Power

Units

Installed

Capacity (MW)

US$

Bi

Basic Project 04 327.6 0,27

Feasibility Study 24 21,659.6 27,58

Inventory Study 01 270

Total 29 22,257.2 27,85

1 Project

270 MW

AMMA

1 Project

796.4 MW

Basics Studies and Projects – Generation

38

Source: Eletrobras Anual Report 2014

Full

ParticipationPartnership Total

Investment:

US$ 3.52

billion, being

US$ 771

million in full

participation

2,784 km - 32

projects LTs +

SEs associated

8,247 Km - 23

projects LTs +

SEs associated

being 4,013.3

km owned by

ELB

11,031 km

8,360 MVA

14,884 MVA

being 7,237.5

MVA owned by

ELB

23,244

MVA

LTs Eletrobras System

LTs Eletrobras System with Partnership

LTs Other Companies

Existent Future

Main Transmission Lines Projects under construction

Paraná River Complex

Paranapanema River Complex

Grande River Complex

Paranaíba River Complex

Paulo Afonso Complex5

4

3

2

1

39Source: Eletrobras Anual Report 2014

468,685

km

6,658,008

Distribution – Eletrobras System

40

700

Cities attended

Source: Eletrobras Anual Report 2014

4%

15%

13%

17%9%

1%

41%

3%15%

9%

32%7%

0%

34%

4%9%

9%

18%

12%1%

47%

Transmission Lines Consumers

Electric Inclusion with Insulated

Cables in Brazil

42

Light for All Program

The “Light for All” program was launched by the

Federal Government in November 2003, and it

has as its goal to end the electric exclusion in the

country in the rural ambit.

16 million people attended

43

The Amazon Rainforest

The Amazon region has peculiarities that make it difficult to

supply electricity to households in isolated regions.

Long stretches of forest, rivers, streams and lakes become

obstacles to the construction of conventional air distribution

network.

Eletrobras owns the local distribution company.

The chosen solution is the use of underwater cables.

Underwater cable from Manacapuru to St. Afonso Island

Underwater cable from Manacapuru to St. Afonso Island

46

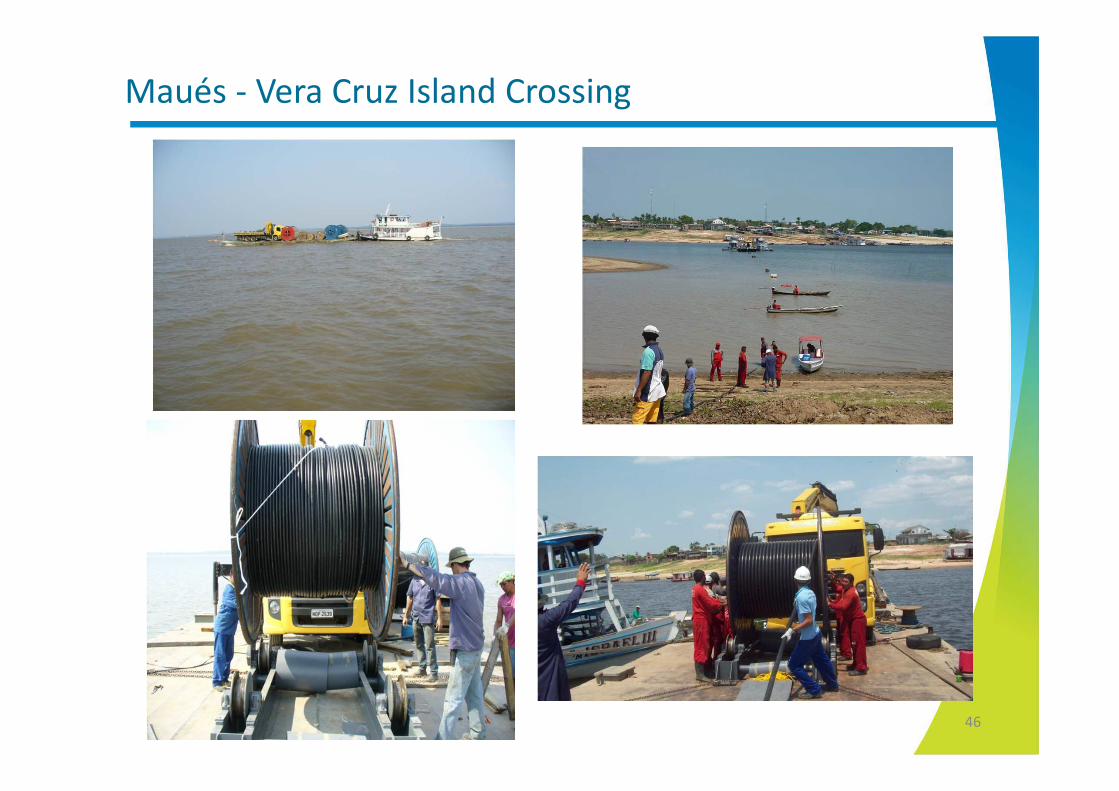

Maués - Vera Cruz Island Crossing

47

Maués - Vera Cruz Island Crossing

3,447.86 meters

48

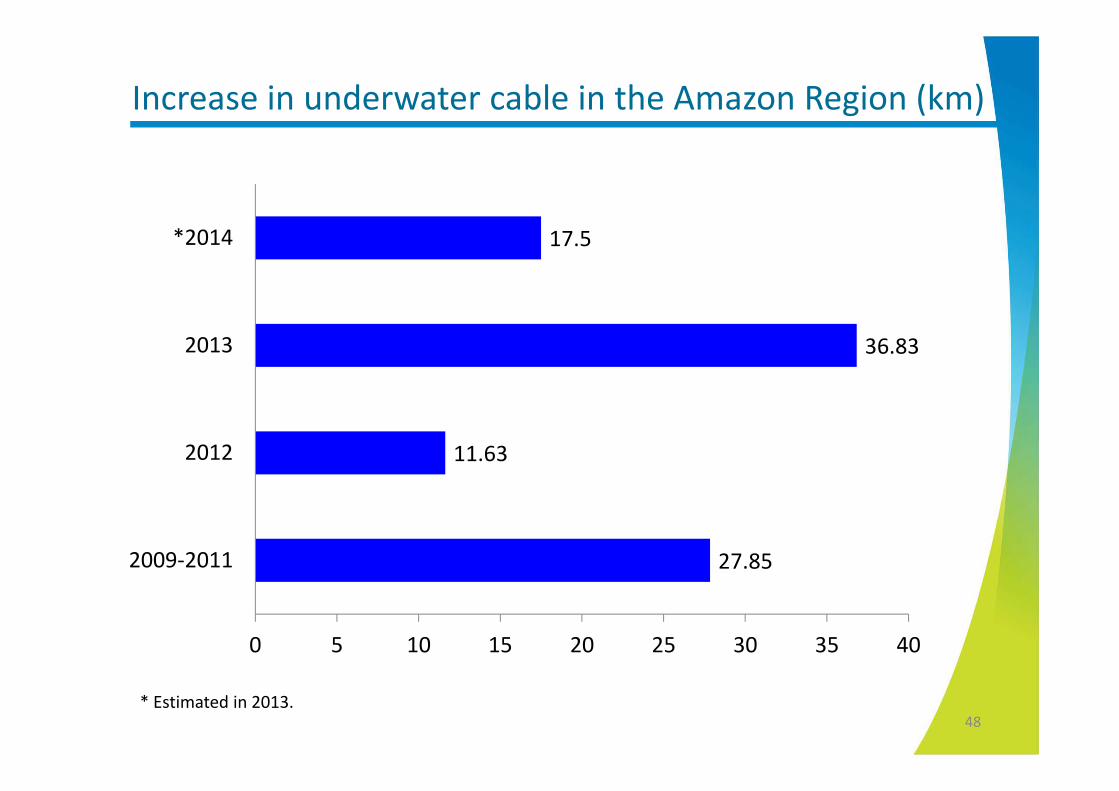

Increase in underwater cable in the Amazon Region (km)

27.85

11.63

36.83

17.5

0 5 10 15 20 25 30 35 40

2009-2011

2012

2013

*2014

* Estimated in 2013.

49

Light for All underwater cables statistics in the Amazon region(*)

67 total crossings.

69 km of underwater cables.

31 cities crossed.

10,300 households served.

51,500 people served.

4.53 km is the largest river crossing located at Andirá r iver.

(*) Data between 2009-2013.

Some of the people who are now

served…

Challenges

• Huge investments in electrical infrastructure expansion in Brazil;

• Great business opportunities for generation, transmission and distributioncompanies from now by 2023;

– Almost 6,000 km new transmission lines every year;

– Almost 5,000 MW new generation every year;

– Almost 2.9 million new consumers every year.

• Increase use of underground cables in crowded cities;

• Integrate new small plants (distributed generation) in the existent networks;

• Improve smart grids actions in distribution network;

• Promote regional integration with Latin America countries;

Challenges

55

• Increasing and maintaining a clean generation matrix in Brazil

• Stimulate a consistent environmental protection in new power plants andtransmission lines

• Work in towards a sustainable company

• Act to reduce emission level of tons of CO2 every year

Challenges

56